Content

- India’s Semiconductor Revolution

- National Cooperation Policy 2025

India’s Semiconductor Revolution

Semiconductors: The Strategic Core of Modern Electronics

- Semiconductors power everything: smartphones, satellites, electric vehicles, smart TVs, defence systems (e.g., Aakash-Teer).

- Function: Store, process, and transfer data using micro-scale transistors (millions to billions).

- Example: Chandrayaan-3’s Vikram Lander used Indian semiconductor tech & AI for autonomous landing.

Relevance : GS 3(Technology) ,GS 2(Governance)

Why Semiconductor Industry Matters Globally

- Geopolitical urgency: Global chip shortage post-COVID & Ukraine war crippled auto, telecom, and electronics industries.

- Concentration risk:

- Taiwan: 60% of global chip production; 90% of advanced chips.

- Strategic chokepoint → Geopolitical & economic vulnerability.

- Nations pushing self-reliant chip ecosystems: US, EU, Japan, South Korea, China.

India’s Strategic Entry into the Chip Race

- India seeks to tap the $1 trillion global chip market by 2030.

- Focus: End-to-end capability across design → fabrication → testing/packaging.

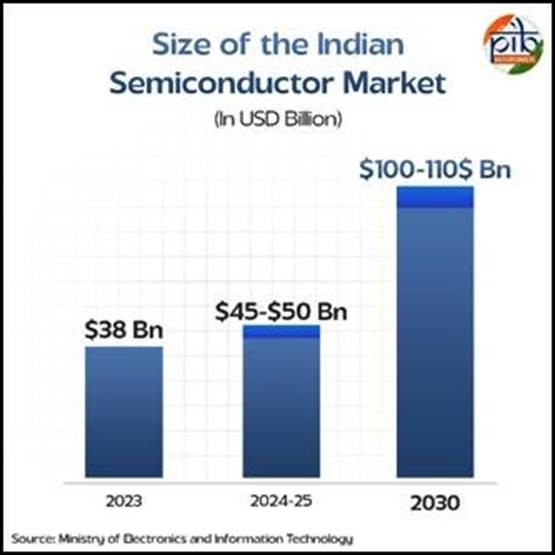

- Indian Market Size Projection:

- 2023: $38 billion

- 2025: ~$50 billion

- 2030: $100–110 billion

Key Initiatives Driving India’s Semiconductor Ambitions

India Semiconductor Mission (ISM)

- Launched: Dec 2021

- Outlay: ₹76,000 crore

- Objective: Position India as a global hub for electronics & chip design.

- Mission Pillars:

- Build fabs, packaging/testing units

- Enable design startups via EDA tools

- Create skilled engineers in VLSI, chip architecture

- Facilitate ToT & R&D hubs

- Secure supply chains: raw materials, gases, IP

Major Schemes Under ISM

| Scheme | Focus Area | Support Offered |

| Semiconductor Fabs Scheme | 28nm & below wafers | Up to 50% fiscal support |

| Display Fabs Scheme | AMOLED, LCD units | Up to 50% project cost |

| Compound Semiconductors & ATMP/OSAT | Packaging, photonics, sensors | Up to 50% capital support |

