Contents

- J&K tribal population to get their due: Forest Rights Act

- Council may bring petrol and diesel under GST

- India, Singapore to link their fast payment systems

- Agriculture Ministry inks MoU with 5 firms

J&K tribal population to get their due: Forest Rights Act

Context:

After a long delay, the Jammu and Kashmir government has decided to implement the Forest Rights Act, 2006, which will elevate the socio-economic status of a sizeable section of the 14-lakh-strong population of tribals and nomadic communities, including Gujjar-Bakerwals and Gaddi-Sippis, in the Union Territory.

Relevance:

GS-II: Social Justice (Issues Related to SCs & STs, Management of Social Sector/Services, Government Policies and Interventions), Prelims

Dimensions of the Article:

- Forest Rights Act, 2006

- Challenges in implementation of the Forest Right Act

- About the tribal communities in focus

Forest Rights Act, 2006

- Schedule Tribes and Other Forest Dwellers Act or Recognition of Forest Rights Act came into force in 2006. The Nodal Ministry for the Act is Ministry of Tribal Affairs.

- It has been enacted to recognize and vest the forest rights and occupation of forest land in forest dwelling Scheduled Tribes and other traditional forest dwellers, who have been residing in such forests for generations, but whose rights could not be recorded.

- This Act not only recognizes the rights to hold and live in the forest land under the individual or common occupation for habitation or for self-cultivation for livelihood, but also grants several other rights to ensure their control over forest resources.

- The Act also provides for diversion of forest land for public utility facilities managed by the Government, such as schools, dispensaries, fair price shops, electricity and telecommunication lines, water tanks, etc. with the recommendation of Gram Sabhas.

- Rights under the Forest Right Act 2006:

- Title Rights- ownership of land being framed by Gram Sabha.

- Forest management rights– to protect forests and wildlife.

- Use rights- for minor forest produce, grazing, etc.

- Rehabilitation– in case of illegal eviction or forced displacement.

- Development Rights– to have basic amenities such as health, education, etc.

Challenges in implementation of the Forest Right Act

- Adivasi lands in Jammu and Kashmir have not been protected, nor have these communities been given ownership rights. Instead, evictions of Adivasis have intensified in the last few years.

- A series of legislation– amendments to the Mines and Minerals (Development and Regulation) Act, the Compensatory Afforestation Fund Act and a host of amendments to the Rules to the FRA- undermine the rights and protections given to tribal in the FRA, including the condition of “free informed consent” from gram Sabhas for any government plans to remove tribal from the forests and for the resettlement or rehabilitation package.

- The process of documenting communities’ claims under the FRA is intensive — rough maps of community and individual claims are prepared democratically by Gram Sabhas. These are then verified on the ground with annotated evidence, before being submitted to relevant authorities.

- There is a reluctance of the forest bureaucracy to give up control with FRA being seen as an instrument to regularise encroachment. This is seen in its emphasis on recognising individual claims while ignoring collective claims — Community Forest Resource (CFR) rights as promised under the FRA — by tribal communities. To date, the total amount of land where rights have been recognised under the FRA is just 3.13 million hectares, mostly under claims for individual occupancy rights.

- In almost all States, instead of Gram Sabhas, the Forest Department has either appropriated or been given effective control over the FRA’s rights recognition process. This has created a situation where the officials controlling the implementation of the law often have the strongest interest in its non-implementation, especially the community forest rights provisions, which dilute or challenge the powers of the forest department.

- Saxena Committee pointed out several problems in the implementation of FRA. Wrongful rejections of claims happen due to lack of proper enquiries made by the officials.

About the tribal communities in focus

Gujjar-Bakerwals:

- Gujjars and Bakerwals are listed as Scheduled Tribes in Jammu and Kashmir.

- They inhabit the high mountain ranges of Jammu and Kashmir. They are a nomadic tribe and seasonally migrate from one place to another with their sheep and goat herds. They travel higher up the mountains and lower down to plains according to seasonal variation.

Gaddi-Sippis:

- Gaddis and Sippis communities are semi-nomadic tribes having a special characteristic feature of living in dhoks (meadows) in the last inhabited areas of the five districts of Udhampur, Doda, Kathua, Reasi and Ramban of Jammu and Kashmir.

