Content

- 67 and Rising: India’s Financial Inclusion Gains Momentum

- National Handloom Day 2025

67 and Rising: India’s Financial Inclusion Gains Momentum

What is Financial Inclusion?

- Definition: Financial inclusion refers to providing affordable financial services—banking, credit, insurance, pensions, and investments—to all individuals and businesses, especially underserved groups.

- Why It Matters: Enables inclusive economic growth, reduces poverty, increases resilience to financial shocks, and supports entrepreneurship and productivity.

- Global Recognition:

- UN SDGs: Identified as a key enabler in 7 out of 17 goals (e.g., poverty reduction, gender equality, decent work).

- World Bank: Monitors progress via Global Findex Database.

Relevance : GS 2 ( Governance, Inclusive Growth, Government Schemes), GS 3(Indian Economy)

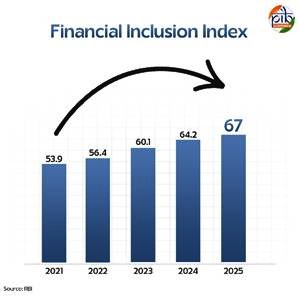

India’s Financial Inclusion Index (FI-Index) – Key Data (2025)

- FI-Index Value (2025): 67.0

- ↑ from 64.2 in 2024 and ↑ 24.3% since 2021 (baseline year).

- Index Scale: 0 (no inclusion) to 100 (complete inclusion).

- Index Components (97 indicators):

- Access (35% weight): Infrastructure availability – bank branches, ATMs, PoS, digital platforms.

- Usage (45% weight): Actual use of services – credit, savings, insurance, UPI.

- Quality (20% weight): Financial literacy, consumer protection, service equity.

PMJDY – The Foundation of Financial Inclusion

- Total Beneficiaries (Aug 2025): 55.98 crore

- Women Account Holders: >55% of total.

- Key Features:

- No minimum balance, ₹1 lakh accident cover, ₹10,000 overdraft, Rupay card.

- Outreach:

- 13.55 lakh Bank Mitras (banking correspondents).

- 107 Digital Banking Units (DBUs) functional (Dec 2024).

- Campaign Drive (July 2025):

- 6.65 lakh PMJDY accounts opened in 1 month.

- Over 10 lakh KYC updates.

- 99,753 outreach camps held.

Key Support Schemes – Multi-Sectoral Expansion

a. Social Insurance Schemes

| Scheme | Coverage | Premium | Benefit |

| PMSBY | 50.54 crore (2025) | ₹20/year | ₹2 lakh (accidental death) |

| PMJJBY | 23 crore | ₹436/year | ₹2 lakh (natural death) |

b. Pension Scheme

- Atal Pension Yojana (APY):

- Subscribers: 7.65 crore (April 2025)

- Corpus: ₹45,974.67 crore

- Women subscribers: ~48%

- Monthly pension: ₹1,000–₹5,000 (based on contributions)

c. Credit Enablement – MSMEs & Women

- Pradhan Mantri MUDRA Yojana (PMMY):

- Loans sanctioned: 53.85 crore

- Amount sanctioned: ₹35.13 lakh crore (as on Aug 2025)

- Target groups: Women, minorities, first-time entrepreneurs

- New Initiative: Tarun Plus – ₹10L–₹20L loans for repeat borrowers

- Stand-Up India Scheme:

- Total amount sanctioned: ₹61,020.41 crore (as on Mar 2025)

- Focus: SC/ST/women entrepreneurs in greenfield ventures

d. Digital Empowerment – UPI Revolution

- UPI Transactions (June 2025):

- Volume: 18.39 billion

- Value: ₹24.03 lakh crore

- Share in India’s digital transactions: 85%

- Global Contribution: ~50% of world’s real-time payments

e. Women Empowerment – Mahila Sammriddhi Yojana

- Target: Economically weak women

- Loan: Up to ₹1.4 lakh to SHGs

- Disbursement: ₹72,859 lakhs (till Mar 2025)

f. Agriculture Credit – Kisan Credit Card (KCC)

