Contents

- Slower growth and a tighter fiscal

- Contempt for labour: On dilution of labour laws

- Raghuram Rajan explains: How best to stimulate economy?

SLOWER GROWTH AND A TIGHTER FISCAL

Focus: GS-III Indian Economy

Introduction

- Various institutions have assessed India’s growth prospects for 2020-21 ranging from 0.8% (Fitch) to 4.0% (Asian Development Bank).

- This wide range indicates the extent of uncertainty and tentative nature of these forecasts.

- The International Monetary Fund (IMF) has projected India’s growth at 1.9%, China’s at 1.2%, and the global growth at (-) 3.0%.

The actual growth outcome for India would depend on:

- the speed at which the economy is opened up;

- the time it takes to contain the spread of virus,

- the government’s policy support.

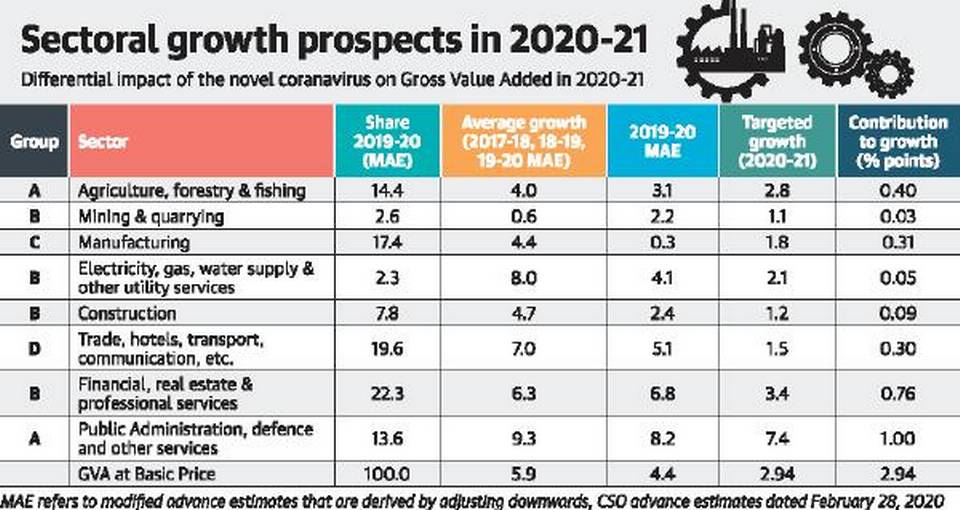

Growth prospects

- In 2019-20, which would serve as the base year, India may show (Gross Value Added) GVA growth of about 4.4%

- GVA is divided into eight broad sectors, and although all sectors have been disrupted, some may be affected less than the others.

We divide the output sectors in four groups:

Group A – Agriculture and allied sectors, and Public administration, Defence and other services.

- In the case of agriculture, rabi crop is currently being harvested and a good monsoon is predicted later in the year.

- Despite some labour shortage issues, this sector may show near-normal performance.

- The public and defence services have been nearly fully active, with the health services at the forefront of the COVID-19 fight.

- For the group A sectors, it may be possible to achieve 90% of the 2019-20 growth performance.

Group B – Mining and Quarrying, Electricity, Gas, Water supply and other Utility services, Construction, and Financial, Real estate and Professional services.

- These four sectors may suffer average disruption showing 50% of 2019-20 growth performance.

Group C – Manufacturing.

- Manufacturing has suffered significant growth erosion in 2019-20. It is feasible to stimulate this sector by supporting demand.

Group D – Trade, Hotels, Transport, Storage and Communications.

- This sector may be able to show 30% of 2019-20 growth performance.

GVA Forecast

- Considering these four groups together, a GVA growth of 2.9% is estimated for 2020-21.

- Realising this requires strong policy support, particularly for the manufacturing sector which has a weight of 17.4%.

- It is also based on the assumption that the Indian economy may move on to positive growth after the first quarter.

- In the first quarter, GVA growth will be negative.

Calibrating policy support

- Monetary policy initiatives undertaken so far include a reduction in the repo rate to 4.4%, the reverse repo rate to 3.75%, and cash reserve ratio to 3%.

- The Reserve Bank of India has also opened several special financing facilities.

- These actions will have a positive impact on output only after the lockdown is lifted.

- These measures need to be supplemented by an appropriate fiscal stimulus.

