Contents

- USTR Slams Digital services taxes adopted by India

- Payments Infrastructure Development Fund (PIDF) scheme

- GDP likely to Contract by 7.7% in 2020-21 according to FAE

- Sudden Stratospheric Warming (SSW)

USTR SLAMS DIGITAL SERVICES TAXES ADOPTED BY INDIA

Context:

The U.S. Trade Representative’s office (USTR) said that the Digital services taxes adopted by India, Italy and Turkey discriminate against U.S. companies and are inconsistent with international tax principles.

Relevance:

GS-III: Indian Economy

Dimensions of the Article:

- What is Digital Services Tax (DST)?

- How does India tax Digital Businesses?

- What are the Issues with India’s DST that is taken by the USTR?

- Significance of the discussion on imposing DST

- Advantages of Imposing Digital Tax

- Disadvantages of imposing Digital Tax

- Issues with the Existing Taxation systems for taxing Digital Services

- How are other countries handling it?

What is Digital Services Tax (DST)?

- Digital Services Tax (DST) is a tax levied on revenues that certain companies generate from providing certain digital services.

- The digital businesses include both the digital-only brands that focus on virtual commodities and services and the services traditional market players use for transforming their businesses with digital technologies.

- Virtual commodities include downloaded software, website applications and digital assets like eBooks, image files, audio clips/audio files, movies or digital files.

- Digital services include those provided by social media companies, collaborative platforms etc.

How does India tax Digital Businesses?

- India has been making use of an ‘equalisation levy’ to level the playing field for the domestic and the foreign players on the virtual platform.

- While the domestic businesses are subject to the Income Tax Act, their foreign counterparts are exempted from its provisions. Hence they enjoy an advantage over the domestic firms. This is what the levy seeks to equalize.

- Equalisation levy was first introduced in 2016 at the rate of 6%. However, this was only limited to advertisements online.

- It is noted that this is a transaction-based tax, as opposed to a tax on earnings. This is to ensure that India doesn’t violate its international obligations.

- It was introduced based on the recommendations of the Committee on Taxation of E-Commerce.

- In 2018, the Finance Act introduced the Significant Economic Presence concept to IT Act of 1961. It incorporates a digital nexus to tax the profits of foreign businesses, based on its revenues and local user-base. This is yet to come into force.

- Currently, India too is involved in the talks to bring in a revamped framework for taxing digital businesses as the international taxation principles being used in the present are outdated (formulated in the 1920s).

What are the Issues with India’s DST that is taken by the USTR?

- The US is probing the 2% Digital Services Tax (DST) that India adopted in 2020.

- The tax applies only to non-resident companies with annual revenues over $267,000, and covers online sales of goods & services to persons in India.

- Further, equalisation levy at 6% has been in force since 2016 on payment exceeding Rs. 1 lakh a year to a non-resident service provider for online advertisements.

- This is applicable for e-commerce companies that are sourcing revenue from Indian customers without having significant presence in the particular country.

- It is argued that India’s equalisation levy is complex and ambiguous which includes the possibility of double taxation.

- Further, India continues to be on the ‘Priority Watch List’ of USTR for lack of adequate Intellectual Property (IP) rights protection and enforcement.

- In India’s case, the probe could potentially affect the outcome of a bilateral trade deal that India has been looking to forge with the US.

Significance of the discussion on imposing DST

- The e-commerce market is set to expand to $200 billion by 2026. This is a largely untapped revenue source for not only the Indian government but also many of the world’s economies.

- India is a major market for the tech-giants like Facebook and Google and a significant portion of their profits flows from India – so it is only justified that they are taxed appropriately.

Post-Pandemic Significance of Imposition of DST

- As the world stares at a looming recession due to the pandemic and the lockdowns imposed, “Big Tech” businesses which involve digital presence rather than physical presence are thriving globally.

- E-commerce, subscriptions, and distributed business infrastructure have emerged as major revenue drivers.

