Content

- From Grassroots to Glory

- 11 Years of PM Jan Dhan Yojana: Banking the Unbanked

From Grassroots to Glory

Background: Sports as a Nation-Building Tool

- Sports in India historically underplayed compared to education, politics, and economy.

- Shift since 2014: sports as governance priority → youth empowerment, health, and national pride.

- India’s demographic advantage: 65% population under 35 years – sports policy aligned with demographic dividend.

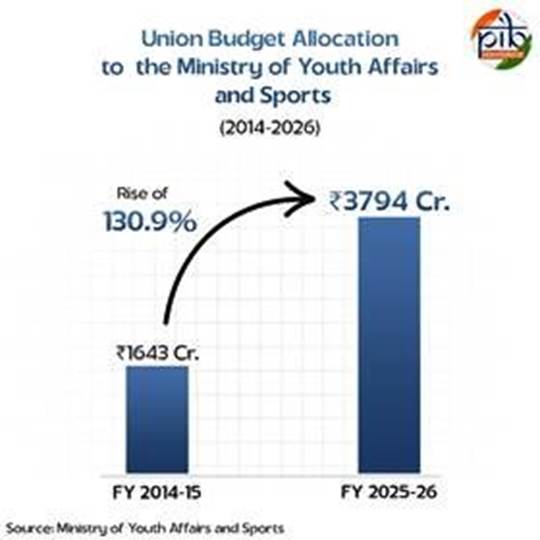

- Budget allocation surge: ₹1,643 crore (2014–15) → ₹3,794 crore (2025–26) (↑130.9%).

Relevance : GS 2 (Governance, Schemes)

Policy Vision: Sports in Viksit Bharat 2047

- Youth-centric approach: Sports as a pillar of Naya Bharat.

- Integration with education (NEP 2020) and lifestyle (Fit India → Jan Andolan).

- Goal:

- Olympics 2036 → India as host nation.

- Top-10 sporting nation by 2036.

- Top-5 sporting nation by 2047.

Key Government Schemes & Initiatives

Sports Authority of India (SAI)

- Apex body for sports excellence & grassroots promotion.

- Functions:

- Talent scouting & nurturing.

- Scientific training & international exposure.

- Infrastructure development (stadia, shooting range, academies).

- Support to flagship schemes – Khelo India, TOPS, Fit India.

Khelo Bharat Niti 2025 (new)

- Paradigm shift – sports as career + national movement.

- Integrates NEP 2020 with sports education.

- Focus:

- Early talent ID via KIRTI.

- Grassroots + elite infrastructure.

- National aspiration: Olympic bid 2036.

Khelo India Programme (2016–17)

- Mass participation + excellence focus.

- Key outcomes:

- 328 infra projects worth ₹3,151 crore.

- 1,045 Khelo India Centres (KICs).

- 34 State Centres of Excellence (KISCEs).

- 306 accredited academies.

- 2,845 athletes supported (₹10,000/month stipend, coaching, medical care).

KIRTI (Khelo India Rising Talent Identification)

- Talent ID for ages 9–18.

- Uses AI, data analytics, standardized protocols for fair selection.

- 174 Talent Assessment Centres (TACs) operational.

- Long-term aim: sustainable athlete pipeline for Olympic-level success.

Target Olympic Podium Scheme (TOPS)

- Elite athlete funding (customized training, exposure).

- Monthly support:

- Core athletes → ₹50,000.

- Development athletes → ₹25,000.

- Beneficiaries: 174 individual athletes + 2 hockey teams (Men & Women).

- Proven success: India’s medals in Tokyo 2020 (7) & Paris 2024 (6).

Fit India Movement (2019)

- Mass fitness → lifestyle change.

- “Ek Ghanta Roz” campaign (NSD 2025 theme).

- Family-centric sessions, expert-led awareness.

Other Schemes

- Assistance to NSFs: strengthens national federations (training, hosting events, hiring coaches).

- National Sports University (2018, Manipur): hub for sports sciences, tech, management, coaching.

- National Sports Awards: Recognition & motivation (Rajiv Gandhi Khel Ratna → Major Dhyan Chand Khel Ratna).

- Pension & Welfare Schemes: ₹12k–₹20k monthly pension, up to ₹10 lakh financial support for retired/hardship athletes.

- National Sports Development Fund (NSDF): CSR, NRI, philanthropy contributions.

- NCSSR (2017): Sports science & medicine, budget ₹260 crore till 2025–26.

Landmark Reform: National Sports Governance Act 2025

- Introduced Aug 18, 2025.

- Objectives: Transparency, accountability, athlete welfare.

- Key features:

- Athlete representation & gender inclusion mandatory.

- Safe Sports Policy – protects women, minors, vulnerable athletes.

- Code of Ethics (aligned with IOC/IPC norms).

- Internal grievance redressal mechanism in all sports bodies.

- Age & tenure limits for office bearers (70–75 yrs conditional relaxation).

- RTI applicability – sports bodies treated as public authorities.

- Professional sports administrators (not just retired judges) to resolve crises.

