Content

- Bengal second-lowest in convictions for crimes against women

- The future of the IMEC

- India’s Municipal Finance Crisis

- Meet AI chatbots replacing India’s call-centre staff

- The new power of rare earths

Bengal second-lowest in convictions for crimes against women

Why in News

- Trigger Event: An alleged gang rape of a medical student from Odisha in Durgapur (Oct 2025).

- Political Reaction: CM Mamata Banerjee’s remarks—suggesting girls should avoid going out at night—sparked public and Opposition backlash.

- Significance: The issue reopens debates on women’s safety, accountability, victim-blaming, and governance failure in West Bengal.

Relevance :

- GS 1: Social issues – women’s safety, gender inequality, victim-blaming, societal norms.

- GS 2: Governance & law – criminal justice system efficiency, role of police and judiciary, NCRB data analysis, implementation of Nirbhaya Fund schemes, fast-track courts.

Background Context

- Previous Incident (2024):

- A woman doctor was raped and murdered at R.G. Kar Medical College, Kolkata.

- The State government issued guidelines to limit women doctors’ night shifts, later withdrawn after Supreme Court criticism for gender discrimination.

- Current Case (2025):

- The victim, a medical student from Odisha, was allegedly gang-raped in Durgapur.

- Public anger intensified due to perceived pattern of administrative inaction.

Statistical Reality: Crime Against Women in West Bengal (NCRB Data 2018–2023)

| Indicator | West Bengal’s Status | Rank (India) | Trend/Observation |

| Crimes against women (annual average >30,000) | Very High | Top 4 | Consistent since 2018 |

| Acid attack & attempt to acid attack | Highest | 1st | 2021–2023 |

| Attempt to rape | Second highest | 2nd | Since 2019 |

| Cruelty by husband or relatives | High | 3rd (after Rajasthan & UP) | 2018–2023 |

| Conviction rate (avg. 2017–2023) | ~5% | 35th/36 States | Extremely poor |

| Conviction rate (2022 peak) | 8.9% | Still among lowest | Marginal improvement |

| Acquittals (2023) | >19,000 cases | Highest | Sharp increase from <8,000 |

| Pending trials (2023) | ~3.7 lakh cases | Highest | +56% rise since 2017 |

Core Issues Identified

- Low Conviction Rate:

- Reflects weak investigation, poor prosecution, and witness intimidation.

- Only 1 in 12 cases result in conviction (2022).

- High Acquittals & Pendency:

- Courts overburdened; lack of fast-track courts and forensic infrastructure.

- Delay → Justice Denied → Impunity.

- Systemic Gaps:

- Poor coordination between police and judiciary.

- Underreporting due to stigma and police apathy.

- Lack of victim support services and shelters.

Socio-Political Dimensions

- Governance Accountability:

- Opposition alleges failure of law and order.

- State government’s “zero tolerance” claim contradicted by data.

- Gender Sensitivity Deficit:

- Administrative response often patriarchal and moralistic.

- Instead of institutional reform, discourse shifts to individual behaviour.

- Judicial and Civil Society Response:

- Calcutta High Court and Supreme Court previously intervened in related cases.

- Civil society demands independent oversight and fast-track mechanisms.

Broader Context in India

- National Picture (NCRB 2023):

- India recorded 4.45 lakh crimes against women, a 4% rise over 2022.

- National conviction rate ~30%, West Bengal only ~5%, showing sharp contrast.

- Highlights state-level variation and policy implementation gaps.

Policy and Legal Framework

- Legal Safeguards:

- IPC Sections 354, 376, etc. (sexual assault & rape).

- Criminal Law (Amendment) Act, 2013 post-Nirbhaya.

- Nirbhaya Fund, One-Stop Centres, Women Helplines (181).

- Implementation in WB:

- Underutilization of central schemes.

- Weak forensic and police infrastructure despite repeated directives.

Way Forward

- Institutional Reforms:

- Establish state-level fast-track courts for gender crimes.

- Modernize forensic labs; integrate digital tracking of cases.

- Police Reforms:

- Increase women officers, sensitization training, and independent oversight.

- Victim Support Systems:

- Strengthen One-Stop Centres, psychological aid, and compensation mechanisms.