- Operative accounts: 7.72 crore farmers

- Outstanding loan: ₹10.05 lakh crore (Dec 2024)

- ↑ from ₹4.26 lakh crore (2014)

- Purpose: Working capital, marketing, household needs, farm maintenance

Policy Frameworks – Strategic Anchors

a. National Strategy for Financial Inclusion (NSFI 2019–24)

- Objectives:

- Universal financial access within 5 km radius

- Basic financial bouquet: savings, credit, insurance, pension

- Livelihood & skill linkages

- Financial literacy through AV modules

- Grievance redressal and consumer protection

b. National Strategy for Financial Education (NSFE 2020–25)

- 5C Approach:

- Content: Curriculum & training material

- Capacity: Build intermediaries’ capabilities

- Community: Leverage local networks

- Communication: Mass outreach

- Collaboration: Multi-stakeholder effort

Recent Campaign – 2025 Financial Saturation Drive

- Timeline: July–September 2025

- Objective: Reach every Gram Panchayat/ULB to:

- Open new PMJDY accounts

- Enrol in PMSBY, PMJJBY, APY

- Conduct re-KYC

- Raise awareness on digital fraud, grievance redressal

- Progress (July 2025):

- 6.65 lakh accounts opened

- >10 lakh KYC re-verifications

- ~1 lakh outreach camps held

Outcomes and Impact – India’s Financial Inclusion Landscape (2025)

- FI-Index reflects:

- ↑ access and use of banking and digital services

- ↑ quality via financial literacy and protection

- Inclusivity gains:

- Women, rural households, small entrepreneurs, unorganised sector

- Reduced informal credit dependency, esp. in agriculture and MSMEs

- Massive digital transformation through UPI and DBT architecture

Challenges Ahead

- Sustainability of Usage: Moving from mere account ownership to active usage

- Digital Divide: Regional, gender-based, and rural-urban disparities

- Financial Literacy: Low awareness of rights, fraud risks, grievance redressal

- Cybersecurity: Rising frauds as digital penetration increases

Conclusion

- India’s rising Financial Inclusion Index (67 in 2025) reflects a robust shift from access to active usage and quality, driven by digital innovation (like UPI), targeted schemes (PMJDY, APY, MUDRA), and grassroots campaigns for saturation and literacy.

- The transformation is structural and inclusive—bridging rural-urban, gender, and class divides—laying the foundation for equitable, resilient, and participatory economic growth.

National Handloom Day 2025

Background & Significance

- Historical Roots:

- Tied to the Swadeshi Movement launched on 7th August 1905, promoting indigenous industries like handloom as tools of economic resistance.

- Institutionalisation:

- 7th August declared National Handloom Day in 2015, first celebrated in Chennai.

- Objective:

- Celebrate handloom heritage.

- Recognise contributions of artisans.

- Promote ‘Vocal for Local’ and Atmanirbhar Bharat.

Relevance : GS 1( History , Heritage)

11th National Handloom Day 2025

A. Venue & Awards

- Date & Venue: 7th August 2025, Bharat Mandapam, New Delhi.

- Dignitary: President of India.

- Awards Distributed:

- Sant Kabir Awards (5):

- ₹3.5 lakh, gold coin, Tamrapatra, shawl, certificate.

- National Handloom Awards (19):

- ₹2 lakh, Tamrapatra, shawl, certificate.

- Sant Kabir Awards (5):

B. Theme-based Innovation:

Handloom Hackathon 2025

- Date: 4th August at IIT Delhi.

- Theme: “DREAM IT; DO IT”

- Stakeholders: Ministry of Textiles, NDC, FITT, IIT-D.

- Objective: Tech-enabled, design-led solutions for traditional problems.

C. Public Engagement Initiatives

1–8 August 2025: Week-long Celebration

- Know Your Weaves Campaign:

- Venue: National Crafts Museum, New Delhi.