- This has led more countries to consider and charter a domestic path towards digital taxation (Digital Service Taxes DSTs), as a source to augment the languishing fiscal revenues.

Advantages of Imposing Digital Tax

- Tech giants like Google, Facebook, Amazon etc., which have a huge consumer base in developing countries like India will not be able to avoid taxation by shifting their offices to low-tax regimes.

- If the law prevents profit shifts, the countries from which the cross-border digital companies’ profit will be able to stop losing corporate tax revenue.

- Digital tax will ensure a level playing field for both domestic and foreign players. In the absence of such a law, the goods and services provided by firms based in a foreign country would get taxed less and hence have a significant competitive advantage over the domestic firms.

- It seeks to create a clear international tax system with improved transparency and certainty for businesses and security for national tax revenues.

Disadvantages of imposing Digital Tax

- Taxing the gross revenues instead of the firm’s profits is problematic.

- The move to bring in digital tax would hurt trade ties with the US.

- It may harm start-ups– especially during their initial expansion stages.

- There is a risk of ‘double taxation’ when shifting from a ‘country-of-establishment’ principle to a ‘country-of-destination’ principle.

- These platforms and broker service providers would pass on the burden of tax to the end consumers or the sellers. This will affect their affordability and popularity.

- The government had opted for low taxation on digital businesses to promote innovation. Increasing taxes may impede global economic and technological advancement.

- Compliance with the transparency guidelines would bring in additional cost burdens on the businesses.

Issues with the Existing Taxation systems for taxing Digital Services

- The sine qua non for taxing any person in India is either he should be resident of India, or the income should accrue or arise in India or deemed to accrue or arise in India i.e., the source of income should be from India.

- Residence-based and source-based are the two criteria to tax a person. Residence-based is largely followed by the developed nations whereas the source-based principle is largely followed by the developing nations.

- India is following basically residence-based taxation; however, foreign companies are taxed in accordance with source taxation and domestic companies are taxed on residence principle.

- The rules of the Income-tax Act 1961 are very clear for taxation of domestic companies, but the rules to tax MNCs having only digital presence are not as clear as that of domestic companies.

Permanent Establishment (PE) determination issue

- To tax foreign or any entity, there needs to be two essential things: one is the jurisdiction over the entity to be taxed and the second is taxable income. Jurisdiction is established through the Permanent Establishment (PE) and taxable income is as per the tax slabs under the Income-tax act 1961.

- With the advent of digital markets/ digital economy the concept of PE has undergone drastic change.

- With the rise of digital economic activities, the conventional PE definition (brick & mortar definition) has blurred and now, the companies have significant economic presence without even having a single asset in the source state.

Digital businesses have three unique characteristics which are not considered by the current Tax regimes:

- They offer services by having limited or no physical presence. Example: Facebook, Twitter etc.

- They are highly dependent on intellectual property assets that are typically located in or can be shifted to a low-tax jurisdiction

- They can increase the value to their goods and services through highly engaged ‘user participation’ from other countries.

How are other countries handling it?

- Governments across the world, from the UK to South Korea, have been eager to collect additional revenues from the tech giants that are presently paying meagre amounts of taxes in their countries.

- While some parties believe that the firms must pay more to the state coffers, other opine that these firms must be taxed where they are based (which is the USA in most cases).

- The OECD has been involved in formulating a compromise between these two sides. In this negotiation process, over 130 countries are involved.

- These talks are co-chaired by France and the USA- countries that represent diametrically opposing stands on the issue. The talks are to decide on how this global tax regime is to work.

-Source: The Hindu

PAYMENTS INFRASTRUCTURE DEVELOPMENT FUND (PIDF) SCHEME

Context:

The Reserve Bank of India (RBI) announced operational guidelines for the Payments Infrastructure Development Fund (PIDF) scheme, aimed at encouraging deployment of more digital payments infrastructure.