- With lower petroleum prices, fertilizer and petroleum subsidies may be reduced.

- These expenditure cuts are contemplated to keep the fiscal deficit under some control.

On fiscal deficit

Fiscal stimulus can be of three types:

- Relief expenditure for protecting the poor and the marginalised

- Demand-supporting expenditure for increasing personal disposable incomes or government’s purchases of goods and services, including expanded health-care expenditure imposed by the novel coronavirus

- Bailouts for industry and financial institutions.

The Centre’s budgeted fiscal deficit of 3.5% of GDP may have to be enhanced substantially to make up for the shortfall in budgeted revenues; account for a lower than projected nominal GDP for 2020-21, and provide for a stimulus.

Thus, the Centre’s fiscal deficit may increase to 6.0% of GDP.

Expenditure on construction of hospitals, roads and other infrastructure and purchase of health-related equipment and medicines require prioritisation.

Financing of the fiscal deficit poses a major challenge this year.

-Source: The Hindu

RAGHURAM RAJAN EXPLAINS: HOW BEST TO STIMULATE ECONOMY?

Focus: GS-III Indian Economy

Introduction

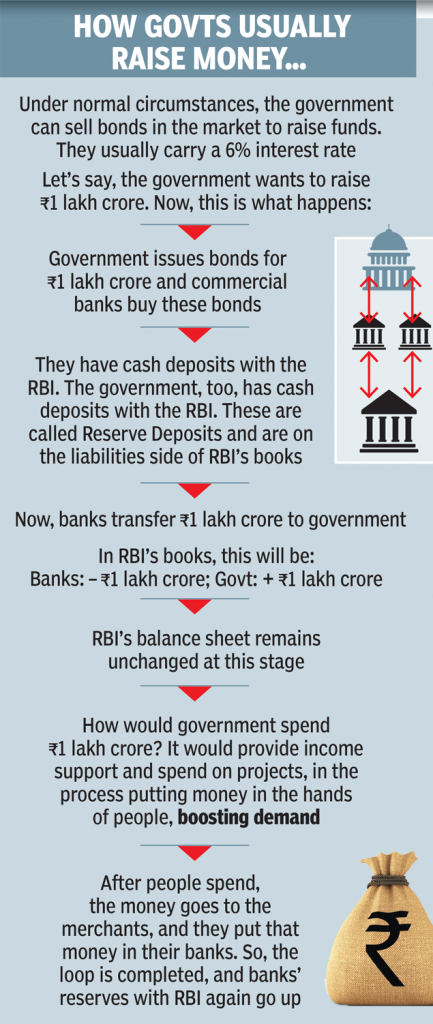

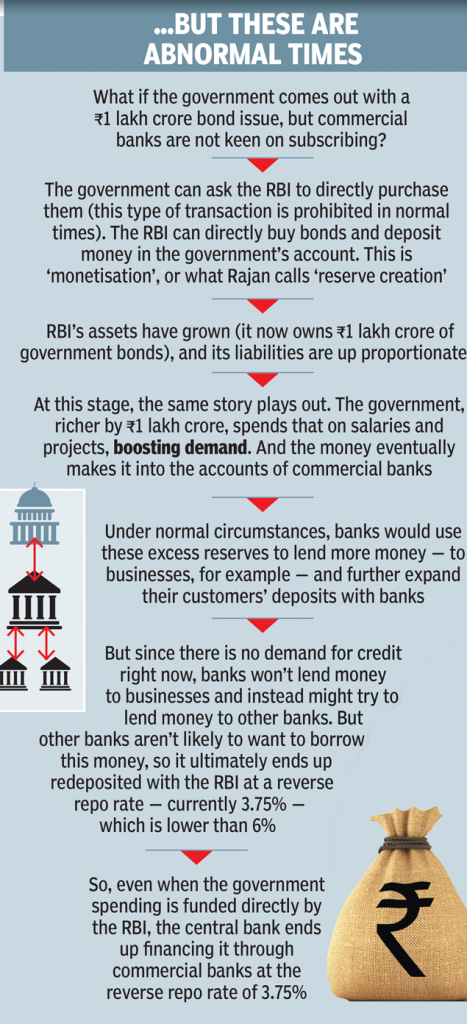

- To fund a bigger public spending programme, the government can either ask the RBI to print more money (monetise the deficit) or it can issue new bonds to be subscribed by the banks (raise money through borrowing).