- Public Accountability:

- Transparent crime and conviction dashboards.

- Stronger civil society engagement in monitoring and advocacy.

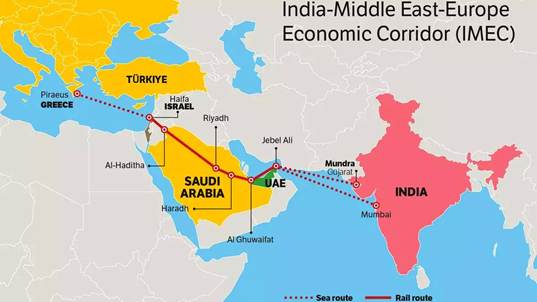

The future of the IMEC

Why in News

- Recent Context (Oct 2025):

- Rising trade frictions with the U.S. have prompted India to diversify trade partnerships with Europe, West Asia, and beyond.

- India is finalizing a trade deal with the U.K. and negotiating with the European Union.

- Simultaneously, renewed emphasis is on operationalizing the India–Middle East–Europe Economic Corridor (IMEC) — envisioned as a strategic trade and connectivity corridor linking India, the Gulf, and Europe.

- However, the West Asian instability post–Hamas attacks (Oct 2023) continues to threaten the corridor’s feasibility.

Relevance :

- GS 2: International relations – India–Middle East–Europe connectivity, trade corridors, I2U2 and multilateral frameworks, strategic autonomy.

- GS 3: Economic development – infrastructure, logistics, energy trade (hydrogen/electricity), supply chain resilience, China’s BRI comparison.

- GS 3: Security – regional stability in West Asia, maritime and cyber dimensions, alternative trade routes amid conflicts.

Background and Genesis

- Launch:

- Announced during the G-20 Summit in New Delhi (Sept 2023) in the presence of leaders from India, the U.S., Saudi Arabia, UAE, France, Germany, Italy, and the European Commission.

- Origin:

- Conceived within the I2U2 framework (India, Israel, UAE, U.S.) aimed at creating economic integration and infrastructure connectivity across Asia and Europe.

- Geopolitical Context:

- The Abraham Accords (2020) normalized Israel–Arab relations, enabling such a corridor proposal.

- Optimism in 2023 for regional peace created momentum for transnational infrastructure planning.

Vision and Structure of IMEC

- Objective: To establish a strategic multi-modal corridor enhancing connectivity between India, the Arabian Peninsula, and Europe.

- Components:

- Maritime Connectivity: Between Indian ports and Gulf ports (e.g., Dubai, Fujairah).

- Rail Connectivity: Linking UAE–Saudi Arabia–Jordan–Israel, culminating at Haifa Port on the Mediterranean.

- Sea Route: Haifa to European ports (e.g., Greece, Italy, France).

- Complementary Infrastructure:

- Clean hydrogen pipeline.

- High-voltage electricity cable.

- Undersea digital cable (telecom data link).

- Integrated logistics and port development.

Strategic Rationale for India

- Diversification Amid U.S. Trade Frictions:

- Reduce overdependence on U.S. markets; expand Europe–West Asia trade axis.

- Alternative to BRI:

- Offers a democratic, rules-based counterbalance to China’s Belt and Road Initiative (BRI).

- Energy and Logistics Security:

- Seamless energy transport (hydrogen, electricity).

- Faster supply chain integration with EU markets.

- Economic Opportunity:

- Europe is India’s largest trade partner ($136 billion trade, 2024–25); IMEC can reduce freight time and cost.

- Geopolitical Leverage:

- Enhances India’s strategic role in West Asia, cementing ties with Saudi Arabia, UAE, and Israel.

Key Geopolitical Developments Impacting IMEC

- October 7, 2023 – Hamas Attacks:

- Sparked Israel–Hamas conflict, destabilizing the entire West Asian region.

- Strained Israel’s ties with Gulf countries that were expected to anchor IMEC.

- Red Sea Crisis (2024–25):

- Houthi attacks on shipping disrupted Suez Canal trade routes, increasing global freight costs by 30–40%.

- Underscored the need for secure alternative corridors like IMEC.

