Contents

- Show commitment to equity in the Budget

- Impending Global minimum tax rate implementation

Show Commitment to Equity in the Budget

Context:

The Budget Session of the parliament commenced from January 31 with President’s address and this provides the government with an opportunity to show commitment to equity in the Union Budget session by discussing inequality.

Relevance:

GS-III: Indian Economy (Growth and Development of Indian Economy, Inclusive Growth), GS-II: Polity and Constitution (Constitutional Provisions, DPSPs)

Dimensions of the Article:

- The need for new focus on inequality in the budget

- Looking outside what the reports tell us

- Other Challenges that exacerbate the economic inequality problem in India

- Constitutional Provisions in DPSP to eliminate inequality

- Way forward

The need for new focus on inequality in the budget

Oxfam Inequality Report 2022

- On January 17, 2022, Oxfam International presented its annual global “Inequality Report” titled Inequality Kills. This report showed the impoverishment of millions of working people while a miniscule few recorded a quantum growth in wealth.

- The Oxfam inequality report of 2022 also revealed that more than half the world’s NEW poor are from India.

- According to the report 84% Indian households have suffered a loss of income, with 4.6 crore people falling into extreme poverty during the novel coronavirus pandemic. At the same time – the richest 142 people have more than doubled their wealth to more than ₹53 lakh-crore.

- The fact that 84% of Indian households have suffered a loss of income, with 4.6 crore people falling into extreme poverty while just over a 100 people have doubled their wealth goes on to show that the government policies are merely paying lip service to the poor while supporting the rich.

World Inequality Report 2022

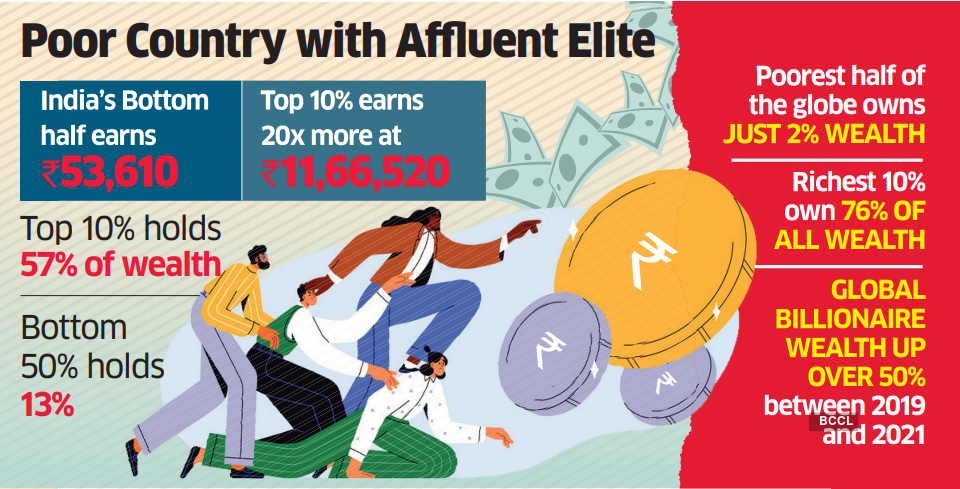

- India stands out as a “poor and very unequal country, with an affluent elite”, where the top 10 per cent holds 57% of the total national income while the bottom 50%’s share is just 13% in 2021.

- The economic reforms and liberalization adopted by India have mostly benefited the top 1%.

- Average Household Wealth in India stands at Rs. 983,010. It has been observed that the deregulation and liberalisation policies implemented since the mid-1980s have led to “one of the most extreme increases in income and wealth inequality observed in the world”.

- The female labour income share in India is equal to 18% which is significantly lower than the average in Asia (21%, excluding China) and this value is one of the lowest in the world.

- A person in the bottom 50% of the population in India is responsible for, on average, five times fewer emissions than the average person in the bottom 50% in the European Union and 10 times fewer than the average person in the bottom 50% in the US.

- There has been a rise of private wealth in emerging countries such as China and India. China has had the largest increase in private wealth in recent decades. The private wealth increase seen in India over this time is also remarkable (up from 290% in 1980 to 560% in 2020).

Apart from the moral obligations to review policies to tackle inequality – there is also a constitutional mandate to reduce inequality in the Directive Principles of State Policies.

Looking outside what the reports tell us

The Oxfam report does not exclusively examine the multiplying wealth of India’s billionaires – therefore we need to look outside this 0.00001% of our population and also focus on the analysis of basic social services (particularly those that affect the survival of the poor).

- India must be one of the only countries in the world where during the COVID-19 pandemic the health Budget has declined — and that too by a huge 10% in 2020-21.