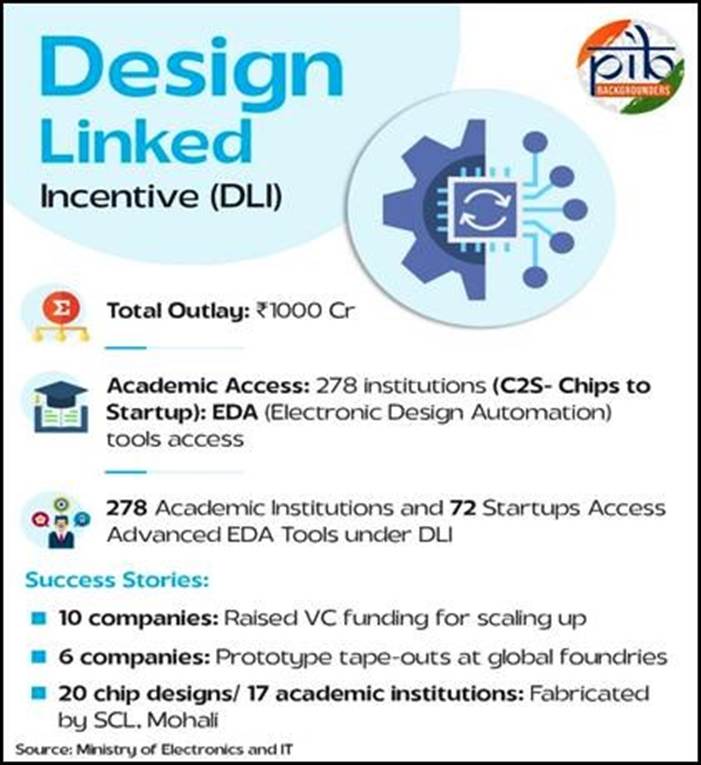

| Design Linked Incentive (DLI) | Chip design startups/MSMEs | ₹1000 Cr outlay, ₹15 Cr/company |

₹234 Cr already committed for 22 chip design projects (CCTV, mobiles, satellites, IoT, vehicles).

Skill Development & Talent Pipeline

- Target: Train 85,000 chip design engineers.

- AICTE curriculum for VLSI & IC manufacturing.

- SMART Lab (NIELIT Calicut): Trained 44,000 engineers.

- 100 institutes → 45,000+ students enrolled in chip design programs.

Collaborators: Lam Research, IBM, Purdue, Micron, IIT Roorkee, IISc.

Major Investments in India’s Semiconductor Infrastructure

| Company | Location | Investment | Output |

| Micron | Sanand, Gujarat | ₹22,516 Cr | ATMP Facility |

| Tata Electronics + PSMC | Dholera, Gujarat | ₹91,000 Cr | 50K wafers/month |

| CG Power + Renesas | Sanand, Gujarat | ₹7,600 Cr | 15M chips/day |

| TSAT (Tata) | Morigaon, Assam | ₹27,000 Cr | 48M chips/day |

| Kaynes Semicon | Sanand, Gujarat | ₹3,307 Cr | 6.33M chips/day |

| HCL–Foxconn JV | Jewar, UP | ₹3,700 Cr | 36M units/year |

May 2025: HCL–Foxconn approved to produce display driver chips (20K wafers/month capacity).

India’s First Advanced Chip Design Centres (May 2025)

- Locations: Noida and Bengaluru

- Focus: 3-nanometer chip design

- Significance: Pushing beyond previous 5nm & 7nm designs.

SEMICON India Programme

- Flagship platform to showcase India’s global chip ambitions.

- Editions:

- 2022: Bangalore

- 2023: Gandhinagar

- 2024: Greater Noida

- 2025: Sept 2–4, New Delhi (Yashobhoomi, IICC)

➤ Highlights of SEMICON India 2025

- 300+ exhibitors from 18 countries

- 4 International Pavilions: Japan, South Korea, Singapore, Malaysia

- 8 Country Roundtables for strategic collaboration

- Dedicated Workforce Development Pavilion – Target: 1 million new jobs by 2030

- Design Startup Pavilion to support innovation

- Participation from 9 State Governments (up from 6)

Recent Developments (2025 Highlights)

- First indigenous chip to enter production in 2025 (announced at Global Investors Summit).

- Netrasemi, a chip-design startup under DLI, raised ₹107 Cr VC funding.

- Madhya Pradesh launched its first IT hardware hub with ₹150 Cr investment, producing chips, drones, robotics hardware.

Strategic Impact and Way Forward

Strategic Leverage

- Reduces dependency on Chinese and Taiwanese chip ecosystem.