- Activities:

- Live demos, storytelling, natural dye workshops.

- Weaves like Banarasi, Chanderi, Kanchipuram, Pochampally.

- Youth engagement through quizzes, installations.

- Saree Festival: Janpath Haat (116 weaves).

- Fashion Shows:

- Vastra Veda – regional handloom showcases.

- Naad – fusion of music and handloom narratives.

- India International Hand-woven Expo:

- Dates: 7–9 August at Bharat Mandapam.

- Buyers–Sellers meet for global promotion.

Sectoral Overview: Economic & Social Context

A. Employment & Livelihood

- Largest cottage industry in India.

- 4th Handloom Census (2019-20):

- 35.22 lakh households, >35 lakh artisans.

- Women comprise 72% of weavers – vital for rural women’s empowerment.

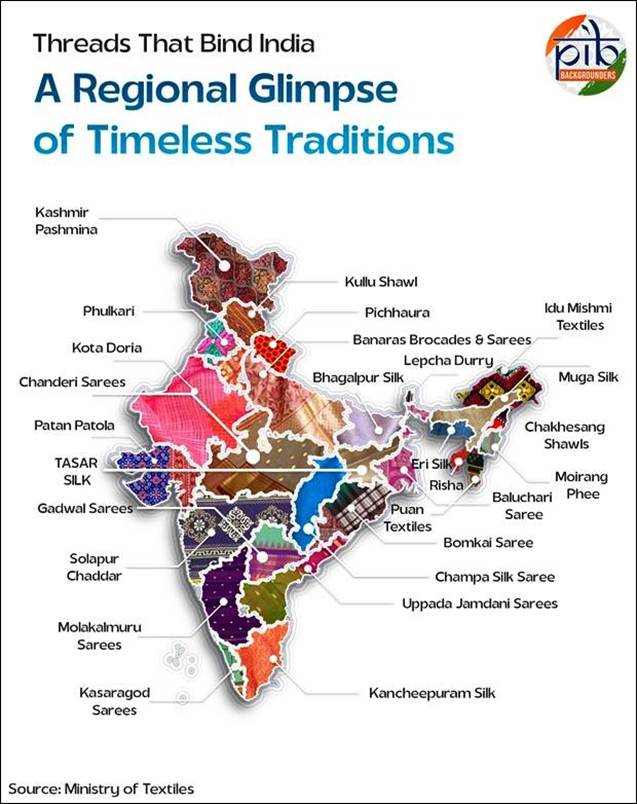

B. Cultural Relevance

- Carries stories of heritage, identity, and ecology.

- Made using eco-friendly, low-capital, and sustainable methods.

- Popular weaves: Banarasi, Kanjeevaram, Chanderi, Bomkai, Paithani, Jamdani, etc.

Global Recognition & Export Performance

A. India’s Global Handloom Standing

- 95% of the world’s handwoven fabric is from India.

- Unique due to living craft traditions + commercial viability.

