Content

- Crafted in India, Delivered Globally: Exports Powered by Trade Agreements

- The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India (SHANTI) Bill, 2025

Crafted in India, Delivered Globally: Exports Powered by Trade Agreements

Why is it in News?

- 18 December 2025: Government released official data highlighting robust export growth and the role of Free Trade Agreements (FTAs).

- Key trigger: Signing of India–Oman CEPA.

- Signals:

- Strong post-pandemic export momentum.

- Strategic shift from protectionism to rules-based trade integration.

- Exports positioned as a growth engine amid global slowdown and geopolitics.

Relevance

GS III – Economy

- Export-led growth; narrowing trade deficit.

- Role of FTAs in market access, GVC integration.

- Manufacturing & MSMEs: PLI, RoDTEP, GST 2.0, labour reforms.

- Export diversification → macroeconomic stability.

Understanding India’s Export Framework

- Exports: Goods + services sold abroad; critical for:

- GDP growth.

- Forex earnings.

- Employment (labour-intensive sectors).

- Trade Balance = Exports – Imports.

- FTAs / CEPAs / CETAs:

- Reduce tariffs.

- Liberalise services.

- Provide market access + mobility.

- Enable integration into Global Value Chains (GVCs).

Snapshot: India’s Export Performance (Nov 2024–Nov 2025)

- Total exports:

- ↑ from US$ 64.05 bn → US$ 73.99 bn (+15.52% YoY).

- Imports:

- Largely stable at US$ 80.63 bn.

- Trade deficit:

- ↓ from US$ 17.06 bn → US$ 6.64 bn (–61.07%).

- Structural takeaway:

- Growth without import surge → healthier external sector.

Composition of Export Growth

Merchandise vs Services

- Merchandise exports:

- US$ 38.13 bn (↑ 19.38% YoY).

- Share: 51.53%.

- Services exports:

- US$ 35.86 bn (↑ 11.67% YoY).

- Share: 48.47%.

- Inference:

- India nearing a balanced dual-export economy (goods + services).

Sector-wise Drivers of Growth

Labour-intensive & Traditional Strengths

- Readymade garments:

- US$ 1.25 bn, ↑ 11.27%.

- Employment-intensive → inclusive growth.

- Gems & jewellery:

- ↑ 27.8%.

- Demand from US, UAE, Europe.

Knowledge & Value-added Sectors

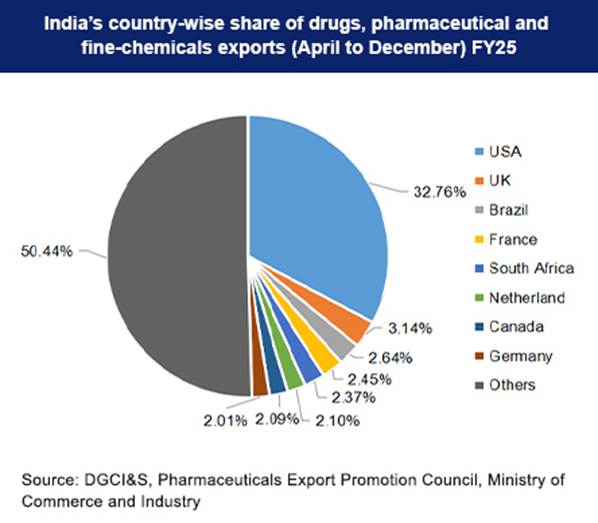

- Pharmaceuticals:

- ↑ 20.19%.

- “Pharmacy of the World”; exports to 200+ countries.

- Organic & inorganic chemicals:

- ↑ 18.49%.

- Engineering goods:

- Steady growth; US largest destination.

Strategic Manufacturing

- Petroleum products:

- ↑ 11.65%.

- India: 7th largest exporter of refined petroleum globally.

- Electronics (mobile phones):

- From ₹1,500 crore (2014–15) → ₹2 lakh crore (2024–25).

- 127× growth in a decade.

- Top markets: US, UAE, Netherlands, UK, Italy.

Market Diversification: Geography Matters

- High growth markets:

- UAE (14.5%), Japan (19%), Spain (9%), France (9.2%).

- Egypt (27%), Saudi Arabia (12.5%), Hong Kong (69%).

- Insight:

- Reduced overdependence on US–EU.

- South–South trade and West Asia emerging as stabilisers.

Export Diversification: Strategic Rationale (Analytical Core)

1. Reducing Volatility

- Commodity concentration → price shocks.

- Diversification spreads risk across sectors & markets.

2. Shock Absorption

- Protects against:

- Global recessions.

- Geopolitical disruptions.

- Supply-chain fragmentation.

3. Knowledge Spillovers

- New exports → new technologies, skills, logistics.

- Long-term productivity gains (endogenous growth logic).

4. Macroeconomic Stability

- Exports = 21.2% of GDP (2024).

- Diversification:

- Stabilises forex.

- Improves investment confidence.

- Supports sustainable growth.

Recently Concluded

- India–Oman CEPA

- Zero duty on 98.08% of Oman tariff lines.