-Source: The Hindu

Council may bring petrol and diesel under GST

Context:

The GST Council might consider taxing petrol, diesel and other petroleum products under the single national GST regime in the upcoming meeting in Lucknow, a move that may require huge compromises by both central and state governments on the taxing these products.

Relevance:

GS-III: Indian Economy (Economic Development of India, Macroeconomics- Taxation)

Dimensions of the Article:

- What is GST?

- GST Council

- Matters on which GST Council makes recommendations

- Current Pricing of Petrol and Diesel

- How much tax we pay on petrol and diesel?

- Bringing Fuel under GST

- Impact of bringing Fuel under GST

What is GST?

- GST is a destination-based indirect tax and is levied at the final consumption point. Under it, the final consumer of the goods and services bear the tax charged in the supply chain. GST is a transparent and fair system that prevents black money and corruption and promotes new governance culture.

GST Act

- Goods and Services Tax (GST) Act came into effect in 2017.

- Goods and Services Tax (GST) was introduced by the Government of India to boost the economic growth of India. GST is considered to be the biggest taxation reform in the history of the Indian economy.

- The power to make any changes in the GST law is in the hands of the GST Council. GST Council is headed by the Finance Minister. One hundred and first amendment act, 2016 introduced the GST in India in July 2017.

GST Council

- Goods & Services Tax Council is a constitutional body for making recommendations to the Union and State Government on issues related to Goods and Service Tax.

- As per Article 279A (1) of the amended Constitution, the GST Council has to be constituted by the President within 60 days of the commencement of Article 279A.

- The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2016, for the introduction of Goods and Services Tax in the country was introduced in the Parliament and passed by Rajya Sabha on 3rd August 2016 and by Lok Sabha on 8th August 2016.

- GST Council is an apex member committee to modify, reconcile or procure any law or regulation based on the context of goods and services tax in India.

- The GST council is responsible for any revision or enactment of rule or any rate changes of the goods and services in India.

- The council contains the following members:

- Union Finance Minister (as chairperson)

- Union Minister of States in charge of revenue or finance (as members)

- The ministers of states in charge of finance or taxation or other ministers as nominated by each state’s government (as members).

Matters on which GST Council makes recommendations

- Taxes, cesses, and surcharges levied by the Centre, States and local bodies which may be subsumed in the GST;

- Goods and services which may be subjected to or exempted from GST;

- Model GST laws, principles of levy, apportionment of IGST and principles that govern the place of supply;

- Threshold limit of turnover below which goods and services may be exempted from GST;

- Rates including floor rates with bands of GST;

- Special rates to raise additional resources during any natural calamity;

- Special provision with respect to Arunachal Pradesh, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand; and

- Any other matter relating to the goods and services tax, as the Council may decide.

Current Pricing of Petrol and Diesel

- As per the latest (as of March 2021) price-build of petrol and diesel: State taxes had a smaller contribution to the retail price than central taxes.

- While the state Value Added Tax (VAT) was just over 10 and 20 rupees, on diesel and petrol respectively, the union excise duties for both petrol and diesel exceeded 30 Rs.

- These headline numbers suggest that the centre is a bigger beneficiary of tax incomes from the sale of petrol and diesel.

- This is because FFC’s earmarked share of states in centre’s revenues applies to what is called the divisible pool of taxes, which excludes cess and other forms of special taxes. Overtime, the weight of cess and other such non-sharable taxes has been increasing in the centre’s gross tax revenue. This, in practice, has meant that the share of states in gross total revenue of the centre has never reached 41% and in fact gone down overtime.

How much tax we pay on petrol and diesel?

- The Union and state levies put together account for roughly 55 per cent and 52 per cent of the retail price of petrol and diesel respectively.

- These work out to around 135 per cent and 116 per cent of the base prices of the two products respectively.

- The central levy on petrol and diesel works out to around 36 per cent of the retail price while the state component is around 20 per cent (diesel) to 28 per cent (petrol).