Relevance:

GS-III: Indian Economy

Dimensions of the Article:

About the Payment Infrastructure Development Fund (PIDF) scheme

Recently in News: RBI launched Digital Payments Index (DPI)

About the Payment Infrastructure Development Fund (PIDF) scheme

- The Payment Infrastructure Development Fund (PIDF) will be operational for three years effective from 2021 (and may be extended for 2 more years) and this fund is created for development of payment acceptance infrastructure in tier-3 to tier-6 cities (centres), with a special focus on the north-eastern states of the country.

- The focus of using funds from PIDF is targeted at those merchants who are yet to be terminalised (merchants who do not have any payment acceptance device).

- The fund will be used to subsidize banks and non-banks for deploying payment infrastructure, which will be contingent upon specific targets being achieved.

- Tentatively, tier-3 and tier-4 centres will be allocated 30% of the acceptance devices, tier-5 and tier-6 centres will get 60% and the north eastern states will be given 10%.

- Multiple payment acceptance devices and infrastructure supporting underlying card payments, such as physical Point of Sale, mobile Point of Sale, General Packet Radio Service (GPRS) , Public Switched Telephone Network (PSTN) and QR code-based payments will be funded under the scheme.

- An Advisory Council (AC) under the chairmanship of RBI deputy governor has been constituted for managing the PIDF.

- Besides the initial corpus, PIDF shall also receive annual contributions from card networks and card issuing banks.

Recently in News: RBI launched Digital Payments Index (DPI)

The Reserve Bank of India (RBI) announced a Digital Payments Index (DPI) to assess and capture the extent of digitalization of payments effectively.

Click Here to read more about the DPI launched by RBI – The article covers Different digital payment modes in India as well.

-Source: Livemint

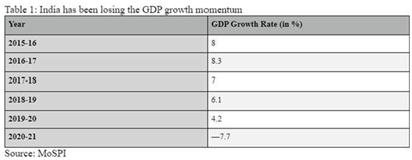

GDP LIKELY TO CONTRACT BY 7.7% IN 2020-21 ACCORDING TO FAE

Context:

The Ministry of Statistics and Programme Implementation released the First Advance Estimates (FAE) for the current financial year according to which India’s real Gross Domestic Product (GDP) is estimated to contract by 7.7% in 2020-21, compared to a growth rate of 4.2% in 2019-20, with Real GVA (Gross Valued added) shrinking by 7.2%.

Relevance:

GS-III: Indian Economy

Dimensions of the Article:

- What are the First Advance Estimates of GDP?

- How are the FAE arrived at before the end of the concerned financial year?

- Highlights of the First Advance Estimates for 2020-21

- Sector-based Data from FAE

What are the First Advance Estimates of GDP?

- For any financial year, the MoSPI provides regular estimates of GDP. The first such instance is through the FAE.

- The FAE for any particular financial year is typically presented on January 7th.

- The significance of FAE lies in the fact that they are the GDP estimates that the Union Finance Ministry uses to decide the next financial year’s Budget allocations.

- The FAE will be quickly updated as more information becomes available.

How are the FAE arrived at before the end of the concerned financial year?

The FAE are derived by extrapolating the available data. According to the MoSPI, the approach for compiling the Advance Estimates is based on Benchmark-Indicator method.

The sector-wise estimates are obtained by extrapolating indicators such as:

- Index of Industrial Production (IIP) of first 7 months of the financial year

- Financial performance of listed companies in the private corporate sector available up to quarter ending September, 2020

- The 1st Advance Estimates of crop production

- The accounts of central & state governments

- Information on indicators like deposits & credits, passenger and freight earnings of Railways, passengers and cargo etc., available for first 8 months of the financial year.

Highlights of the First Advance Estimates for 2020-21

GDP Growth Rate

- The 7.7 per cent contraction in GDP that is estimated in the FAE is a sharp one considering that India has registered an average annual GDP growth rate of 6.8 per cent since the start of economic liberalisation in 1992-93.

- But, a big reason for the contraction this year has been the disruption caused by Covid-induced lockdowns which saw the economy contract by almost 24 per cent in the first quarter.