India’s Sporting Journey (Olympics Performance)

- Rio 2016: 117 athletes → 2 medals.

- Tokyo 2020: 124 athletes → 7 medals.

- Paris 2024: 117 athletes → 6 medals.

- Icons: Neeraj Chopra (1st Olympic athletics gold), Mirabai Chanu (multiple medals).

- Trend: Growing medal tally, diversified disciplines, improved global presence.

Social & Cultural Dimension

- Major Dhyan Chand: Hockey legend, National Sports Day inspiration.

- Olympic & Paralympic values: Excellence, Respect, Equality, Courage.

- Sports → youth discipline, fitness, national integration, soft power.

- “From pastime → profession → diplomacy tool”.

Challenges & Way Forward

- Grassroots penetration: ensuring rural & tier-2/3 cities get infra & coaching.

- Gender disparity: bridging participation gaps, ensuring safety.

- Sustainability of funding: private sector partnerships via NSDF critical.

- Scientific ecosystem: expand NCSSR model nationwide.

- Olympic 2036 ambition: requires global-scale infra, governance credibility, and mass athlete pipeline.

- Cultural shift: Sports must become “mainstream career” comparable to education/professions.

Conclusion

- India’s sports ecosystem is undergoing systemic, athlete-centric transformation.

- From Khelo India → Khelo Bharat Niti 2025 → Governance Act 2025, reforms integrate grassroots to elite.

- With a demographic dividend, scientific support, and transparent governance, India is positioned for a leap from sporadic success to sustained global excellence.

- By 2036 (Olympic bid) and 2047 (Viksit Bharat), India envisions itself as a sporting superpower—where sports are not just medals, but also nation-building, youth empowerment, and global leadership.

11 Years of PM Jan Dhan Yojana: Banking the Unbanked

Background: Why Financial Inclusion was Needed

- Pre-2014 scenario:

- 40%+ Indians unbanked, esp. in rural/semi-urban areas.

- Dependence on informal moneylenders → high interest debt traps.

- Lack of access to credit, insurance, pensions, DBT, digital payments.

- Policy Push (2014 onwards):

- PMJDY launched (28 Aug 2014) as National Mission for Financial Inclusion.

- Motto: Banking the Unbanked, Securing the Unsecured, Funding the Unfunded, Serving the Unserved & Underserved.

Relevance : GS 2(Governance , Schemes) , GS 3(Indian Economy)

Core Tenets of PMJDY

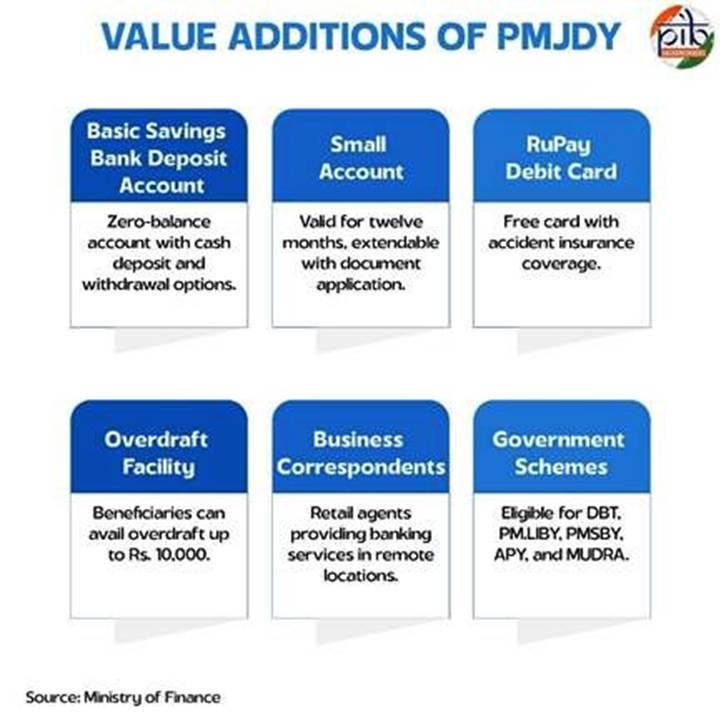

- Banking the Unbanked:

- Basic Savings Bank Deposit Accounts (BSBDA) with zero balance, minimal KYC, e-KYC, account opening in camps.

- Securing the Unsecured:

- Free RuPay debit cards with accident insurance (₹2 lakh after Aug 2018; earlier ₹1 lakh).

- Funding the Unfunded:

- Overdraft facility (up to ₹10,000).

- Access to micro-credit, micro-insurance, micro-pensions.

- Financial Integration:

- Direct Benefit Transfers (DBT), linking to other schemes – PMJJBY, PMSBY, APY, MUDRA.

Key Features of Accounts

- BSBDA (Basic Savings Bank Deposit Account):

- No minimum balance, 4 withdrawals/month, via bank/ATM/BCs.

- Small Accounts / Chota Khata:

- For citizens without valid KYC; valid for 12 months + 12-month extension with proof of applied documents.