- First-ever commitments on traditional medicine (AYUSH).

- Strong Mode-4 mobility provisions.

- India–UK CETA

- Duty-free access to 99% of Indian exports.

- Services + professional mobility.

- Double Contribution Convention → ₹4,000+ crore savings.

- India–EFTA TEPA

- USD 100 bn investment commitment.

- 1 million jobs target.

Earlier Strategic Pacts

- India–UAE CEPA

- India–Australia ECTA

- India–Mauritius CECPA

Ongoing Negotiations

- India–EU FTA

- India–US Trade Agreement (Mission 500).

- India–GCC FTA

- Israel, ASEAN (AITIGA review), Canada, Mexico, New Zealand.

Domestic Policy Support: Export Competitiveness Stack

1. Export Promotion Mission (2025)

- Outlay: ₹25,060 crore.

- Niryat Protsahan: Trade finance for MSMEs.

- Niryat Disha: Quality, branding, compliance.

2. Labour Codes

- 29 laws → 4 codes.

- Lower compliance cost + worker protection.

- Boosts export-oriented manufacturing.

3. Next Gen GST 2.0

- 90% provisional refunds.

- Refunds for low-value consignments.

- Corrected inverted duty structures.

- Competitive logistics & working capital relief.

4. Structural Enablers

- RoDTEP: ₹58,000 crore disbursed.

- PLI:

- ₹1.76 lakh crore investment.

- ₹16.5 lakh crore output.

- 12 lakh jobs.

- Logistics: PM GatiShakti, NLP.

- Institutional:

- Districts as Export Hubs (734 districts).

- SEZ exports: ₹14.56 lakh crore (FY 2024–25).

Critical Evaluation

- Strengths:

- Balanced goods–services growth.

- FTAs aligned with comparative advantage.

- Electronics & pharma as sunrise exports.

- Concerns:

- MSME compliance capacity.

- Preference erosion due to overlapping FTAs.

- Rules of origin complexity.

- Way Forward:

- Trade facilitation + skilling.

- Services-led FTAs with data adequacy.

- Export credit deepening.

Conclusion

- India’s export story reflects a structural transformation, not a cyclical rebound.

- Diversification across products, markets, and agreements has:

- Reduced vulnerability.

- Improved trade balance quality.

- Enhanced strategic autonomy.

- FTAs are no longer transactional tools but pillars of India’s growth, employment, and global economic positioning.

The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India (SHANTI) Bill, 2025

Why is it in News?

- 19 December 2025: Introduction of the SHANTI Bill, 2025.

- Context:

- India’s commitment to net-zero by 2070.

- Announcement of Nuclear Energy Mission in Union Budget 2025–26.

- Target of 100 GW nuclear capacity by 2047.

- Signals a structural reset of India’s nuclear legal framework, last comprehensively shaped in 1962 and 2010.

Relevance

GS III – Energy, Environment, S&T

- Energy security & clean energy transition.

- Nuclear power for net-zero 2070; 100 GW by 2047.

- SMRs, hydrogen, indigenous nuclear technology.

- Safety, waste management, disaster preparedness.

What is Nuclear Energy?

- Definition:

- Electricity generated using heat released from nuclear fission (splitting of atoms).

- Key features:

- Near-zero greenhouse gas emissions.

- High capacity factor (24×7 baseload).

- Complements intermittent renewables (solar, wind).

- Global role:

- Critical for deep decarbonisation in energy-intensive economies.

Evolution of India’s Nuclear Legal Framework

1. Atomic Energy Act, 1962

- Replaced the 1948 law.

- Centralised control over:

- Research.

- Development.

- Use of atomic energy for peaceful purposes.

- Reflected post-independence strategic caution.

2. Amendments (1986, 1987, 2015)

- Allowed:

- Government companies.

- Select joint ventures.

- Objective:

- Capacity expansion without diluting sovereign control.

3. Civil Liability for Nuclear Damage Act, 2010

- Introduced no-fault liability.

- Ensured victim compensation.

- However:

- Created investor uncertainty.

- Limited private and foreign participation.

Rationale Behind SHANTI Bill, 2025

- India’s nuclear ecosystem has matured:

- Indigenous reactor design.

- Global cooperation.

- Advanced safety practices.

- Existing laws:

- Fragmented.

- Rigid.

- Unsuitable for rapid scale-up and innovation.

- Need for:

- Unified legislation.

- Regulatory independence.

- Clean energy alignment.