- Arctic Route Competition:

- Melting ice caps have opened northern sea lanes, benefitting Russia, China, and the U.S., diverting trade from the Mediterranean.

- Hence, Italy and other Mediterranean economies see IMEC as crucial to retain relevance in global shipping.

Economic and Strategic Significance

- Trade and Connectivity:

- Reduces India–Europe freight time by up to 40% compared to Suez route.

- Creates interoperable logistics networks connecting Asia, Gulf, and Europe.

- Energy Transition:

- Facilitates clean hydrogen trade, aligning with India’s National Green Hydrogen Mission.

- Digital Integration:

- Undersea cables to enhance data and telecom linkages between India, West Asia, and Europe.

- Strategic Stability:

- Deepens India–Gulf strategic partnerships, reducing Pakistan’s influence in the region.

- Supply Chain Resilience:

- Supports “China+1” diversification, anchoring trusted value chains from India to Europe.

Challenges and Constraints

- Security Risks:

- Ongoing Israel–Hamas conflict, Iran–Saudi rivalry, and Houthi threats could derail regional transit stability.

- Political Uncertainty:

- Shifting U.S.–West Asia diplomacy and changing Arab public sentiments toward Israel.

- Infrastructure Gaps:

- Need for standardization of rail gauges, customs frameworks, and multimodal coordination.

- Financial Viability:

- High upfront cost (~$20–25 billion estimated). Requires multilateral investment and risk-sharing.

- Competition from Arctic and BRI Routes:

- Arctic route reduces Europe–Asia travel time by 40%.

- China’s BRI continues to dominate Eurasian logistics.

Diplomatic and Strategic Opportunities

- India–Europe Partnership Renewal:

- EU’s Global Gateway Initiative (2021) aligns with IMEC goals of sustainable infrastructure.

- India–Gulf Economic Integration:

- Deepening ties with Saudi Arabia and UAE under Comprehensive Economic Partnership Agreements (CEPAs).

- Regional Balancing:

- IMEC provides leverage for India’s strategic autonomy—collaborating with the West without antagonizing the Global South.

- Countering Pakistan’s Narrative:

- Strong India–Arab economic linkages marginalize Pakistan’s attempts at forming anti-India coalitions in West Asia.

Way Forward

- Institutionalizing IMEC:

- Establish a Permanent Coordination Mechanism among members.

- Integrate with I2U2 framework for technology and financing.

- Expanding Participation:

- Engage Egypt, Oman, and Qatar for greater regional integration.

- Focus on Dual Security–Economy Strategy:

- Combine maritime security cooperation with economic corridor development.

- Parallel Trade Diplomacy:

- Expedite FTA negotiations with EU and GCC to enhance market access.

- Public–Private Collaboration:

- Mobilize Indian corporates and Gulf sovereign funds for infrastructure financing.

India’s Municipal Finance Crisis

Context:

- Despite urban India generating nearly two-thirds of the national GDP, its municipalities control less than 1% of India’s total tax revenue.

- Core Issue:

The fiscal architecture of India’s federalism has left cities financially powerless — over-centralised, grant-dependent, and unable to self-finance essential services or issue credible municipal bonds.

Relevance :

- GS 2: Governance – fiscal federalism, 74th Constitutional Amendment, urban governance reforms, intergovernmental transfers.

- GS 3: Economy – municipal bonds, urban revenue generation, property tax reforms, urban infrastructure financing, public goods delivery.

- GS 1: Society – impact on citizens’ welfare, equitable access to urban services, participatory governance.

Background: India’s Urban Revenue Paradox

- Urban India’s Contribution: ~66% of GDP, yet <1% of tax powers.

- Post-GST Impact (2017):

- Municipalities lost ~19% of their own revenue sources (e.g., octroi, entry tax, local surcharges).

- Revenue powers were absorbed into the GST regime, making cities reliant on state and central transfers.

- Result:

- Revenue centralisation: States and Centre retain >95% of tax powers.

- Fiscal autonomy erosion: Cities became implementers, not governors.

How Did Cities Lose Fiscal Autonomy

- Centralisation of Taxes:

- GST subsumed local taxes without creating municipal compensation mechanisms.

