Contents

Index of Services Production: India Gets Its First Monthly Services Barometer

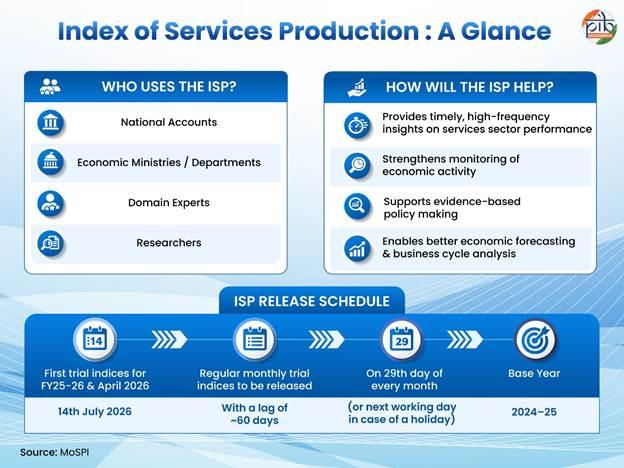

- MoSPI (Ministry of Statistics and Programme Implementation) launched the Index of Services Production (ISP) in July 2026 — India’s first high-frequency monthly indicator dedicated to measuring short-term changes in the output of the formal services sector.

- The ISP is India’s services-sector counterpart to the Index of Industrial Production (IIP), which measures mining, manufacturing and electricity but does not capture services — leaving the economy’s largest sector (53% of GVA) without a monthly pulse-check.

- A Trial Index for 19 sub-sectors covering ~60% of services GVA was released first, for April 2026, with base year 2024-25.

- The IIP, published monthly by MoSPI since 1950, captures mining, manufacturing and electricity only — structured as a fixed-weight Laspeyres index (current base year: 2011-12). It has no services component.

- India’s structural shift: services crossed 50% of GVA in 2013-14 and have remained the dominant sector since. Monitoring economic activity using only the IIP increasingly misrepresents the true growth picture.

- Three data developments made ISP compilation feasible now: (1) availability of high-frequency GST outward supplies data; (2) launch of ASISSE (Annual Survey of Incorporated Services Sector Enterprises) in April 2026; (3) expansion of digital administrative databases for railways, aviation, banking and insurance.

- Institutional architecture: MoSPI constituted a Technical Advisory Committee (TAC) in May 2025, chaired by Ms. Debjani Ghosh, Distinguished Fellow, NITI Aayog, with members from academia, industry associations and service-sector ministries.

- Global precedent: The OECD Compilation Manual for ISP (2007) is the most comprehensive international guideline; Eurostat is another key reference. Countries already publishing ISP equivalents: France, Spain, Slovenia (EU); South Korea (monthly Service Industry Activity Index); United Kingdom (Monthly Index of Services).

- The ISP uses a fixed-weight Laspeyres volume index with 2024-25 as the base year (aligned with the rebased CPI series). Sectoral weights are derived from each sub-sector’s Gross Value Added (GVA) contribution, converting nominal turnover into real output using price deflators.

- Deflators used (since comprehensive Service Producer Price Indices / SPPIs are unavailable in India):

- WPI (Wholesale Price Index) for wholesale trade

- Sector-specific CPI where available; CPI-General for banking, insurance and repair & maintenance

- CPI-Services / CPI Non-Food as a proxy for other sectors — justified because over 80% of non-food inflation is linked to services or their cost-push factors (energy, transport, housing)

- Quantity vs. value indicators: Air transport and railways use quantity-based indicators (e.g. passenger-kilometres); most other services use value-based indicators (turnover, sales) deflated to real terms.

- Three pillars of data:

Source Sectors Covered Administrative / secondary data Air transport, railways, banking, insurance GST outward supplies data Wholesale & retail trade, transport (road/water/warehousing), telecom, accommodation & food, real estate, IT, professional services, arts & recreation ASISSE (once available) Health and education (excluding government) — to be added later - Health and education excluded from the initial framework — ASISSE, launched only in April 2026, needs time to build a reliable dataset.

- Release schedule: Monthly trial indices published with a ~60-day lag on the 29th of each month (or next working day). Full regular monthly series to follow after trial validation.

