Why in News ?

- India’s electricity demand, stagnant at around 5% annual growth for two decades, is now rising rapidly due to new high-energy sectors.

- Key demand drivers: AI & Data Centres, Electric Vehicles (EVs), 5G/IoT, green hydrogen, and digital economy expansion.

- The US, China, and Big Tech firms are already witnessing 25%+ annual power demand surges from AI data centres.

- India is planning GW-scale AI data centres (Google at Visakhapatnam, Reliance at Jamnagar) and exploring Small Modular Reactors (SMRs) as clean, reliable energy sources for them.

- The Union Budget 2025 launched a ₹20,000 crore Nuclear Energy Mission to add 100 GW nuclear capacity by 2047, including SMRs.

Relevance:

- GS 3 – Energy, Infrastructure, and Technology: AI-driven electricity demand, sustainable energy mix, nuclear innovation through Small Modular Reactors (SMRs), and linkage with the IndiaAI Mission.

- GS 2 – Governance and Policy: Inter-ministerial coordination between MeitY, MoP, and DAE for energy–technology convergence; clean energy policies under Budget 2025; regulatory reforms for private participation in nuclear energy.

- GS 3 – Environment: Low-carbon power strategy, Net Zero 2070 alignment, and sustainable infrastructure for digital economy expansion.

Background: India’s Power Demand Trends

- Past 20 years: Electricity demand grew at ~5% annually — relatively stable due to efficient grids, low industrial expansion, and moderated population growth.

- Shift (post-2023): Rise in data traffic, EV charging, AI computation, and green hydrogen manufacturing expected to double electricity demand by 2030.

- India’s per capita electricity consumption (2025): ~1,350 kWh — 1/3rd of global average (~4,000 kWh), but projected to rise steeply.

- Planning challenge: Aligning digital economy growth with sustainable, low-carbon electricity expansion.

Why India Needs Data Centres

- Digital India Mission, data localisation laws, and explosive data usage demand domestic storage and processing capacity.

- Current capacity: 1.4 GW

- vs. Europe: 10 GW

- India has 2× more internet users than Europe, yet 1/7th capacity.

- Expected growth:

- By 2027: 2–3× increase (to ~4 GW).

- By 2030: >5× increase (to ~7–8 GW) with AI and LLM infrastructure.

- Drivers:

- Data privacy & localisation mandates.

- 5G and IoT ecosystem.

- Cloud computing, fintech, and generative AI expansion.

Power Demand from AI Data Centres

- Traditional server racks: 15–20 kW.

- AI/LLM GPU racks: 80–150 kW (≈6× higher load).

- Global data centre electricity usage:

- 2024: ~460 TWh

- 2030 (projection): ~1,000 TWh

- 2035: ~1,300 TWh (~6% of global generation).

- Case studies:

- China:

- Data centre electricity use to reach 400+ billion kWh by 2025 (~4% of total power).

- CAGR ~18% (2023–2030).

- US (Dominion, Virginia):

- Electricity and peak demand projected to rise >25% in 5 years due to data centres.

- China:

Data Centre Hubs: Global and Indian

Global

- US: 51% of global capacity — hubs in Texas, Virginia, Ohio, Phoenix, Wisconsin, Pennsylvania.

- Other nations: China, Norway, UK, Germany, Japan, Malaysia investing in AI-grade infrastructure.

India

- Emerging AI data centre clusters:

- Visakhapatnam (Google) – GW-scale, AI-optimised.

- Jamnagar (Reliance Industries) – part of IndiaAI Mission.

- Mumbai, Chennai, Bengaluru, Hyderabad – existing hyperscale hubs (Yotta, AdaniConneX, Sify, CtrlS).

- IndiaAI Mission (2024):

- Focus on indigenous AI models, large-scale compute infrastructure, and clean energy linkages.

Powering the AI Era: Energy Mix Options

Renewables

- Solar, wind, and hydro as clean options but intermittent and storage-dependent.

- Storage (battery, pumped hydro) still developing — costly for 24/7 AI operations.

Natural Gas & Green Hydrogen

- Used as backup for renewables ensuring grid reliability.

- Hydrogen blending and onsite generation emerging in industrial clusters.

Emerging Alternatives

- Geothermal energy (pilot projects in Ladakh & Gujarat).

- Nuclear fusion research under ITER collaboration (long-term).