- Weak Implementation of 74th Amendment (1992):

- Cities were to be “third tier of governance”, but remained administratively dependent on states.

- Conditional Grants:

- Funds come with strict conditions (e.g., AMRUT, Smart Cities Mission), limiting local discretion.

- Low Own-Revenue Base:

- Property tax contributes only 20–25% of total municipal revenues — politically sensitive and poorly assessed.

- User charges (water, waste, parking) underpriced or poorly collected.

- Creditworthiness Crisis:

- Ratings and RBI norms treat grants as “non-recurring income”, making cities appear fiscally weak.

The Problem: Flawed Model of Fiscal Federalism

- Inadequate:

- Cities lack predictable and untied revenues.

- Dependence on higher governments leads to fiscal uncertainty.

- Unjust:

- Burden shifted onto urban residents through user-pay logic — privatising public goods (water, sanitation, lighting).

- Penalises poorer households in informal settlements.

- Ideological Flaw:

- Treats grants as charity, not entitlements.

- Undermines the redistributive spirit of cooperative federalism.

Municipal Bonds — The “New Frontier” or a Mirage?

- Government Push:

- NITI Aayog, Finance Commission, and World Bank promote municipal bonds for infrastructure finance.

- Reality Check:

- Only a handful of cities (e.g., Pune, Ahmedabad, Indore) have successfully issued bonds.

- Low investor confidence due to:

- Weak financial transparency and audits.

- No stable, predictable revenue stream.

- Dependence on ad-hoc state/central grants.

- Credibility Problem:

- Current credit rating system judges cities narrowly by own revenue, ignoring grants and governance performance.

- This undervalues cities’ real fiscal position.

Why the Current Fiscal Prescription is “Inadequate and Unjust”

- Inadequate because:

- Property tax base too small and politically sensitive.

- Administrative weakness in assessment and collection.

- User charges regressive, hurting low-income groups.

- Unjust because:

- Converts collective goods into commodities (e.g., water, waste).

- Blames cities for inefficiency, while withholding fiscal authority.

- Residents pay more, yet get poor services due to funding shortfalls.

Comparative Perspective: Lessons from Scandinavia

- Denmark, Sweden, Norway Model:

- Cities can levy and collect income taxes directly.

- Enjoy predictable intergovernmental transfers.

- Result: Transparent, accountable, and citizen-trusted local governance.

- Outcome:

- Decentralised fiscal power = efficient urban welfare states.

- Transfers treated as part of a shared fiscal ecosystem, not as discretionary charity.

The Indian Paradox

- Centralised Power, Decentralised Burden:

- Cities are expected to deliver on solid waste, housing, climate resilience, and digital infrastructure without funds.

- Revenue Inversion:

- Accountability lies at local level; fiscal power lies at central level.

- Creates a “democracy deficit” — local governments answerable to citizens but dependent on distant bureaucracies for funds.

The Way Forward

- Reimagine Fiscal Federalism:

- Recognize cities as equal fiscal entities, not beneficiaries.

- Mandate constitutionally guaranteed urban revenue-sharing.

- Reform Municipal Bonds Framework:

- Treat grants and shared taxes as legitimate income for creditworthiness.

- Allow GST compensation or state shares as collateral.

- Empower Local Taxation:

- Modernize property tax systems (GIS mapping, annual revision).

- Rationalize user charges while protecting low-income groups.

- Institutionalise Urban Transfers:

- Create Urban Finance Commissions at the state level.

- Link transfers to transparency, citizen participation, and audit compliance.

- Democratize Urban Governance:

- Strengthen ward committees and citizen budgeting.

- Shift from technocratic to participatory fiscal management.

Meet AI chatbots replacing India’s call-centre staff

Why is it in the News?

- A Reuters investigation (Oct 2025) highlighted how AI chatbots developed by Indian startups like LimeChat (Bengaluru-based) are transforming the customer service and IT outsourcing landscape.

- LimeChat claims its generative AI agents reduce workforce needs by 80%, signaling a major shift in India’s $283 billion IT and BPM (Business Process Management) sector.

- Raises questions on AI-led automation, employment security, and India’s readiness to manage large-scale technological disruption.

Relevance :

- GS 3: Science & technology – AI, automation, digital workforce, IT-BPM sector transformation.