- Of the total central levies on petrol and diesel, Rs 1.40 per litre and Rs 1.80 per litre is the basic excise duty for the two fuels, and Rs 11 per litre and Rs 18 per litre is the special additional excise duty.

- Both these components form part of the divisible pool of taxes i.e. 42 per cent of which (approximately Rs 52,000 crore) goes to the states.

- The remaining portion of Rs 18 per litre in both cases is the Road and Infrastructure Cess and Rs 2.50 per litre and Rs 4 per litre is the Agriculture Infrastructure and Development Cess which are retained by the Centre.

Bringing Fuel under GST

- Economists have said that bringing petrol and diesel under the goods and services tax is an unfinished agenda of the GST framework and getting the prices under the new indirect taxes framework can help.

- Centre and states are loathing to bring crude oil products under the GST regime as sales tax/VAT (value added tax) on petroleum products is a major source of own tax revenue for them.

- Thus, there is lack of political will to bring crude under the ambit of GST.

- At present, states choose to levy a combination of ad valorem tax, cess, extra VAT/surcharge based on their needs and these taxes are imposed after taking into account the crude price, the transportation charge, the dealer commission and the flat excise duty imposed by the Centre.

Impact of bringing Fuel under GST

- A growth in the consumption – diesel going up 15 per cent and petrol by 10 per cent – has been used to assess the Rs 1 lakh crore fiscal impact of getting petroleum prices under GST.

- States, which have the highest share of tax revenues at present, will be the biggest losers if the system shifts to GST.

- However, such a move will help consumers pay up to Rs 30 less per liter of fuel. This is because he highest slab under the existing GST rates is 28%. Even if petrol and diesel were to be taxed at the highest rate, the post-tax price will be much lower than what43 it is currently.

Loss of revenue

- A 28 per cent levy of GST on the base price would fetch around Rs 5.40 per litre on petrol and around Rs 5.45 on diesel to the central and each of the state governments.

- Contrast the above with the current yield of Rs 32.90 per litre on petrol and Rs 31.80 per litre on diesel to the Centre alone and an average of around Rs 20 per litre and Rs 15 per litre on petrol and diesel, respectively, to each of the states.

- This, however, would bring down the prices of petrol and diesel to around Rs 55 per litre.

- This would translate into a revenue loss of around Rs 3 lakh crore on account of petrol and around Rs 1.1 lakh crore on account of diesel to the Centre and the states, at current volumes.

Loss of autonomy

- Once petrol and diesel are subsumed within the GST, both the Centre and states will have to give away the current autonomy they enjoy with these taxes which serve twin purposes of counter-cyclical interventions in the realm of both politics and economy.

- For example, both the Centre and the states increased taxes on petrol and diesel to compensate for revenue loss during the lockdown.

- The central taxes on petrol and diesel are a fixed amount per litre rather than a fraction of the base price, which is how GST is levied currently.

- Also, the current regime allows individual state governments to change their taxes – poll bound Assam has reduced taxes on petrol-diesel – a leeway which will not exist once they are subsumed within GST, as taxes will have to be uniform across the country.

-Source: The Hindu

India, Singapore to link their fast payment systems

Context:

The Reserve Bank of India (RBI) and the Monetary Authority of Singapore (MAS) announced a project to link their respective fast payment systems — Unified Payments Interface (UPI) and PayNow which will facilitate instant low-cost cross border fund transfer.

Relevance:

GS-III: Indian Economy (Growth and Development of Indian Economy, Monetary Policy, Inflation)

Dimensions of the Article:

- What is Unified Payments Interface (UPI)?