- Enhances India’s digital sovereignty, cyber-security, and economic competitiveness.

- Integral to programs like Digital India, defence modernization, and smart infrastructure.

Economic and Industrial Gains

- Create 1M skilled jobs by 2030.

- Add significantly to $300 billion electronics manufacturing goal by 2026.

- Position India as a global trusted supplier in chip value chain.

Challenges Ahead

- High capital intensity: Setting up a fab = ~$10B+ investment.

- Ensuring uninterrupted supply of ultrapure water, chemicals, rare earths.

- Global competition: Catching up with TSMC, Samsung, Intel in design/fab tech.

Conclusion

India’s semiconductor journey is transitioning from policy intent to production capability. With robust funding, strong partnerships, talent development, and strategic diplomacy, India is no longer just a consumer but a rising semiconductor power. From design to fabs, the India Semiconductor Mission is turning Bharat into the brain behind the chips.

National Cooperation Policy 2025

Contextual Backdrop: Why NCP 2025 Was Needed

- Last Policy Update in 2002: Became outdated in light of digitization, globalization, climate imperatives, and youth aspirations.

- Creation of Ministry of Cooperation (2021): Signaled renewed political and administrative focus on cooperatives.

- Participatory Drafting: 48-member Suresh Prabhu-led committee held 17 consultations and 4 regional workshops; gathered 648 stakeholder inputs from federations, state depts, experts.

Relevance : GS 2(Governance ) , GS 3(Cooperatives)

India’s Cooperative Landscape (2025 Snapshot)

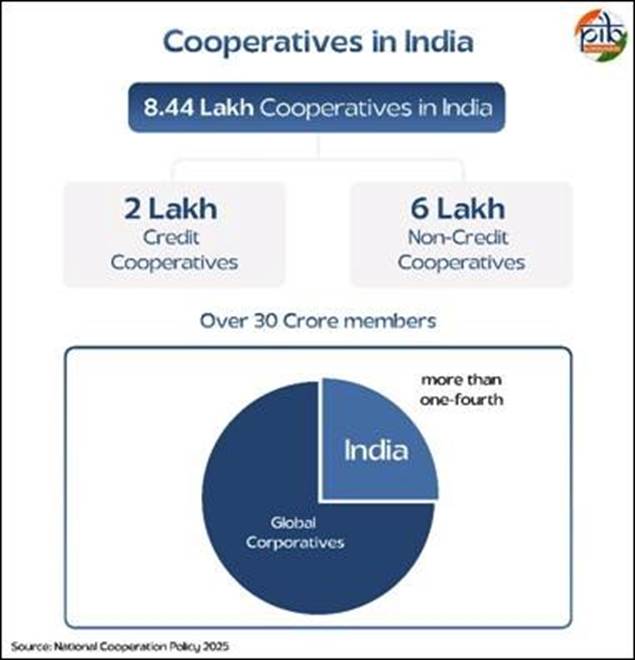

- 8.44 lakh cooperatives, of which:

- ~2 lakh credit cooperatives (PACS, UCBs)

- ~6 lakh non-credit cooperatives (dairy, fisheries, housing, etc.)

- 30+ crore members (largest cooperative membership globally).

- India accounts for >25% of the world’s cooperatives.

- Massive footprint in agriculture, rural finance, housing, and marketing.

Vision & Mission

- Vision: Enable cooperatives to power India’s transformation into Viksit Bharat by 2047 through Sahkar-se-Samriddhi.

- Mission: Build legal, financial, and tech ecosystems to make cooperatives professional, transparent, inclusive, and market-ready.

Six Strategic Pillars – Foundation of NCP 2025

- Strengthening Foundations: Legal reform, digital records, governance, PACS revival.

- Promoting Vibrancy: Model cooperative villages, branding, cluster development.

- Future-Readiness: Cooperative stack, ONDC-GeM integration, tech incubators.