- GS 2: Governance – policy responses to technological disruption, employment regulation, reskilling frameworks.

- GS 1: Society – youth employment, gendered workforce impact, social adaptation to AI disruption.

Background: India’s IT and Outsourcing Sector

- India = world’s back-office hub: Accounts for 52% of global outsourcing (NASSCOM, 2025).

- Contributes 7.5% to India’s GDP; employs over 5 million directly (2024).

- Major strengths: Cheap labour, English proficiency, and large skilled workforce.

- Now faces AI-led automation pressures, especially in routine jobs (customer care, payroll, technical support).

What is Happening: AI-Led Disruption

1. Rise of Conversational AI

- Global market projected to reach $41 billion by 2030, growing at 24% annually (Grand View Research).

- Startups like LimeChat, Haptik (Reliance-owned), and others are automating customer interactions via chatbots.

- AI agents can handle 70% of customer complaints today — aiming for 90–95% automation within a year.

2. Economic Model

- LimeChat’s service: ₹1 lakh/month automates work of 15 agents (~$1,130 = salary of 3 human staff).

- Sales growth: From $79,000 (2022) → $1.5 million (2024) (19x rise).

- Integrations with Microsoft Azure to enhance natural language processing and multilingual capabilities.

3. Automation Impact

- Jefferies (Sept 2025) forecast:

- 50% revenue hit for call centres.

- 35% hit for other back-office functions within 5 years.

- TeamLease Digital data:

- BPM sector hiring fell drastically:

- +1,77,000 (2021–22)

- +1,30,000 (2022–23)

- <17,000 (2023–24 & 2024–25).

- BPM sector hiring fell drastically:

- Workers report AI replacing human evaluators and call quality analysts.

- Increasing job insecurity among India’s 1.65 million BPM employees.

Policy and Governance Dimensions

1. Government Position

- PM Narendra Modi (Feb 2025): “Work does not disappear; its nature changes.”

- Official stance: AI’s impact on employment will be limited in the long run due to new job creation in AI coordination, design, and oversight.

- Lack of dedicated AI-labour impact assessment mechanism so far.

2. Expert Concerns

- Sumita Dawra (ex-Labour Secretary): Advocates for unemployment benefits & social security reforms during AI transition.

- Santosh Mehrotra (University of Bath): Warns that India lacks a policy game plan for workforce reskilling amid AI disruption.

3. Geopolitical/Economic Risks

- U.S. policies:

- 25% tax proposal on outsourcing users.

- $100,000 H-1B visa fee.

- Tariffs on tech services.

- Combined with AI automation, these pose a double shock to India’s IT exports.

Social Implications

- Youth employment crisis risk — fresh graduates face shrinking entry-level IT roles.

- Women disproportionately affected — many occupy back-office or voice-process jobs now being automated.

- Cultural dimension: Many employees, like “Megha,” conceal layoffs from families — indicating social stigma of tech job loss.

- Customer perspective: Despite AI’s efficiency, EY Survey (Aug 2024) found:

- 78% Indians still prefer human support online.

- 62% purchases influenced by AI — shows growing but cautious consumer acceptance.

Opportunities for India

Transition from “Back Office” to “AI Factory”:

- Focus on AI engineering, model fine-tuning, and data annotation.

- Potential to export AI expertise, similar to IT exports in 2000s.

Upskilling Imperative:

- Shift towards AI deployment engineers, process analysts, data trainers, and algorithm auditors.

- Need for AI literacy integration in higher education.

AI Governance Leadership:

- Develop frameworks for ethical AI use, employment impact assessments, and social security nets.

Challenges Ahead

- Skill mismatch: Current workforce not trained for generative AI, automation design, or supervision.

- Policy lag: No AI-specific labour transition strategy or unemployment insurance.

- Corporate risk: Over-automation may harm customer trust (as seen with Sweden’s Klarna “course correction”).

- Ethical and accountability issues: Chatbots providing incomplete or misleading responses (e.g., Knya case).

Conclusion

- India stands at a critical inflection point — balancing automation-led productivity with inclusive employment.

- If managed well: India can become the world’s AI deployment hub (“AI factory”).