- Key users: MoSPI (National Accounts), RBI (monetary policy), economic ministries, researchers and investors for GDP nowcasting, business cycle analysis and evidence-based policymaking.

- Fills a critical data void: India is the world’s fifth-largest economy with a services-dominated structure, yet lacked a monthly services output indicator — a significant statistical anomaly now corrected.

- Laspeyres methodology + OECD alignment ensures international comparability, credibility and eventual integration into global economic monitoring frameworks.

- GST data repurposing is innovative — converting tax-administrative data into national statistics demonstrates data governance maturity and reduces survey burden on firms.

- Trial phase before regular release is methodologically sound — allows stakeholder feedback, methodology validation and resilience testing before the index informs high-stakes policy decisions.

- Deflator limitation: Using CPI as a proxy for SPPIs introduces measurement error — consumer prices and producer prices can diverge significantly, especially in B2B services (IT, logistics, finance). This is acknowledged by MoSPI as a limitation.

- Informal sector exclusion: ISP covers only the formal, incorporated services sector. India’s vast informal services economy (self-employed professionals, gig workers, unregistered traders) remains invisible — limiting macroeconomic completeness.

- Health & education gap: Two of India’s fastest-growing, most employment-intensive services sub-sectors are absent from the initial ISP, reducing its comprehensiveness in the short term.

- 60-day lag: The UK’s Monthly Index of Services is released within ~45 days — a tighter turnaround would improve the ISP’s policy relevance for real-time decisions.

- GST compliance variability: Sectors with lower or irregular GST filing compliance may introduce noise into sub-sectoral indices, requiring quality filters.

- Develop dedicated SPPIs for major sectors (IT, finance, telecom) to replace CPI proxies and reduce deflation-induced measurement errors.

- Integrate ASISSE data expeditiously to bring health and education into scope — the two biggest services employment drivers.

- Shorten the release lag progressively toward 40–45 days, in line with UK/EU standards, to improve real-time policy utility.

- Develop a Composite Activity Index combining ISP + IIP to provide a single high-frequency barometer of India’s entire formal economy.

- Explore alternative informal-sector proxies (UPI/digital payment flows, mobile data, enterprise surveys) to gradually widen coverage.

Q1. Consider the following statements about the Index of Services Production (ISP):

1. It is compiled using a fixed-weight Laspeyres volume index with 2024-25 as the base year.

2. It covers both formal and informal services sectors.

3. Health and education services are excluded from the initial ISP framework.

Which of the statements given above is/are correct?

Q2. (Assertion–Reasoning) Assertion (A): The ISP uses CPI as a deflator for most service sectors rather than Service Producer Price Indices (SPPIs). Reason (R): Comprehensive SPPIs are not available across most Indian service sectors, making CPI the only practical proxy.

A) Both A and R are true, and R is the correct explanation of A B) Both A and R are true, but R is NOT the correct explanation of A C) A is true, R is false D) A is false, R is trueQ3. The Technical Advisory Committee (TAC) constituted by MoSPI to develop the ISP framework was chaired by:

A) The Chief Economic Adviser, Ministry of Finance B) The Chief Statistician of India C) Ms. Debjani Ghosh, Distinguished Fellow, NITI Aayog D) The Governor, Reserve Bank of IndiaIndia–Australia Civil Nuclear Cooperation: Uranium Deal Operationalised

- The Third India–Australia Annual Summit (Melbourne, 9 July 2026) finalised the Administrative Arrangement under the India–Australia Civil Nuclear Cooperation Agreement, operationalising long-term exports of Australian uranium to India for peaceful purposes under IAEA safeguards.

- Australia holds the largest uranium reserves globally (>1/3 of global total) — making assured access a strategic fuel-security milestone for India’s expanding reactor fleet.

- The breakthrough was enabled by a pivotal domestic policy shift: India’s SHANTI Act (December 2025) opened the nuclear sector to private and foreign investment, addressing Australia’s long-standing governance concerns.