- Inclusive Growth: Gender, SC/ST, youth representation and model bye-laws.

- Sectoral Diversification: Cooperatives in health, clean energy, waste, logistics.

- Youth for Cooperatives: HEI curricula, digital literacy, employment exchange.

Legal and Institutional Reforms

- Encourage states to align State Cooperative Societies Acts with NCP vision.

- Digital registries: Real-time cooperative tracking to reduce fraud, enhance governance.

- Institutional revival package for sick cooperatives.

Financial Empowerment

- Strengthen 3-tier rural credit structure: PACS → DCCB → SCB.

- Push for umbrella organizations like National Urban Cooperative Finance Corp.

- Government business eligibility for cooperative banks: Pensions, DBTs, subsidies.

Model Cooperative Village & Rural Cluster Strategy

- One model cooperative village per State/UT encouraged.

- Cooperative-led clusters in honey, spices, silk, dairy, tea, etc.

- Promotion of “Bharat Brand” for cooperative goods (national brand strategy).

Digital Tech & Future-Readiness

- National Cooperative Stack: Seamless integration with AgriStack, ONDC, and GeM.

- Promote e-commerce platforms for cooperative products.

- Establish Cooperative Innovation Hubs and Centres of Excellence.

Inclusivity Measures

- Model Bye-laws for SC/ST, women, and PwD inclusion in boards.

- Launch of awareness campaigns in schools and colleges.

- Gender quotas and capacity-building schemes for underrepresented groups.

Sectoral Expansion into New-Age Areas

- NCP 2025 seeks to embed cooperatives into:

- Clean energy (solar, biogas, ethanol)

- Waste management (solid, liquid, e-waste)

- Health & Education (school, diagnostic cooperatives)

- Gig-economy aggregators (plumber, taxi, delivery services)

- Organic/Natural farming, food processing, e-logistics

Youth-Oriented Cooperative Ecosystem

- University-level cooperative courses with UGC/AICTE integration.

- National Cooperative Employment Exchange (digital job portal).

- Recruit skilled trainers in finance, marketing, governance for cooperatives.

- Boost digital and financial literacy among rural youth.

Implementation & Monitoring Architecture

- 3-tier governance for policy rollout:

- Implementation Cell (Ministry of Cooperation) – with PMU support.

- National Steering Committee – chaired by Union Minister.

- Policy Monitoring Committee – led by Cooperation Secretary.

- Action plan with timelines – awaited; states to be roped in through MoUs and convergence mechanisms.

Why NCP 2025 Is Transformational

| Parameter | Legacy Cooperative Model | NCP 2025 Shift |

| Governance | Outdated, manually recorded | Real-time, digital, transparent |

| Focus | Agriculture-centric | Multi-sectoral & innovation-driven |

| Inclusivity | Limited representation | Gender, youth, SC/ST focus with model laws |

| Role in economy | Rural support only | Growth engine in Viksit Bharat strategy |

| Tech Integration | Minimal | Stack-driven, ONDC + GeM + AI-led |

Critical Evaluation

Strengths

- Holistic and future-ready: Legal + Digital + Social inclusion.

- Youth engagement and gender justice embedded.

- Serious effort to mainstream cooperatives into national economy.

Challenges

- Centre–State friction: Cooperatives fall under Entry 32, State List.

- Capacity constraints in Tier-2/Tier-3 cooperatives.

- Need for robust data infrastructure and regulatory convergence.

- Sustained financing of tech upgrades and HR capacity.

Conclusion

The National Cooperation Policy 2025 is not merely an update; it is a reimagination of India’s cooperative sector — from marginal rural support to a pillar of Viksit Bharat 2047. By fusing democratic participation with digital innovation and economic competitiveness, it offers a blueprint for inclusive, bottom-up growth. If implemented with Centre-State synergy, it can transform cooperatives into India’s second engine of growth.