Content

- India: A Global Bioeconomy Powerhouse

- GST Reforms 2025: Relief for Common Man, Boost for Businesses

India: A Global Bioeconomy Powerhouse

Growth Trajectory

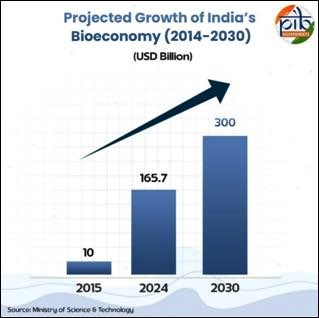

- Expanded from USD 10 bn (2014) → USD 165.7 bn (2024).

- CAGR: ~35% over the decade, contributing 4.25% of GDP.

- Target: USD 300 bn by 2030, USD 1.4–2.7 tn by 2050 (6.5–12% of GDP).

- Global context: Bioeconomy expected to hit USD 30 tn by 2050 (12% of world GDP).

Relevance :

- GS III (Economy, S&T, Environment) – Biomanufacturing, energy independence, innovation ecosystems.

- GS II (Governance) – Policy initiatives like BioE³, regulatory frameworks.

- GS I (Geography & Society) – Regional contribution, rural bio-agri impact.

- Essay & Ethics – Sustainability, bio-innovation, and climate justice.

Subsectoral Distribution (2024)

- BioIndustrial (47% | USD 78.2 bn)

- Biofuels, bioplastics, enzymes, green chemicals.

- Key driver of circular and green economy.

- BioPharma & BioMedical (35.2% | USD 58.4 bn)

- Affordable generics, vaccines, biologics, diagnostics, MedTech.

- Global reputation for cost-effective biopharma.

- BioAgri (8.1% | USD 13.5 bn)

- GM crops, Bt cotton success, precision farming, biofertilizers, biopesticides.

- BioResearch & BioIT (9.4% | USD 15.6 bn)

- Contract research, clinical trials, bioinformatics, biotech software.

- Strengthens India’s role as a global R&D hub.

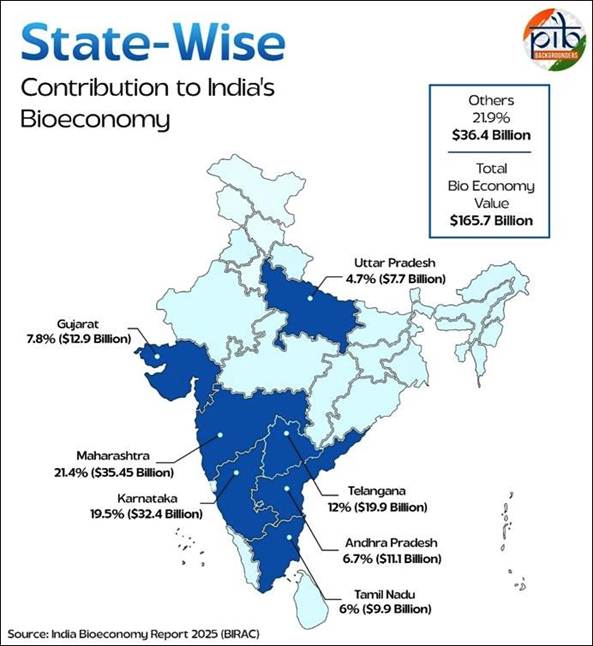

State & Regional Contribution (2024)

- Top States:

- Maharashtra (USD 35.45 bn | 21.4%), Karnataka (USD 32.4 bn | 19.5%), Telangana (USD 19.9 bn | 12%).

- Gujarat, Andhra Pradesh, Tamil Nadu, Uttar Pradesh follow.

- Regional Share:

- South (45.4%), West (30.3%), North (18.5%), East (5.8%).

- South dominates due to biotech clusters (Bengaluru, Hyderabad).

Major Policy Interventions

- BioE³ Policy (2024): Biotechnology for Economy, Environment, Employment.

- Biomanufacturing & Biofoundry Initiative: Move from consumptive → regenerative production.

- 21 BioEnabler facilities: Shared infra for startups & R&D (focus on microbial biotech, smart proteins, marine biotech, gene therapy).

- BioE³ Youth Challenge (2025): Monthly innovation contest, prizes (₹1L to ₹25L), incubation & mentoring for grassroots biotech talent.

Breakthrough Achievements

- Ethanol Blending:

- 20% blending (2025) → achieved 5 years ahead of target.

- Benefits: ₹1.21 lakh crore to farmers, elimination of sugarcane arrears, forex savings ₹1.44 lakh crore, crude substitution 245 LMT.