- Conceived by Dr. Homi J. Bhabha (1954) under the Department of Atomic Energy (DAE), the three-stage programme is designed around India’s resource reality: limited uranium but ~25% of world’s thorium reserves (coastal sands of Kerala, Tamil Nadu, Andhra Pradesh and Odisha).

| Stage | Technology | Fuel | Status |

|---|---|---|---|

| Stage 1 | Pressurised Heavy Water Reactors (PHWRs) | Natural uranium; produces plutonium as byproduct | Operational (most Indian reactors) |

| Stage 2 | Fast Breeder Reactors (FBRs) | Plutonium from Stage 1; breeds uranium-233 from thorium blankets | PFBR at Kalpakkam: first criticality 6 April 2026 |

| Stage 3 | Advanced Heavy Water Reactors (AHWRs) | Thorium + uranium-233 | R&D stage |

- Australian uranium directly fuels Stage 1 PHWRs — the workhorse of India’s current nuclear fleet. Plutonium produced feeds into Stage 2 FBRs.

- Thorium is not directly fissile — it must first be converted into fissile uranium-233 via neutron absorption inside a reactor. This is the bridge role of Stage 2 FBRs.

- 1974 Pokhran test: India’s “Peaceful Nuclear Explosion” triggered international backlash; the Nuclear Suppliers Group (NSG) was created to restrict nuclear trade with non-NPT states.

- 1998 Pokhran II: Further sanctions, but eventually forced global recognition of India’s unique position. Led to the landmark India–US Civil Nuclear Agreement (123 Agreement, 2008) and India’s NSG waiver (2008) — breaking nuclear isolation without NPT membership.

- 2010: Australia refused uranium sales citing India’s non-membership of the Nuclear Non-Proliferation Treaty (NPT). 2012: Australia reversed policy. September 2014: Civil Nuclear Cooperation Agreement signed; entered into force November 2015.

- 9 July 2026: Administrative Arrangement finalised at Melbourne Summit — moves the 2014 Agreement from policy intent to operational, commercial reality.

- SHANTI Act, December 2025 (Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India): Historic departure from NPCIL monopoly — enables Indian private companies and joint ventures to build, own and operate nuclear power plants, addressing Australia’s governance concerns and attracting global investors.

- Establishes implementing procedures for the 2014 Civil Nuclear Cooperation Agreement, enabling long-term uranium supply contracts between Australian exporters and Indian state/private entities.

- All uranium supplied remains under IAEA safeguards (India-specific safeguards agreement) — no diversion to military use permitted.

- Australia under its own policy exports uranium only to countries covered by a civil nuclear cooperation agreement — India now fully qualifies.

- Australia reaffirmed support for India’s membership of the NSG — a diplomatic outcome with long-term significance.

- Broader summit outcomes included cooperation in maritime security, cyber, critical technologies, skill development and reaffirmation of the Comprehensive Strategic Partnership.

- Fuel diversification: India currently imports uranium from Russia, Kazakhstan, Canada, Namibia and Uzbekistan. Australian supply adds a politically stable, Quad-aligned source — reducing geopolitical concentration risk.

- Clean energy alignment: Nuclear is low-carbon baseload; assured fuel supply supports India’s Panchamrit pledges (COP26) — 500 GW non-fossil capacity by 2030 and net-zero by 2070.

- SHANTI Act + uranium security: Assured long-term supply gives investors confidence to commit capital under the new private-sector licensing regime.

- PFBR milestone: 500 MWe Prototype Fast Breeder Reactor at Kalpakkam achieved first criticality on 6 April 2026 — inaugurates Stage 2 and demonstrates India’s FBR capability globally.

- SMRs: Up to 300 MWe each; factory-based manufacture; faster construction; 5 indigenous SMRs by 2033; ₹20,000 crore (Budget 2025-26).

- Quad strategic dimension: Deepens India–Australia Comprehensive Strategic Partnership, complementing the Quad’s Indo-Pacific security architecture; Australia’s decision implicitly recognises India’s strong non-proliferation record.

- Energy security multiplier: Assured long-term uranium reduces supply-chain vulnerability — India cannot reach 100 GW nuclear by 2047 without diversified, stable fuel sources.

- Strategic trust signal: Operationalising a 12-year-old agreement demonstrates the depth of India–Australia strategic partnership and India’s growing stature as a responsible nuclear power.

- Private sector integration: SHANTI Act + uranium assurance creates conditions for genuine commercial nuclear investment — a structural reform that no previous government had achieved.