- About the India-Singapore linking of UPI and PayNow

- India–Singapore relations

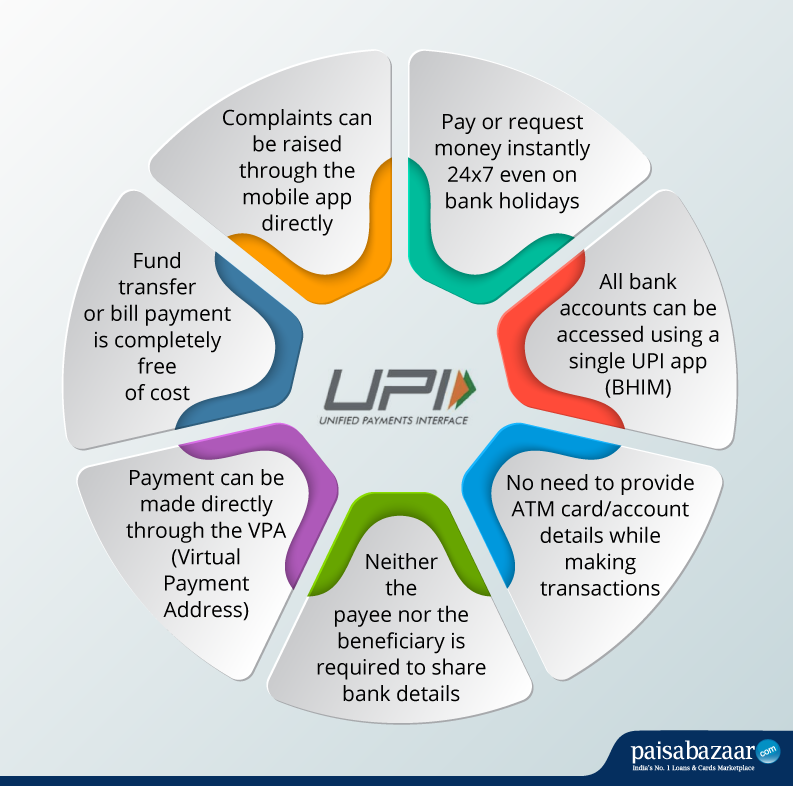

What is Unified Payments Interface (UPI)?

- Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments into one hood.

- Advantages of UPI Includes – Immediate money transfer through mobile device round the clock 24*7 and 365 days.

- UPI Enables Single mobile application for accessing different bank accounts with Single Click 2 Factor Authentication – Aligned with the Regulatory guidelines yet provides for a very strong feature of seamless single click payment.

- It also features Virtual address of the customer for Pull & Push providing for incremental security with the customer not required to enter the details such as Card no, Account number; IFSC etc.

About the India-Singapore linking of UPI and PayNow

- The project to link the fast payment systems of both the countries was announced by Reserve Bank of India (RBI) and Monetary Authority of Singapore (MAS).

- This linked payment interface is expected to be operationalised by July 2022.

- Linked interface will help in making instant, low-cost fund transfers on a reciprocal basis without onboarding onto the other payment system.

- The linkage will be a significant milestone for the development of infrastructure for cross-border payments between both the countries. It will also align with the \ G20’s financial inclusion priorities to provide for faster, cheaper and more transparent cross-border payments.

What is PayNow?

- PayNow is the fast payment system of Singapore, enabling peer-to-peer funds transfer service. It is available for retail customers with the help of participating banks & Non-Bank Financial Institutions (NFIs) in Singapore. It provides the users to send and receive instant funds from one bank or e-wallet account to another by using their mobile number, Singapore NRIC/FIN, or VPA.

India–Singapore relations

- India-Singapore relations have traditionally been strong and friendly, with the two nations enjoying extensive cultural and commercial relations.

- India and Singapore share long-standing cultural, commercial and strategic relations, with Singapore being a part of the “Greater India” cultural and commercial region.

- Following its independence in 1965, Singapore was concerned with China-backed communist threats as well as domination from Malaysia and Indonesia and sought a close strategic relationship with India, which it saw as a counterbalance to Chinese influence and a partner in achieving regional security.

- Although the rival positions of both nations over the Vietnam War and the Cold War caused consternation between India and Singapore, their relationship expanded significantly in the 1990s; Singapore was one of the first to respond to India’s “Look East” Policy of expanding its economic, cultural and strategic ties in Southeast Asia to strengthen its standing as a regional power

- Ethnic Indians constitute about 9.1% or around 3.5 lakhs of the resident population of 3.9 million in Singapore. More than 500,000 people of Indian origin live in Singapore.

- Singapore is India’s 2nd largest trade partner among ASEAN countries.