- The Former RBI governor Raghuram Rajan explained how the two paths work and why ‘monetisation’ is a good option in the short-term and within reasonable limits

Highlights

Government finances itself from RBI while RBI finances itself from the banks at the reverse repo rate of 3.75% – Hence, RBI’s Direct Funding is termed as Printing Money wrongly.

RBI’s Direct Funding represents a loss to the government in two ways:

- A reduction in the annual dividend RBI pays the government

- Banks get 3.75% instead of the 6% they could get by buying government bonds directly.

Since the government owns 70% of the banking sector, its dividends from public sector banks also fall commensurately.

Will it Fuel Inflation?

Such direct financing is “not inflationary per se” as long as banks are reluctant to lend further to business or consumers.

However, as normal times return, RBI will have to pay a higher rate on excess reserves, or sell its government bond holdings and extinguish excess reserves, else it will risk excessive credit expansion and inflation.

-Source: Times of India

CONTEMPT FOR LABOUR: ON DILUTION OF LABOUR LAWS

Focus: GS-II Social Justice, Governance

Introduction

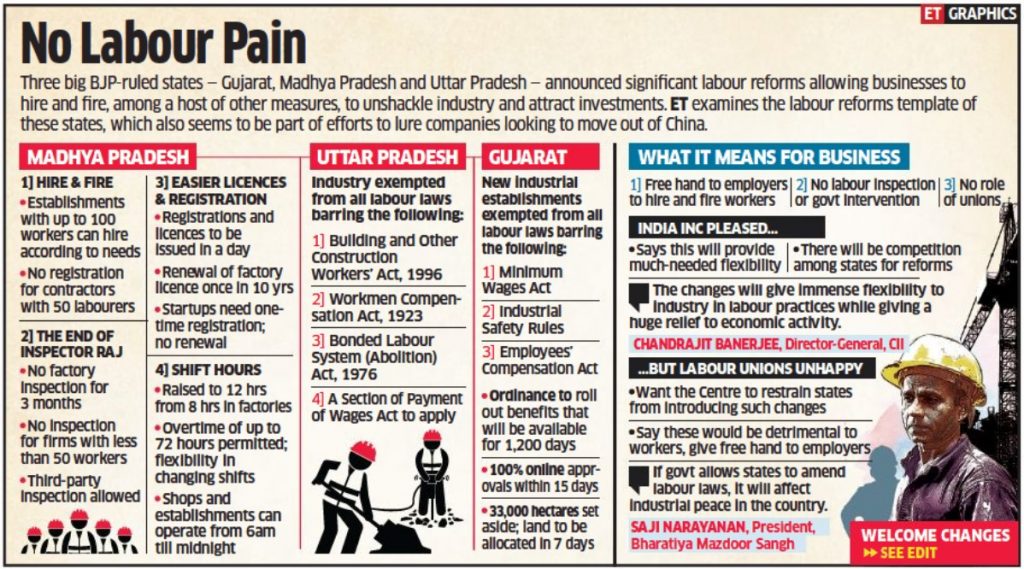

It is amoral and perverse on the part of some States to address this need, for revival of business and economic activity, by granting sweeping exemptions from legal provisions aimed at protecting labourers and employees in factories, industries and other establishments.

What actions have states taken?

- Madhya Pradesh will be allowing units to be operated without many of the requirements of the Factories Act — working hours may extend to 12 hours, instead of eight, and weekly duty up to 72 hours.

- This exemption can be given only during a ‘public emergency’, defined in a limited way as a threat to security due to war or external aggression.

- Uttar Pradesh has approved an ordinance suspending for three years all labour laws, save a few ones relating to the abolition of child and bonded labour, women employees, construction workers and payment of wages, besides compensation to workmen for accidents while on duty.

- Changes in the manner in which labour laws operate in a State may require the Centre’s assent.

Conclusion

- Centre is pursuing a labour reform agenda through consolidated codes for wages, industrial relations and occupational safety, health and working conditions.

- The most egregious aspect of the country’s response to the pandemic was its inability to protect the most vulnerable sections and its vast underclass of labourers from its impact.

- The emphasis in the initial phase was on dealing with the health crisis, even when the consequence was the creation of an economic crisis.

- Concerns are to be raised against a government relieving factories of even elementary duties such as providing drinking water, first aid boxes and protective equipment, cleanliness, ventilation, lighting, canteens, restrooms and crèches.

-Source: The Hindu, Economic Times