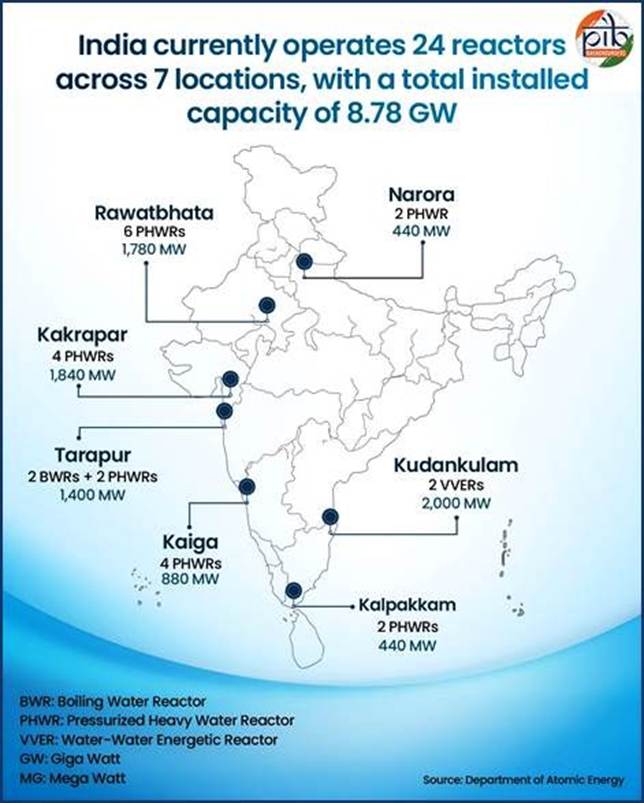

Present Status of Nuclear Power in India

- Share in electricity generation (2024–25): ~3.1%.

- Installed capacity: 8.78 GW.

- Pipeline:

- Indigenous 700 MW and 1000 MW reactors.

- Projected capacity: 22.38 GW by 2031–32.

- Inference:

- Underutilised potential despite technological capability.

Nuclear Energy Mission (Budget 2025–26)

- Allocation: ₹20,000 crore.

- Focus: Small Modular Reactors (SMRs).

- Targets:

- ≥5 indigenously designed SMRs by 2033.

- Key initiatives byBhabha Atomic Research Centre:

- BSMR-200 (200 MWe).

- SMR-55 (55 MWe).

- HTGR (≤5 MWth) for hydrogen generation.

- Strategic aim:

- Technology leadership.

- Energy security.

- Non-power nuclear applications.

Why India Must Scale Nuclear Power ?

- Rapidly rising electricity demand:

- Data centres.

- AI and advanced manufacturing.

- Limitations of renewables:

- Intermittency.

- Storage costs.

- Nuclear advantages:

- Baseload power.

- Long plant life.

- Low land footprint.

- Legal bottleneck:

- 1962 & 2010 laws unsuitable for 100 GW by 2047 ambition.

Core Architecture of the SHANTI Bill, 2025

1. Private Sector Participation

- Permitted in:

- Plant operations.

- Power generation.

- Equipment manufacturing.

- Limited fuel fabrication (within notified thresholds).

- Mandatory prior safety authorisation for all radiation-related activities.

2. Activities Reserved for Central Government

- Enrichment and isotopic separation (unless notified).

- Spent fuel reprocessing and recycling.

- High-level radioactive waste management.

- Heavy water production.

- Ensures strategic control.

3. Licensing & Safety Oversight

- Structured process for:

- Granting.

- Suspension.

- Cancellation of licences.

- Safety authorisation becomes the legal cornerstone.

4. Graded Liability Framework

- Replaces uniform liability cap.

- Operator liability varies by:

- Type of installation.

- Risk profile.

- Detailed in Second Schedule.

- Addresses investor concerns while protecting victims.

5. Regulation of Non-Power Applications

- Covers nuclear use in:

- Healthcare.

- Agriculture.

- Industry.

- Research.

- Enables medical isotopes, food irradiation, industrial radiography.

6. Exemptions for Innovation

- Limited exemptions for:

- R&D.

- Experimental work.

- Encourages innovation without diluting safety.

Institutional & Regulatory Reforms

- Statutory status toAtomic Energy Regulatory Board:

- Enhances independence.

- Strengthens credibility.

- Dispute resolution:

- Atomic Energy Redressal Advisory Council.

- Appellate authority:

- Appellate Tribunal for Electricity.

- Claims framework:

- Claims Commissioners.

- Nuclear Damage Claims Commission for severe incidents.

Safeguards & Strategic Oversight

- Sovereign control retained over:

- Fuel cycle.

- Waste.

- Security.

- Enhanced:

- Emergency preparedness.

- Quality assurance.

- Safeguards and inspections.

- Ensures:

- National security.

- Strategic autonomy.

- International confidence.

Critical Evaluation

Strengths

- Aligns nuclear law with climate goals.

- Unlocks private capital and innovation.

- Strengthens independent regulation.

- Supports SMRs and hydrogen economy.

Concerns

- Capacity of AERB to regulate expanded ecosystem.

- Public perception and safety confidence.

- Long-term waste management challenges.

Way Forward

- Transparent communication.

- Global best practices in liability and safety.

- Human resource and regulatory capacity building.

Conclusion

- The SHANTI Bill, 2025 represents a generational shift in India’s nuclear governance.

- It balances:

- Expansion with caution.

- Innovation with sovereignty.

- Clean energy goals with strategic control.

- If effectively implemented, it can anchor nuclear energy as a reliable pillar of India’s clean, secure, and self-reliant energy future.