- Vaccine Leadership:

- Serum Institute: global share rose from 19% (2021) → 24% (2024).

- 3 Indian firms (Serum, Bharat Biotech, Biological E) among world’s top 10.

- Supplied 40% of WHO vaccines; 20% exports went to Africa.

- Precision Medicine & AMR:

- Launch of Nafithromycin (anti-AMR antibiotic).

- CAR-T therapies, AI-driven diagnostics, oncology gene sequencing.

Climate Change & Sustainability Role

- Bioeconomy enables:

- Emission reduction via biofuels, recycling, bioplastics.

- Carbon capture in agriculture, afforestation, food waste reduction.

- Greener manufacturing processes → reduced fossil dependence.

- Central to India’s net-zero roadmap by 2070.

Startup & Investment Ecosystem

- Startups: 13,000 in 2025 (from 5,365 in 2021; +142%).

- Products: 800+ launched; $600 mn follow-on funding.

- FDI: MedTech FDI grew from $370 mn (2022) → $618 mn (2024).

- Ecosystem backed by BIRAC, DBT, venture funding, incubation infra.

Global Positioning

- India is:

- Vaccine hub (low-cost, mass production).

- Ethanol leader (fastest adoption curve globally).

- Emerging precision medicine hub in the Global South.

- R&D outsourcing base for pharma & bioinformatics.

- By 2050, India may rival US, EU, and China as a bioeconomy power centre.

Challenges & Way Forward

- Challenges:

- Regulatory harmonisation across subsectors.

- Biosafety, bioethics, and AMR management.

- Funding volatility & global competition in biotech patents.

- Need to scale from pilot → industrial-level biomanufacturing.

- Way Forward:

- Strengthen IP regime, clinical trial capacity, and global partnerships.

- Incentivise R&D tax breaks, green financing, and rural biotech adoption.

- Enhance regional biotech clusters in East & North India.

- Foster public trust via awareness on biotech safety and benefits.

GST Reforms 2025: Relief for Common Man, Boost for Businesses

Historical Context

- Pre-GST Era (Before 2017)

- Fragmented indirect tax system (VAT, excise, service tax, octroi, entry tax).

- Multiple levies created cascading effect (“tax on tax”).

- Different state laws caused compliance burden & litigation.

- Weak input tax credit provisions → high cost of goods & services.

- GST Introduction (2017)

- Rolled out on 1st July 2017 via 101st Constitutional Amendment.

- Subsumed 17 taxes & 13 cesses into a single national tax.

- Created “One Nation, One Tax, One Market” framework.

- Brought IT-based filing, improved transparency, and widened the tax base.

Relevance :

- GS III (Economy) – Tax simplification, inflation relief, MSME competitiveness, boost to agriculture & manufacturing.

- GS II (Governance) – GST Council (Art. 279A), cooperative federalism, welfare-linked exemptions.

GST Performance till 2025

- Taxpayer base: Grew from 66.5 lakh (2017) → 1.51 crore (2025).

- Revenue Growth:

- FY 2017–18: ₹82,000 crore avg. monthly collection.

- FY 2024–25: ₹2.04 lakh crore avg. monthly collection.

- CAGR ~18%, gross collections doubled to ₹22.08 lakh crore in 4 years.

- Formalization: Stronger compliance + technology adoption increased revenues.