- NPT exclusion persists: India remains outside the NPT. Full NSG membership is still blocked (primarily by China’s objections) — limiting India’s access to some advanced nuclear technologies on commercial terms.

- Nuclear liability overhang: The Civil Liability for Nuclear Damage Act, 2010 placed supplier liability that deterred US and Western reactor vendors. The extent to which SHANTI Act resolves this for international vendors remains to be tested in practice.

- Workforce and regulatory bandwidth: Scaling from 8.78 GW to 100 GW requires massive parallel construction — India’s nuclear workforce and regulatory capacity are not yet commensurate with this ambition.

- Thorium timeline: Stage 3 (thorium utilisation) remains decades away. Import dependency on uranium will persist for the foreseeable future, making diplomatic supply management critical.

- Accelerate NSG membership through diplomatic engagement — full membership would unlock technology and fuel access without case-by-case waivers.

- Fast-track PFBR commercialisation at Kalpakkam to validate India’s FBR capability and build international credibility for Stage 2.

- Clarify liability provisions under SHANTI Act to attract US, French and South Korean reactor vendors whose participation is essential for the 100 GW target.

- Build strategic uranium reserves using assured Australian supply to insulate India from geopolitical supply shocks.

- Invest in nuclear workforce development — dedicated engineering institutions and NPCIL/BHAVINI human capital expansion.

Q1. Which of the following is the correct chronological sequence of milestones in India–Australia nuclear cooperation?

1. Australia reverses policy on uranium sales to India

2. Civil Nuclear Cooperation Agreement signed

3. Agreement enters into force

4. Administrative Arrangement finalised

Q2. Consider the following statements about India’s Three-Stage Nuclear Programme:

1. Stage 1 uses Pressurised Heavy Water Reactors (PHWRs) fuelled by natural uranium.

2. Stage 2 Fast Breeder Reactors (FBRs) use thorium directly as their primary fuel.

3. India’s thorium reserves are found primarily in coastal sands.

Which are correct?

Q3. Match List I (Technology / Act) with List II (Description):

A. PFBR, Kalpakkam B. SHANTI Act C. SMR

1. Enables private sector entry into nuclear power plant ownership and operation

2. Up to 300 MWe; compact factory-based manufacture; 5 to be operational by 2033

3. 500 MWe prototype; first criticality April 2026; marks Stage 2 of three-stage programme

India–Maldives FTA: First Round of Negotiations Concludes Successfully

- The first round of India–Maldives Free Trade Agreement (IMFTA) negotiations concluded successfully in virtual mode (29 June–7 July 2026), covering 8 technical sessions across 8 policy areas; broad convergence reached on several issues.

- India’s Chief Negotiator: Ujjwal Kumar Ghosh, Joint Secretary, Department of Commerce. Maldives’ Chief Negotiator: Yusuf Riza.

- On 8 July 2026, Commerce Minister Piyush Goyal met Maldivian Minister Mohamed Saeed to review progress; both sides reaffirmed commitment to conclude both the FTA and the Bilateral Investment Treaty (BIT), marking 60 years of diplomatic relations.

- The Republic of Maldives is an archipelago of 1,200+ islands in the Indian Ocean, strategically located on the 8° and 9° Channels — critical Sea Lines of Communication (SLOCs) connecting the Persian Gulf, India and Southeast Asia.

- India’s Neighbourhood First Policy and the SAGAR doctrine (Security and Growth for All in the Region) identify the Maldives as a priority partner in the Indian Ocean Region.

- India has been a first responder in Maldivian crises: Operation Cactus (1988) foiled an armed coup attempt; COVID-19 medical assistance (2020); recurring economic bail-out packages.

- Existing trade framework: A trade agreement signed in 1981 covers essential commodity exchanges (food, medicine, building materials) — the IMFTA will be a far more comprehensive successor.

- The IMFTA was first announced during President Mohamed Muizzu’s visit to India in 2024; Terms of Reference (ToR) were finalised before Round 1. A Bilateral Investment Treaty (BIT) is being negotiated in parallel.

