Content

- Smart Finance, Smart Future: GIFT City

- 8.2% GDP: India’s Growth Story Strengthens

Smart Finance, Smart Future: GIFT City

What is GIFT City?

- India’s first International Financial Services Centre (IFSC) under SEZ Act, 2005.

- Located in Gandhinagar, spread over ~1000 acres, expanding to 3300+ acres (DTA + GIFT SEZ).

- India’s first operational smart city + integrated financial hub.

- Hosts 1034+ registered entities, 38 banks, asset base $100.14 bn.

- Offers 10-year income tax holiday in a 15-year block.

- Competes with Singapore, Dubai, Hong Kong.

Relevance:

GS 3 – Economy

- International Financial Services Centre (IFSC): role in financial sector reforms.

- Capital markets, global financial integration, offshore vs onshore financial hubs.

- Regulatory architecture (IFSCA Act 2019) → institutional reforms.

- SEZ Act, tax incentives, competitiveness in global finance.

GS 3 – Infrastructure

- Smart city infrastructure: district cooling, utility tunnels, zero-discharge water, 99.999% power reliability.

- High-speed connectivity, metro linkages, airport access.

- Tier-IV data centre & digital backbone as critical infrastructure

Origins and Vision

- Conceived to bring offshore financial services onshore.

- Aims to position India as a top global financial centre by 2047.

- Strategy pillars:

- Attract global capital

- Enable regulatory innovation

- Build fintech-led financial infrastructure

- Generate high-skilled jobs

- Government-backed integrated planning ensures walk-to-work, sustainability, ease of doing business.

Governance and Regulatory Architecture

International Financial Services Centres Authority (IFSCA)

- Statutory regulator under IFSCA Act, 2019.

- Unifies powers of RBI, SEBI, IRDAI, PFRDA for IFSC.

- Regulates products, institutions, conduct, supervision.

- IFSC units treated as non-residents under FEMA → enhances international competitiveness.

Single Window Governance

- Powers delegated from SEZ Development Commissioner to IFSCA.

- SWITS (Single Window IT System) enables integrated approvals.

Key Institutions

India International Bullion Exchange (IIBX)

- Launched 2022; world-class bullion trading ecosystem.

- Complies with OECD due diligence standards.

- Enables transparent gold imports and bullion-linked financial products.

Financial Ecosystem Snapshot (2025)

- Fund Managers (FMEs): 194

- IFSC Exchanges: 2, monthly turnover $89.6 bn

- GIFT NIFTY monthly turnover: $102.35 bn

- Insurance + intermediaries: 52

- Aircraft lessors: 37 (303 aircraft leased)

- Ship lessors: 34 (28 ships leased)

- Banking assets: $100.14 bn

- Cumulative transactions: $142.98 bn

GIFT City as a Global GCC/GIC Hub

- Financial groups set up Global In-House Centres (GIC/GCC) under IFSCA GIC Regulations, 2020.

- Operate in foreign currency; serve global markets.

- Major players:

- Infineon (750 staff), Technip Energies (500), TELUS (500)

- Accenture, Capgemini, IBM, NASSCOM CoE

FinTech Growth Engine

Regulatory Framework

- FinTech regulations notified April 2022.

- Dual entry route: Direct Authorization + Sandbox.

- 20 FinTech/TechFin entities, 8 sandbox participants.

- Big players: Wipro, Infosys, Cognizant, Hexaware, KFintech, Signzy.

Fintech Innovation & Research Centre

- Joint initiative: Govt of Gujarat + Asian Development Bank.

- Partners: IITGN, Ahmedabad University, UC San Diego, Plug and Play.

- Focus: R&D, incubation, global collaboration.

Business Setup Framework

- Entities must be from FATF-compliant jurisdictions.

- Allowed structures: Company, LLP, Branch.

- Must be linked to financial products/services.

- IFSC units = non-resident status → regulatory clarity.

Infrastructure Excellence: GIFT as a Smart City

Utility Innovations

- District Cooling System: 30% energy saving.

- Automated Waste Collection System: Pneumatic, zero manual transport.

- 17-km Utility Tunnel: Digging-free city.

- Zero-Discharge Water: 24×7 potable supply; sewage reuse.

- Power Reliability: 99.999% uptime (≈5.3 min outage/year).

- Tier IV Green Data Centre: 99.999% uptime + global certifications.

Transport Connectivity

- Metro to Ahmedabad–Gandhinagar.

- 20 min from Ahmedabad airport.

- 15 min from high-speed rail terminal (proposed).

- EV bus network; NH-48 Delhi–Mumbai corridor.

Social Infrastructure

- 21-acre Central Park, riverfront, Lilavati Hospital.

- City Command Centre (C4): SCADA-based utility monitoring; 70,000+ I/O sensors.