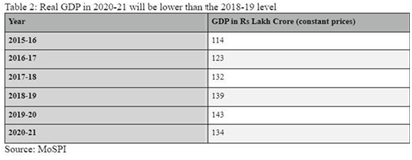

Absolute level of real GDP

- India’s real GDP — that is, GDP without the influence of inflation — in 2020-21 will be lower than the 2018-19 level (dropping from 143 Lakh crores to 134 lakh crores).

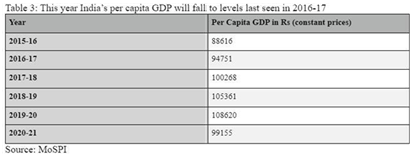

Per Capita GDP

- India’s per capita GDP will fall to less than Rs. 1 Lakh – which was last seen 4 years ago.

- While the overall real GDP will fall by 7.7 per cent, per capita real GDP will fall by 8.7 per cent.

- Per capita GDP is a better variable if one wants to understand how an average India has been impacted.

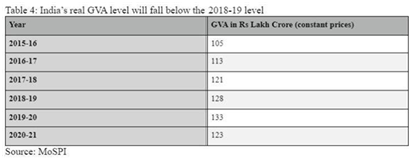

Absolute level of real Gross Value Added (or GVA)

- The Gross Value Added provides a picture of the economy from the supply side. It maps the value-added by different sectors of the economy such as agriculture, industry and services.

- In other words, GVA provides a proxy for the income earned by people involved in the various sectors.

- India’s real GVA level, too, will fall below the 2018-19 level.

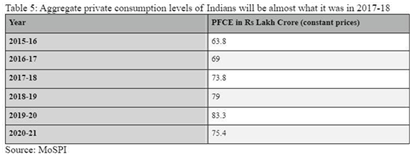

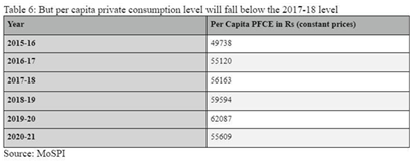

Private Final Consumption Expenditure (PFCE)

- The biggest demand for goods and services comes from private individuals trying to satisfy their consumption needs.

- This demand is called PFCE and it constitutes over 56 per cent of the total GDP.

- PFCE levels will be almost what they were in 2017-18 and per capita PFCE levels will fall below what they were in 2017-2018.

Sector Based Data from the FAE

Just two sectors are estimated to record positive growth in GVA this year, with:

- Agriculture continuing its strong run through the first half of year to the second half (3.4%) and

- Electricity, Gas, Water Supply & Other Utility services (2.7%).

The sharpest decline in the pandemic-dented year is expected in

- Trade, Hotels, Transport, Communication and Services related to broadcasting (more than 20% decline)

- Construction (more than 12% decline)

- Mining and quarrying (more than 12% decline) and

- Manufacturing (almost 10% decline)

Public administration, defence and other services are also projected to contract by almost 4%.

- Financial, Real Estate and Professional Services shall record a marginal decline (less than 1%) year-on-year, as per the advanced estimates.

- Government expenditure is expected to show a robust growth of 17% in the second half of the year, despite the challenges faced by the government on fiscal consolidation and the fact that government expenditure fell by almost 4% in the first half of the year.

-Source: The Hindu, Indian Express

SUDDEN STRATOSPHERIC WARMING (SSW)

Context:

A recent study has found that the dramatic meteorological event known as Sudden Stratospheric Warming (SSW) unfolding high above the North Pole may be behind very cold weather in large parts of the world currently.

Relevance:

GS-I: Geography

Dimensions of the Article:

- What is the Stratosphere?

- What is Sudden stratospheric warming (SSW)?

- What is a Polar vortex?

- Impact of SSW on weather

- What the latest study on SSW found?

What is the Stratosphere?

- The stratosphere is the second major layer of Earth’s atmosphere, just above the troposphere, and below the mesosphere.