- Goes beyond tariff reduction to cover: market access (goods & services), investment facilitation, digital payments (UPI/RuPay already operational in Maldives), tourism, MSMEs, startups, blue economy, fisheries and renewable energy.

- Both sides are working towards a “broad-based, balanced and comprehensive agreement guided by fairness and reciprocity.”

- Parallel track: the BIT provides legal protection to investors — precedent of concluding both simultaneously set by the India–UAE CEPA (2022).

- India’s FTA portfolio: implemented agreements with ASEAN, Japan, South Korea, Sri Lanka, Nepal, Bhutan, UAE (CEPA 2022), Australia (ECTA 2022 interim); India–UK FTA under negotiation.

- The IMFTA would be India’s first FTA with a Small Island Developing State (SIDS) — a novel template with potential replication for other Indian Ocean island nations.

- FTA vs. CEPA vs. CECA: FTA primarily covers tariffs on goods → CEPA adds services and investment → CECA is broadest (all pillars including IPR, digital trade).

- India’s Model BIT (2016): India terminated 50+ older BITs post-2016 and now negotiates from a more restrictive template — Maldives may seek stronger investor protections than India is typically willing to offer.

- Strategic imperative: Maldives’ SLOC location makes deep economic integration a security and diplomatic necessity — economic interdependence as a hedge against Chinese strategic penetration in the Indian Ocean.

- Natural complementarity: India’s large consumer market complements Maldives’ tourism, fisheries and services strengths — a mutually reinforcing trade structure.

- Digital integration: UPI adoption in Maldives already underway — FTA provides the legal superstructure for deeper fintech and digital payment cooperation.

- Economic diversification for Maldives: Reduces Maldivian mono-sectoral (tourism) vulnerability — aligns with their economic resilience goals.

- Trade imbalance risk: India’s exports (USD 458 mn) significantly exceed Maldivian exports (USD 313 mn). Without careful structuring, an FTA may worsen the asymmetry and fuel domestic Maldivian political backlash.

- Non-tariff barriers persist: Maldives lacks production scale — even zero-tariff access may not boost Maldivian exports if supply-side constraints (skilled labour, infrastructure, logistics) remain unaddressed.

- Geopolitical volatility: The Muizzu government initially pursued an “India Out” posture before recalibrating — future political shifts in Malé could stall or reopen negotiated terms.

- Fisheries sensitivity: Indian fishing communities compete with Maldivian fishers in some species — this politically sensitive sector requires careful, phased negotiation.

- BIT complexity: India’s restrictive Model BIT (2016) may create friction with Maldives’ investor protection expectations.

- Pace vs. quality tension: Aim to sign by end-2026 is ambitious — rushing text can compromise domestic stakeholder consultation and create implementation problems later.

- Include robust Rules of Origin to prevent treaty-shopping (third-country goods entering India via Maldives using duty preferences).

- Dedicate a capacity-building chapter to address Maldivian supply-side constraints so trade flows become genuinely bidirectional, not just one-directional.

- Negotiate the fisheries chapter with domestic industry consultation and phase-in periods to manage political sensitivity on both sides.

- Conclude the FTA and BIT simultaneously for a comprehensive economic architecture — following the India–UAE CEPA precedent.

- Anchor the FTA to UPI/digital payment framework and renewable energy cooperation (Maldives has net-zero by 2030 ambitions) for strategic depth beyond traditional trade.

Q1. Consider the following statements about the India–Maldives FTA negotiations (2026):

1. The first round was held in New Delhi in physical format.

2. India is the second-largest trading partner of the Maldives.

3. Both the FTA and the Bilateral Investment Treaty are being negotiated.

Which are correct?

Q2. ‘Operation Cactus’ is associated with:

A) India’s peacekeeping operation in Sri Lanka under IPKF B) India’s military intervention to foil a coup attempt in the Maldives C) Counter-piracy operations by the Indian Navy in the Gulf of Aden D) India’s first nuclear test at PokhranQ3. Which of the following best distinguishes a CEPA from a simple FTA?

A) CEPA applies only to goods; FTA covers services too B) CEPA covers goods, services, and investment; FTA primarily focuses on goods trade C) CEPA is a multilateral agreement; FTA is bilateral only D) CEPA is concluded under WTO supervision; FTA is purely bilateral