Talent and Education Hub

- Access to top-tier institutions: IIM-A, IIT-Gn, GMU.

- Local professional pool:

- 86,000 software engineers

- 71,000 finance professionals

- 21,000 management professionals

- 142% growth in AI-skilled talent (Ahmedabad).

Global Universities

- Operational: Deakin University, University of Wollongong.

- Upcoming: Queen’s University Belfast, Coventry University.

- AISPs enable foreign campuses via infrastructure support.

Business Highlights (2025)

- 1034+ entities across finance, insurance, capital markets, fintech, leasing.

- Jumped to 46th in Global Financial Centres Index (2025).

- Ranked 5th among emerging centres; topped reputation index.

- Dollar loan market: $20 bn disbursed; overtook Singapore, London for India-linked dollar loans.

Fiscal & Non-Fiscal Incentives

Direct Tax

- 10-year tax holiday within 15-year block (Sec 80-LA).

- Reduced TDS on interest income.

Indirect Tax

- No GST on IFSC transactions.

- Custom duty exemption for SEZ imports.

Other Incentives

- No STT, CTT, stamp duty.

- Exemptions under Companies Act.

- 100% PF reimbursement.

- Gujarat IT/ITeS incentives: CAPEX/OPEX support, electricity duty waiver.

Why GIFT City is Rising Globally ?

- Unified regulator + predictable policy regime.

- Offshore-like environment within Indian jurisdiction.

- High-end infrastructure + global-grade digital backbone.

- Increasing shift of treasury operations, aircraft leasing, ship leasing, fintech innovation to GIFT.

- Strategic location in one of India’s fastest-growing economic corridors.

Challenges & Concerns

- Needs deeper liquidity, global investor diversity.

- Global competition from Singapore, Dubai, Shanghai.

- Talent density still lower than global hubs.

- Fiscal incentives must align with WTO rules.

- Regulatory adaptation needed for emerging products (crypto-assets, carbon markets, green finance).

Why It Matters ?

- Instrument for financial sector reforms, capital account liberalisation.

- Aligns with Viksit Bharat 2047, Make in India, Aatmanirbhar Bharat.

- Anchor for India’s fintech and digital public infrastructure exports.

- Critical for globalising Indian rupee, boosting India-linked dollar loan markets.

- Enhances India’s position in global financial diplomacy.

Conclusion

- GIFT City has evolved into India’s most ambitious financial ecosystem—combining global-grade regulation, infrastructure, talent, and incentives.

- Its fast-growing fintech, aircraft leasing, bullion trading, and capital market segments position it as a future rival to global hubs.

- With sustainability and innovation at its core, GIFT City is central to India’s aspiration to become a top global financial centre by 2047.

8.2% GDP: India’s Growth Story Strengthens

Why Is This in News?

- PIB released Q2 FY26 macroeconomic data showing 8.2% real GDP growth, reaffirming India as the fastest-growing major economy.

- Headline CPI dropped to 0.25% (record low in current series), raising debate on disinflation, deflation risks, and policy stance.

- IIP, exports, labour participation, and GST collections showed broad-based improvement, signalling strong domestic momentum despite global slowdown.

Relevance:

GS 3 – Economy

- Macro indicators: GDP, GVA, CPI, WPI, IIP → core macroeconomic fundamentals.

- Sector-wise performance: primary vs secondary vs tertiary.

- Disinflation, deflation risk, monetary policy trade-offs (RBI 2–6% band).

- Labour market dynamics: LFPR, WPR, unemployment, EPFO data.

- Export performance: services dominance, electronics exports → value-chain upgrading.

- PLI scheme impact on manufacturing revival.

- Fiscal indicators: GST revenues, structural reforms.

- Global agencies’ growth projections → investor confidence.

What Is GDP and Why It Matters

- GDP = market value of all final goods and services produced within a country.

- Real GDP adjusts for inflation → reflects true output growth.

- GVA = GDP + taxes – subsidies; shows sectoral strength.

- GDP growth indicates economic momentum, investment cycles, employment generation.

Headline Findings (Q2 FY26 + Apr–Sep H1)

GDP

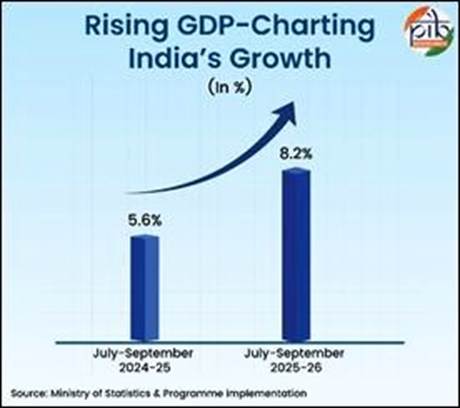

- Real GDP: 8.2% in Q2 vs 5.6% last year.

- Real GDP H1 FY26: 8% vs 6.1% in FY25.