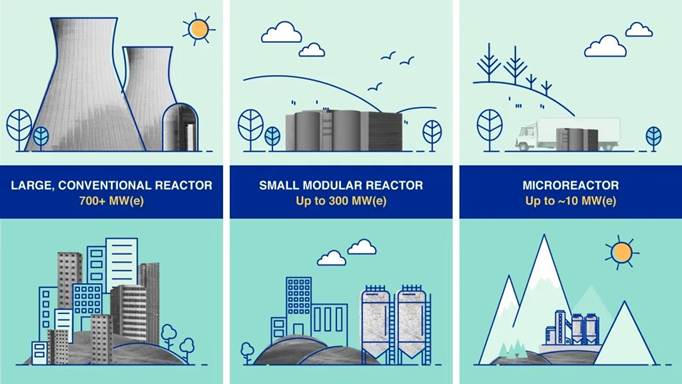

Small Modular Reactors (SMRs) – The Key Innovation

- SMRs emerging as reliable, low-carbon baseload solution for AI data centres.

- Range: 1–300+ MW capacity.

- Advantages:

- Modular, factory-built → faster deployment.

- Passive safety systems → no human/manual intervention needed.

- Can be located near consumption hubs → no transmission losses.

- Flexible for remote/industrial sites.

Global Investment & Regulation in SMRs

Investment Landscape

- Total global SMR investment: $15.4 billion

- $10 billion – public funding

- $5.4 billion – private capital (tech & energy companies)

- Big Tech (Google, Microsoft, Amazon) exploring SMR power purchase deals for AI facilities.

Regulatory Reforms (Global Trends)

Six key areas of SMR regulation evolving internationally:

- Technology-neutral frameworks (beyond large LWR models).

- Streamlined licensing – combined construction-operating licences.

- Fleet-wide approvals – enabling standardised mass deployment.

- Factory certification – for modular manufacturing.

- Risk-informed requirements – proportional safety zones.

- International harmonisation – via IAEA standards & mutual recognition.

Leading Regulatory Models

- U.S. ADVANCE Act (2024) – accelerates SMR licensing.

- Canada – Vendor Design Review (pre-licensing pathway).

- UK – Regulatory sandbox approach.

- IAEA – Nuclear Harmonization and Standardization Initiative (NHSI).

India’s SMR Push

Budget 2025 Initiatives

- ₹20,000 crore outlay under Nuclear Energy Mission.

- Target: 100 GW nuclear capacity by 2047.

- IndiaAI–Nuclear synergy: Aligns AI infrastructure growth with clean baseload energy.

Key Developments

- BARC’s BSMR-200 – 200 MW Pressurised Heavy Water Reactor (PHWR) variant.

- 55 MW SMR for remote areas in isolated grid mode.

- Holtec–India partnership for technology transfer.

- Private participation reforms:

- Planned amendments to Atomic Energy Act (1962) & Civil Liability Act (2010).

- Aims to attract $26 billion private investment.

State-level Role

- Pre-approval of coal plant sites for SMR conversion.

- Land facilitation, safety training, and workforce reskilling.

- Demonstration projects integrated with green hydrogen hubs.

SMR Safety and Environmental Aspects

- Passive safety features:

- Natural convection cooling.

- Automated shutdown systems.

- Accident-tolerant fuels withstand higher temperatures.

- Waste & transport regulation:

- Need for new frameworks addressing factory fabrication, transport risks, and spent fuel disposal.

- HALEU fuel (high-assay low-enriched uranium) requires specific waste management protocols.

- IAEA support:

- SMR Regulators’ Forum.

- Safeguards by Design Programme – balancing safety, economics, and security.

Opportunities for India

- Energy Security – 24/7 baseload for AI infrastructure.

- Climate Goals – Low-carbon transition aligned with India’s Net Zero 2070 target.

- Export Potential – India can become SMR exporter to Global South via cost-effective indigenous tech.

- Industrial Repurposing – Utilize decommissioned coal plant sites.

- Employment & Skill Creation – Reskill coal workforce for nuclear operations.

Challenges Ahead

- Regulatory delays – outdated laws not suited for SMRs.

- Public perception & safety concerns.

- Financing barriers – high upfront capital cost despite modularity.

- Waste disposal & liability – still unresolved.

- Grid integration – ensuring SMR–renewable hybrid stability.

Core Takeaway

India’s next energy transition will be driven not just by renewables, but by AI-driven demand.

Data centres and SMRs together define the digital–nuclear nexus of the future — where clean, constant power meets the data economy, enabling India’s journey from Digital India to Energy-Secure India by 2047.