- The India–Singapore Comprehensive Economic Cooperation Agreement, also known as the Comprehensive Economic Cooperation Agreement or simply CECA, is a free trade agreement between Singapore and India to strengthen bilateral trade- signed in 2005.

- Singapore had always been an important strategic trading post, giving India trade access to the Far East.

- Singapore participates in Indian Ocean Naval Symposium (IONS) and multilateral Exercise MILAN hosted by Indian Navy.

- Singapore’s membership of Indian Ocean Rim Association (IORA) and India’s membership of ADDM+ (ASEAN Defence Ministers’ Meeting – Plus) provides a platform for both countries to coordinate positions on regional issues of mutual concern.

- Both the countries successfully conducted the 27th edition of Singapore-India Maritime Bilateral Exercise (SIMBEX) and also participated in the second edition of the Singapore-India-Thailand Maritime Exercise (SITMEX), both held in November 2020.

-Source: The Hindu

Agriculture Ministry inks MoU with 5 firms

Context:

Recently, the Ministry of Agriculture and Farmers Welfare signed 5 Memorandums of Understanding (MOUs) with private companies for taking forward Digital Agriculture.

These pilot projects are part of the Digital Agriculture Mission and will draw on the National Farmers Database which already includes 5.5 crore farmers identified using existing national schemes.

Relevance:

GS-III: Indian Economy (Growth and Development of Indian Economy, Monetary Policy, Inflation)

Dimensions of the Article:

- Digital Agriculture

- Digital Agriculture mission

- Highlights of the recent MOUs signed by the Ministry of Agriculture and Farmers Welfare

Digital Agriculture

Digital Agriculture is “ICT (Information and Communication Technologies) and data ecosystems to support the development and delivery of timely, targeted information and services to make farming profitable and sustainable while delivering safe nutritious and affordable food for all.”

Examples of Digital Agriculture

- Agricultural biotechnology is a range of tools, including traditional breeding techniques, that alter living organisms, or parts of organisms, to make or modify products; improve plants or animals; or develop microorganisms for specific agricultural uses.

- Precision agriculture (PA) is an approach where inputs are utilised in precise amounts to get increased average yields, compared to traditional cultivation techniques such as agroforestry, intercropping, crop rotation, etc. It is based on using ICTs.

- Digital and wireless technologies for data measurement, Weather monitoring, Robotics/drone technology, etc.

Digital Agriculture mission

- The Digital Agriculture mission was launched by the Ministry of Agriculture & Farmers Welfare for a period of five years (2021 -2025).

- The mission aims to achieve rapid development in the Indian Agriculture Sector through the use of the latest technologies. These include technologies such as artificial intelligence, blockchain technology, remote sensing and Geographic information systems technology (GIS), usage of drones and robotics.

- The focus is on projects based on new technologies such as artificial intelligence, blockchain, use of drones, remote sensing and GIS technology and robots etc.

Highlights of the recent MOUs signed by the Ministry of Agriculture and Farmers Welfare

- As per Agriculture Ministry, Jio Platforms Limited will conduct its pilot project in order to provide advisories for farmers in Jalna & Nasik districts of Maharashtra.

- ITC Limited has signed MoU in a bid to build a “Customized ‘Site Specific Crop Advisory’ service.”

- MoU with the ITC limited will help in implementing the proposal in identified villages of Sehore and Vidisha districts of Madhya Pradesh. It will support Wheat crop operations.

- MoU with Cisco will “conceptualize the Proof of Concept in effective knowledge sharing between farmers, administration, academia and industry” in Kaithal district of Haryana and Morena district of Madhya Pradesh.

- MoU with NCDEX e Markets Limited (NeML) will look after four services–Market Linkages, Financial Linkages, Aggregation of demand, and Data Sanitization in three districts namely, Guntur (Andhra Pradesh), Nasik (Maharashtra) and Devanagere (Karnataka).

- Ninjacart will help in the development and hosting the Agri Marketplace Platform (AMP). It will bring all the participants in post-harvest market linkage together. As per MoU, Proof of Concept (POC) will be conducted in Anand (Gujarat), Chhindwara (Madhya Pradesh) and Indore (Madhya Pradesh).

-Source: PIB, Indian Express