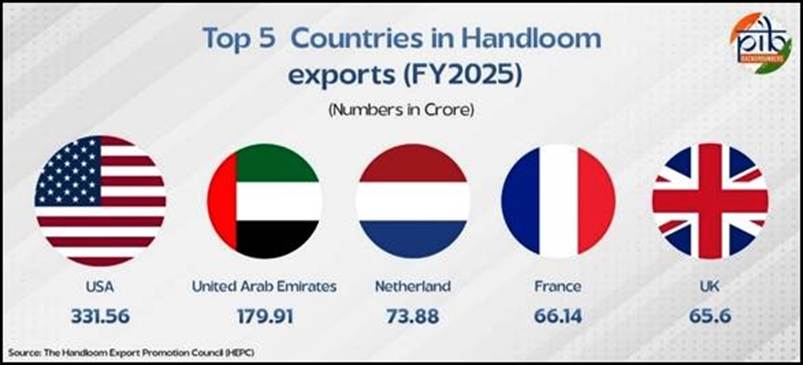

B. Exports (FY 2024-25):

| Country | Export Value (₹ crore) |

| USA | ₹ 331.56 |

| UAE | ₹ 179.91 |

| Netherlands | ₹ 73.88 |

| France | ₹ 66.14 |

| United Kingdom | ₹ 65.6 |

C. Product Categories (Share in Total Export):

- Made-ups (Curtains, linen): 42.4%

- Floor coverings: 40.6%

- Clothing accessories: 12.7%

- Fabrics: 4.3%

Government Schemes: Financial & Policy Support

A. Key Schemes

| Scheme | Objective |

| NHDP | Cluster development, marketing, skill building |

| Raw Material Supply Scheme (RMSS) | Yarn subsidy, freight reimbursement |

| MUDRA Loans | 6% interest rate, margin money, online portal |

| Handloom Mark & India Handloom Brand | Certification & branding of authentic products |

| Small Cluster Development Programme | Up to ₹2 crore/cluster for tools, looms etc. |

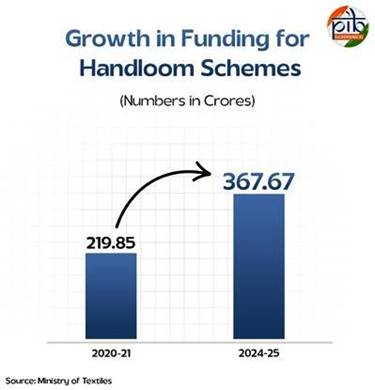

B. NHDP Performance

| Parameter | 2014–24 | 2024–25 (so far) |

| Clusters Sanctioned | 715 | 79 |

| Funds Released (₹ crore) | 533.17 | 85.99 |

| Beneficiaries Covered | 2.16 lakh | 12,221 |

| Marketing Events | 2316 | 177 |

| Products under GI Act | 73 | 31 |

C. Social Security Measures

- PMJJBY, PMSBY, MGBBY schemes.

- Awardee weavers (60+ years): ₹8,000/month support.

- Children of weavers: Scholarships up to ₹2 lakh/year.

Modernisation, Digitisation & Capacity Building

| Initiative | Description |

| Skill Upgradation | Eco-dyeing, design innovation, e-commerce skills |

| Hathkargha Samvardhan Yojana | Govt bears 90% cost of new looms |

| Workshed Scheme | ₹1.2 lakh units; 100% subsidy for marginalised |

| Producer Companies | 163+ companies formed to improve market access |

| indiahandmade.com & GeM | 1.8 lakh onboarded on GeM; 2418 sellers on IndiaHandmade |

GI Tagging: Preserving Design Identity

- 104 handloom products registered under GI Act (1999).

- Seminars, workshops conducted for awareness and registration.

Critical Appraisal

Strengths:

- Deep cultural roots + global market edge.

- Inclusive (women-dominated, rural employment).

- Eco-friendly production.

- Supported by strong institutional frameworks (NHDP, RMSS).

Challenges:

- Competition from powerlooms & cheap imports.

- Lack of awareness among youth & modern consumers.

- Low income levels despite high skill.

- Fragmented supply chains, weak marketing.

Way Forward

- Design-Led Innovation: Expand hackathons, design schools in clusters.

- Market Expansion: Strengthen exports via trade pacts, fashion weeks.

- Digital Push: Strengthen platforms like indiahandmade.com.

- Social Media Campaigns: Influence-driven marketing to attract youth.

- Integrated Value Chains: Cooperatives, logistics, branding under one roof.

- Financial Literacy & Credit Access: Strengthen Mudra, SHG linkages.

- Education: Include handloom heritage in school & design curriculums.

Conclusion

National Handloom Day 2025 exemplifies India’s renewed commitment to blending heritage with innovation, honouring the artisans, and building a self-reliant handloom ecosystem. It reflects a strategic vision of “economic empowerment through cultural pride.” As India celebrates its weaving traditions, the focus is shifting from preservation to transformation, from craft to commerce.