- If mismanaged: Risk of technological unemployment, social disruption, and loss of demographic dividend.

- Requires a proactive policy mix — reskilling, social protection, ethical AI frameworks, and strategic public–private collaboration.

The new power of rare earths

Why is it in the News?

- Growing China’s dominance in rare earth elements (REEs) and its strategic leverage in global trade, especially amid US–China tensions.

- Rare earths are critical for clean energy, electronics, defense, and high-tech manufacturing, making them geopolitically sensitive.

- The news is timely due to:

- China’s export controls and potential supply restrictions.

- Global concerns about technological supply chain security.

- Rising strategic competition between China and the US in tech and defense sectors.

Relevance :

- GS 3: Economy – strategic minerals, critical raw materials for technology, EVs, renewable energy.

- GS 2: International relations – China’s dominance, US-China competition, Indo-Pacific mineral diplomacy, supply chain security.

- GS 3: Science & technology – green energy tech, EV batteries, high-tech manufacturing, rare earth metallurgy.

Basics: Rare Earth Elements (REEs)

- Definition: 17 metallic elements (15 lanthanides + scandium + yttrium) with high electrical conductivity, magnetic properties, and heat resistance.

- Applications:

- Electronics: smartphones, semiconductors, display screens.

- Renewable energy: wind turbines, EV batteries, magnets.

- Defense: fighter jets, missile guidance systems.

- Misnomer: Despite the name, REEs are not rare in the Earth’s crust but occur in low concentrations that make extraction economically challenging.

Global Reserves & Production (2021–2022)

- Reserves (in tonnes of REE equivalent content):

- Vietnam: 22,000

- Brazil: 21,000

- Russia: 12,000

- India: 6,90,000 (1st in land-based reserves)

- Australia: 42,000

- USA: 23,900

- Other countries: 42,000

- Production of Rare Earth Oxides (2020–2022):

- China: 180,000–210,000 tonnes → >50% of global production.

- USA: 25,000–28,500 tonnes.

- Australia: 14,500–15,900 tonnes.

- Others: Russia, Vietnam, Malaysia, Madagascar contribute smaller shares.

China’s Strategic Dominance

- Controls ~60–80% of global REE production and processing, creating a near-monopoly.

- Extracts and refines REEs at low costs due to:

- Vertical integration of mining, separation, and refining.

- Economies of scale and state subsidies.

- Leverages REEs as a geopolitical tool:

- Past examples: export restrictions to Japan (2010), potential leverage against the US and allies.

- Creates supply chain vulnerabilities for critical industries in Europe, US, Japan.

Challenges for Other Countries

- High extraction costs: REEs often in low concentrations, requiring environmentally intensive processes.

- Limited refining capability: Even countries with reserves (USA, Australia, India) rely on China for refining and separation.

- Geopolitical dependence: Western countries cannot easily replace Chinese REEs due to lack of infrastructure.

Global Market Dynamics

- Demand surge: Driven by EVs, wind turbines, electronics, and defense tech.

- China’s pricing power: Can influence global REE prices through:

- Export quotas

- Tariffs

- Technology partnerships and strategic stockpiling

- US & allied responses: Initiatives to develop domestic extraction and processing, e.g., Mountain Pass mine (USA), Australian ventures.

India’s Position

- India has 6,90,000 tonnes of REE reserves (notably in Odisha, Andhra Pradesh, and Karnataka).

- Challenges:

- Low extraction and refining capacity.

- Lack of commercial-scale processing plants.

- Opportunities:

- Partner with US, Japan, Australia to develop domestic REE value chain.

- Potential hub for strategic minerals in the Indo-Pacific supply chain.

Environmental and Regulatory Issues

- REE extraction is chemically intensive and environmentally risky, producing toxic waste.

- Countries need strict regulations and eco-friendly technologies for sustainable mining.

- China has historically prioritized economic output over environmental concerns, giving it cost advantage.

Impact on Global Economy and Geopolitics

- REEs are critical for green energy transition: EVs, wind turbines, batteries.

- Any supply disruption by China can affect:

- US and EU defense industries.

- EV and semiconductor manufacturing.

- Countries are increasingly investing in domestic REE projects and diversifying supply chains.