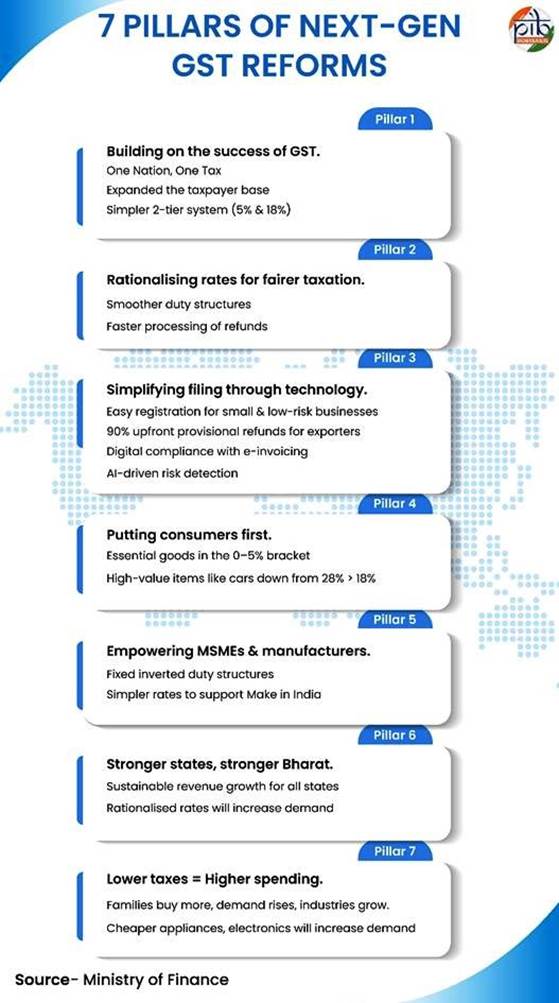

2025 GST Reform Highlights

- Simplification of Tax Structure

- Shift from 4 slabs (5%, 12%, 18%, 28%) → two slabs: 5% & 18%.

- 40% slab retained for luxury & sin goods (tobacco, aerated drinks, luxury cars, yachts, private aircraft).

- Focus: Relief to common man, lower input costs for MSMEs, boost to agriculture & manufacturing, and correction of inverted duty structures.

Sector-Wise Impact

A. Household & Food

- Daily essentials: soaps, toothpaste, shampoos, bicycles → down to 5%.

- Indian breads, paneer, UHT milk → NIL GST.

- Packaged foods (sauces, pasta, chocolates, coffee, preserved meat) → 18/12% → 5%.

- TVs (>32”), ACs, dishwashers → 28% → 18%.

Impact: Boost in affordability + demand for FMCG & consumer durables.

B. Housing & Construction

- Cement: 28% → 18%.

- Marble, granite, bricks, bamboo products → 12% → 5%.

Impact: Lower construction costs, cheaper housing, push to infra sector, job creation.

C. Automobiles

- Two-wheelers ≤350cc & small cars: 28% → 18%.

- Buses, trucks, three-wheelers, auto parts: 28% → 18%.

Impact: Relief for middle-class + push for auto manufacturing & exports.

D. Agriculture

- Tractors: 12% → 5%.

- Tires & tractor parts: 18% → 5%.

- Irrigation equipment, harvesters, sprinklers: 12% → 5%.

- Bio-pesticides, natural menthol: 12% → 5%.

Impact: Lower input costs, farmer relief, boost to sustainable farming.

E. Services

- Hotels (<₹7,500/day): 12% → 5%.

- Gyms, salons, yoga: 18% → 5%.

Impact: Boost to hospitality, wellness, and tourism sectors.

F. Textiles, Toys & Handicrafts

- Manmade fibre: 18% → 5%; yarn: 12% → 5%.

- Handicrafts, statues, paintings, toys: 12% → 5%.

Impact: Boost exports, support artisans, rural jobs, cultural preservation.

G. Education

- Exercise books, pencils, erasers, crayons, sharpeners → 0% GST.

- Geometry boxes, trays: 12% → 5%.

Impact: Reduced education costs, student-friendly.

H. Healthcare

- Life-saving drugs & diagnostic kits: 12% → 0%.

- Other medicines (Ayurveda, Unani, Homeopathy): 12% → 5%.

- Medical oxygen, surgical instruments: 12–18% → 5%.

- Spectacles: 28% → 5%.

Impact: Affordable healthcare, support for domestic pharma & MedTech.

I. Insurance

- Life & health insurance premiums → GST exempt.

Impact: Promotes financial security, supports Insurance for All by 2047.

Broader Economic Impact

- Consumers: Lower costs → higher disposable income → demand growth.

- MSMEs: Lower input costs, corrected inverted duty structure → competitiveness.

- Manufacturing: Boost to domestic value addition, exports.

- State Revenues: Simplified rates + wider base → higher compliance → stable revenues.

- Employment: Growth in construction, auto, textiles, handicrafts.

- Inflation: Expected moderation due to lower GST on essentials.

- Formalization: Simple two-slab system reduces disputes, encourages compliance.

Challenges Ahead

- Revenue Neutrality: Risk of revenue loss from sharp rate cuts; must be offset by better compliance.

- State Compensation: Concerns of revenue shortfall for some states (esp. after cess phase-out).

- Transition Issues: Businesses must quickly adapt to new slabs, possible IT challenges.

- Luxury/Sin Goods Taxation: High 40% rate may sustain black market activity.

Long-Term Significance

- Reinforces GST as citizen-centric & business-friendly.

- Aligns with India’s goal of Ease of Living + Ease of Doing Business.

- Supports Viksit Bharat @2047 vision by:

- Affordable healthcare & education.

- Strong MSME & manufacturing base.

- Sustainable agriculture.

- Formalized, transparent tax system.