Headline Figure

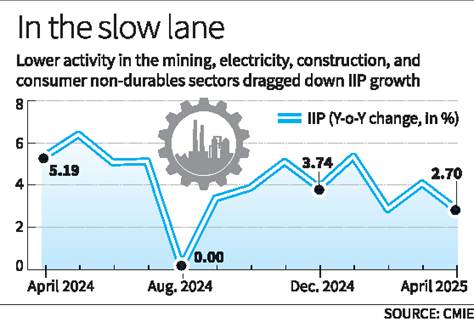

- IIP growth slowed to 2.7% in April 2025, an 8-month low.

- Last lower reading: 0.0% in August 2024 — suggests waning momentum.

Relevance : GS 3(Indian Economy)

Sector-wise Performance

- Mining & Quarrying:

- Declined by 0.2% (worst since August 2024).

- Indicates weak commodity extraction and upstream supply constraints.

- Electricity:

- Slower growth → possible lower power demand from industries or supply issues.

- Primary Goods & Infrastructure/Construction Goods:

- Weakness indicates sluggish investment and infrastructure activity.

- Consumer Non-Durables:

- Indicates muted rural or essential consumption.

- Reflects subdued demand for everyday goods, despite summer season.

Outlier Performance

- Capital Goods:

- Grew 20.3% in April 2025.

- However, base effect significant: April 2024 growth was only 2.81%.

- Still suggests private and public sector investment push or cyclical recovery in machinery output.

Concerns and Implications

- Broad-based slowdown across production-linked sectors hints at underlying demand weakness.

- Poor mining and electricity data may hurt core industries and downstream production.

- Weak consumer non-durables → possible rural distress or price sensitivity among consumers.

- Contradicts the capital goods surge, showing a mixed recovery picture.

Policy Relevance

- Monetary Policy Implication:

- Slower IIP may deter further rate hikes by RBI despite inflation concerns.

- Fiscal/Policy Focus:

- Government may need to accelerate capital expenditure and rural support measures.

- Focus on demand stimulation in consumer sectors.

Way Forward

- Address supply chain bottlenecks in mining and electricity.

- Sustain capital goods momentum through infrastructure pipeline.

- Monitor inflation-consumption balance to revive non-durable consumption.

- Ensure industrial recovery is broad-based and demand-driven, not just investment-led.