- The stratosphere is stratified (layered) in temperature, with warmer layers higher and cooler layers closer to the Earth.

- The increase of temperature with altitude in the Stratosphere is a result of the absorption of the Sun’s ultraviolet radiation (shortened UV) by the ozone layer. (This is in contrast to the troposphere, near the Earth’s surface, where temperature decreases with altitude.)

- The border between the troposphere and stratosphere, the tropopause, marks where this temperature inversion begins.

- Near the equator, the lower edge of the stratosphere is as high as 20 km, at midlatitudes around 10 km and at the poles about 7 km.

- Temperatures range from an average of −51 °C near the tropopause to an average of −15 °C near the mesosphere.

- Winds in the stratosphere can far exceed those in the troposphere, reaching near 60 m/s in the Southern polar vortex.

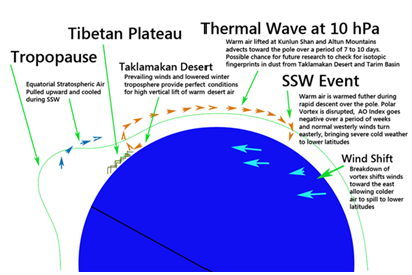

What is Sudden stratospheric warming (SSW)?

- A sudden stratospheric warming (SSW) is an event in which the polar stratospheric temperature rises by several tens of kelvins (up to increases of about 50°C (90°F)) over the course of a few days.

- The change is preceded by a situation in which the Polar jet stream of westerly winds in the winter hemisphere is disturbed by natural weather patterns or disturbances in the lower atmosphere.

- SSW is closely associated with polar vortex breakdown.

- In a usual northern-hemisphere winter, several minor warming events occur, with a major event occurring roughly every two years. One reason for major stratospheric warmings to occur in the Northern hemisphere is because orography and land-sea temperature contrasts are responsible for the generation of long Rossby waves in the troposphere.

- These waves travel upward to the stratosphere and are dissipated there, decelerating the westerly winds and warming the Arctic.

- This is the reason that major warmings are only observed in the northern-hemisphere, with two exceptions. In 2002 and 2019, southern-hemisphere major warmings were observed which are not fully understood.

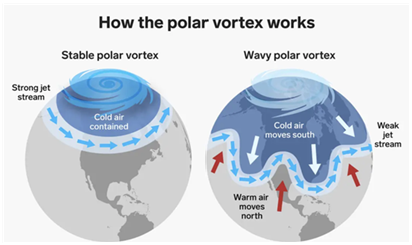

What is a Polar vortex?

- A polar vortex is a persistent, large-scale, upper-level low-pressure area, less than 1,000 kilometers in diameter, that rotates counter-clockwise at the North Pole and clockwise at the South Pole (called a cyclone in both cases), i.e., both polar vortices rotate eastward around the poles.

- The vortices weaken and strengthen from year to year.

- As with other cyclones, their rotation is driven by the Coriolis effect.

Impact of SSW on weather

- Although sudden stratospheric warmings are mainly forced by planetary scale waves which propagate up from the lower atmosphere, there is also a subsequent return effect of sudden stratospheric warmings on surface weather.

- Following a sudden stratospheric warming, the high altitude westerly winds reverse and are replaced by easterlies.

- The easterly winds progress down through the atmosphere, often leading to a weakening of the tropospheric westerly winds, resulting in dramatic reductions in temperature in Northern Europe.

- This process can take a few days to a few weeks to occur.

What the latest study on SSW found?

- During an SSW, polar stratospheric temperature can increase by up to 50 degrees Celsius over the course of a few days. Such events are often followed by very cold weather, especially heavy snow storms.

- They analysed 40 observed SSW events that occurred over the last 60 years and developed a novel method for tracking the signal of an SSW downward from its onset in the stratosphere to the surface.

- There was an increased chance of extreme cold and potentially snow, over the next week or two.

- The latest SSW was potentially the most dangerous kind, where the polar vortex split into two smaller ‘child’ vortices.

-Source: Down To Earth Magazine