- RuPay Debit Card:

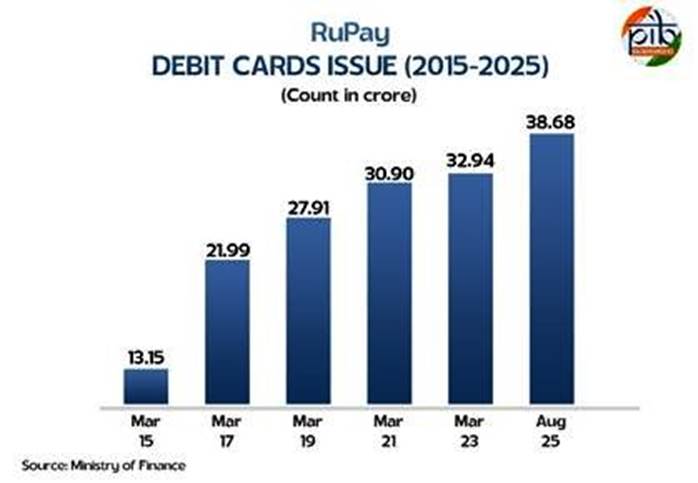

- 38.68 crore issued till 2025.

- Enabled digital payments, accident cover, cashless transactions.

- Overdraft Facility:

- Contingency support up to ₹10,000 (esp. for women).

- Business Correspondents (BCs)/Bank Mitras:

- Last-mile banking agents in villages → deposits, withdrawals, mini-statements.

Achievements in 11 Years (2014 → 2025)

- Account Growth:

- 14.72 crore (2015) → 56.16 crore (Aug 2025).

- ~67% rural/semi-urban, 33% urban/metro.

- Women Empowerment:

- 56% accounts held by women (nearly 30 crore women beneficiaries).

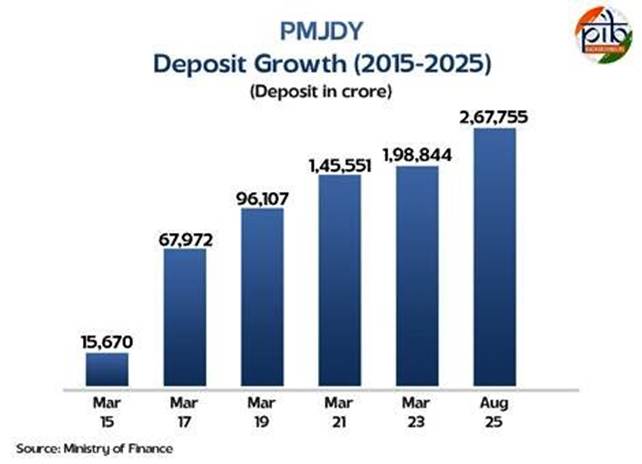

- Deposits Growth:

- ₹15,670 crore (Mar 2015) → ₹2.67 lakh crore (Aug 2025).

- RuPay Cards:

- 38.68 crore issued, pivotal in digital payment adoption.

- Direct Benefit Transfer (DBT):

- Linked with 327 schemes → leakage reduction, subsidy efficiency.

- Financial Literacy & Camps (2025 Saturation Drive):

- 99,753 camps held (July 2025).

- 6.6 lakh new PMJDY accounts, 22.65 lakh new enrollments in PMJJBY/PMSBY/APY.

- 4.73 lakh inactive accounts reactivated.

PMJDY’s Transformative Impact

- Financial Ecosystem Backbone:

- DBT pipeline for LPG subsidy (PAHAL), MGNREGA, PM-KISAN, pensions, scholarships.

- Gender Empowerment:

- Women get control over savings, pensions, and insurance.

- Reduced dependence on moneylenders.

- Digital Economy Boost:

- RuPay cards + UPI adoption → India leads in global real-time payments (40%+ of world’s volume).

- Social Equity:

- Access for marginalized groups (migrant workers, rural poor, unorganised sector).

- Trust in Formal Banking:

- Deposits growth shows behavioural shift → poor saving in banks, not cash-at-home.

Global Recognition

- Guinness World Record (2014):

- 18,096,130 bank accounts opened in one week → world record.

- World Bank & IMF:

- Recognize PMJDY as largest financial inclusion drive globally.

Challenges & Gaps

- Dormant/Inactive Accounts: Still ~15–20% accounts inactive.

- Overdraft Utilisation Low: Fear of repayment, lack of awareness.

- Financial Literacy Deficit: Many account holders don’t fully use facilities (credit/insurance).

- Digital Divide: Rural women, elderly, less-educated find digital transactions difficult.

- Banking Correspondent Sustainability: Low remuneration → high attrition.

Way Forward (2025 → 2047)

- Deepening Financial Services: Move beyond accounts → ensure access to credit, insurance, pensions.

- Women-Centric Financial Products: Special micro-savings, insurance for women SHGs.

- Digital + AI Empowerment: Fintech innovations to expand reach in remote areas.

- Strengthening BC Model: Better incentives, tech support for Bank Mitras.

- Financial Literacy Revolution: Village-level awareness + school curriculum integration.

- Universal Coverage by 2047: Every Indian with a bank account + digital footprint + financial product access.