- Nominal GDP Q2: 8.7%.

Sectoral GVA

- Primary: 3.1% (weather-linked, structural stagnation).

- Secondary: 8.1% (manufacturing-heavy recovery).

- Tertiary: 9.2% (services remain the growth engine).

Inflation Trajectory (CPI + WPI)

CPI (Retail Inflation)

- October 2025 CPI: 0.25%, lowest in current CPI series.

- Food inflation (CFPI): –5.02% → major driver of disinflation.

- Rural CPI: –0.25%; Urban CPI: 0.88%.

WPI (Wholesale Inflation)

- October 2025 WPI: –1.21%.

- WPI food inflation: –5.04%.

- Driven by lower crude, metals, food prices.

Policy Interpretation

- Inflation well within RBI’s 2–6% band.

- Supports neutral–accommodative monetary stance.

- Raises medium-term questions: disinflation vs demand softening.

Industry & Manufacturing: IIP Signals

IIP (September 2025)

- Overall IIP: 4% YoY.

- Manufacturing: 4.8% → main driver.

Top Sub-sectors

- Basic metals: 12.3%.

- Electrical equipment: 28.7%.

- Motor vehicles: 14.6%.

Use-Based Classification

- Infrastructure/Construction Goods: 10.5%.

- Consumer Durables: 10.2%.

- Intermediate Goods: 5.3%.

Interpretation

- Strong investment cycle revival.

- Healthy demand for consumer durables.

- Manufacturing expansion aligns with PLI impact.

Employment Trends: Labour Market Strength

Macro Labour Indicators

- LFPR: 55.4%, highest in 6 months.

- WPR: 52.5%.

- Unemployment: 5.2% (stable).

- Female LFPR: 34.2% (improving but structurally low).

EPFO Data

- Net additions: 21.04 lakh in July 2025.

White-Collar Hiring (Naukri JobSpeak)

- Hiring up 10.1%.

- AI-ML jobs: +61%.

- Fresher hiring: +15%.

Interpretation

- Labour market broadening across sectors.

- Services + technology driving job growth.

- Need for continued skilling to align workforce.

Trade & External Sector

Exports (Apr–Oct 2025)

- Combined exports: +4.84% (USD 491.8 bn).

- Merchandise exports: +0.63%.

- Services exports: +9.75% (USD 237.5 bn) → India’s stronghold.

Top Merchandise Growth Areas

- Electronics: +37.8%.

- Cashew: +28.32%.

- Other cereals: +25.52%.

- Marine products: +16.18%.

Export Market Growth

- Spain: +40.7%.

- China: +24.8%.

- Hong Kong: +20.7%.

- USA: +10.1%.

Interpretation

- India moving up value chains.

- Services cushion global goods-market slowdown.

- PLI boosting electronics export capability.

Government Policy Push: Structural Drivers

Manufacturing

- PLI: ₹1.97 lakh crore; investment attracted: ₹1.76 lakh crore.

- Skill India, Make in India → ecosystem building.

Labour Market

- PMKVY → 27 lakh trained.

- NAVYA → skilling adolescent girls.

- PMMY: ₹4.91 lakh crore sanctioned.

- 17th Rozgar Mela → 51,000 appointment letters.

Trade

- Export realization window extended → 15 months.

- Credit Guarantee Scheme → ₹20,000 crore credit facility to exporters.

- Export Promotion Mission → outlay of ₹25,060 crore.

GST 2.0

- Two-slab structure: 5% & 18%.

- GST collection (Oct 2025): ₹1.96 lakh crore (+4.6%).

Growth Projections (Global Agencies)

| Agency | Projection |

| RBI | 6.8% FY26 |

| World Bank | 6.5% (2026) |

| Moody’s | 6.4% (2026), 6.5% (2027) |

| IMF | 6.6% (2025), 6.2% (2026) |

| OECD | 6.7% (2025), 6.2% (2026) |

| S&P | 6.5% (FY26), 6.7% (FY27) |

High convergence across agencies → confidence in India’s fundamentals.

Big-Picture Takeaways

Strengths

- Broad-based GDP growth.

- Manufacturing revival → PLI impact visible.

- Services remain globally competitive.

- Inflation sharply moderated.

- Export ecosystems improving.

- Labour participation improving.

Emerging Concerns

- Excessively low CPI could indicate:

- demand softening in rural economy,

- agricultural stress.

- Primary sector growth modest (2.9%).

- Women’s LFPR still low compared to peers.

- WPI deflation may pressure MSME margins.

Strategic Implications

- India entering investment-led growth cycle.

- Strong macro stability enables fiscal room before 2029.

- Disinflation offers policy bandwidth for growth-supporting reforms.

- Need to improve:

- rural incomes,

- agricultural productivity,

- skilling for AI-driven jobs,

- export diversification.