- Social security expenditure has declined from an already pathetically low 1.5% in 2020-21 to 0.6% of the Union Budget in 2022.

- Social security pensions, for the elderly, for the disabled, and widows have been frozen at ₹200-₹300 a month for almost 15 years (this means there is not enough money allocated by the government to even index these to inflation).

- The priority list of households under the NFSA has been frozen in absolute numbers, based on a percentage determined from the 2011 Census.This means in the last 11 years, approximately 10 crore eligible beneficiaries, according to the increasing population numbers, have been kept out. Therefore, approximately 12% legally entitled people — even children of existing “priority households” — cannot get subsidised foodgrain.

- While the pandemic has produced a generation of children who have forgotten what formal education is and many teenagers from poor households have already joined the workforce – there has been a 6% cut in the education Budget.

Other Challenges that exacerbate the economic inequality problem in India

- Poverty in relation with population numbers: Despite lifting 271 million people out of poverty between 2005-15, India still remains home to 28 per cent of the world’s poor, as per the Human Development Report. Though severe poverty is less, vulnerability towards poverty is quite high.

- Smaller Incomes: While it can be claimed that unemployment is under control in India to some extent, smaller incomes have resulted in a higher dominance of working poor, lower share of skilled workforce and lack of old-age security.

- Education: In terms of Education, inequality in India is more than that in the South Asian region and the world. Indian girls attend school for a shorter period than the regional average.

Constitutional Provisions in DPSP to eliminate inequality

- Article 38 section (2) says ““The State in particular shall strive to MINIMISE ECONOMIC INEQUALITIES IN INCOME and eliminate inequalities in status, facilities and opportunities not amongst individuals but also amongst groups.”

- Article 39 says “The State shall in particular, direct its policies towards securing:

- that the citizens, men and women equally, have the right to an adequate means to livelihood;

- that the ownership and control of the material resources of the community are so distributed as best to subserve the common good;

- that the operation of the economic system DOES NOT RESULT IN THE CONCENTRATION OF WEALTH AND MEANS OF PRODUCTION to the common detriment;

- that there is equal pay for equal work for both men and women;

- that the health and strength of workers, men and women, and the tender age of children are not abused and that citizens are not forced by economic necessity to enter avocations unsuited to their age or strength;

- that children are given opportunities and facilities to develop in a healthy manner and in conditions of freedom and dignity and that childhood and youth are protected against exploitation and against moral and material abandonment

- Article 43 says “The State shall endeavour to SECURE TO ALL WORKERS A LIVING WAGE and a decent standard of life.”

Way forward

- India urgently needs a new strategy for growth, founded on new pillars, such as broader progress measures.

- Until the incomes of all rise, India will be a poor country from the perspective of the majority of its citizens, no matter how large its GDP, therefore, Indian economy must grow to create more incomes for its billion-plus citizens.

- Governments must adopt strong anti-inequality policies on public services, tax and labour rights, to significantly reduce the gap between rich and poor.

- Governments, international institutions and other stakeholders should work together to rapidly improve data on inequality and related policies, and to accurately and regularly monitor progress in reducing inequality.

-Source: The Hindu

Impending Global minimum tax rate implementation

Context:

The long-standing complaint about corporate houses abusing provisions for tax exemption and deductions was addressed in a unique way in India by the introduction of a twin system of tax rates for companies claiming deductions and not claiming deductions.

Domestic companies are charged 25% when their turnover is less than ₹250 crore and 30% when their turnover is above ₹250 crore and partnership firms are taxed at 30%.

The idea seems to be to encourage corporatisation of firms. But medium- and small-scale industries find it a pain to go through the legal processes of corporatisation. Promoters of companies devise novel ways to escape the rigour of taxation.

With such developments, the Government of India also has to prepare for the introduction of the global minimum tax on MNCs, as agreed to by 130 countries in July 2021.

Relevance:

GS-III: Indian Economy (Economic Growth and Development, Foreign Trade and related issues, Inclusive growth and issues therein), GS-II: International Relations

Dimensions of the Article:

- India’s Taxation system on corporations

- Impact of such reductions in direct taxation

- Base Erosion Profit Shifting (BEPS)

- About the Global Minimum Corporate Tax Rate proposal

- The necessity of the Global Minimum Corporate Tax according to U.S.

- India and the Global Minimum Tax rate

- Conclusion

India’s Taxation system on corporations

- The decline in corporate tax rates is against the progressive nature of the tax system as it reduces government revenue at a time of growing public deficit and declining public wealth.

- High-income individuals choose to incorporate their business so that they can shift income from personal income tax to corporate tax.

- There is also the recent phenomenon of wealthy families of promoters of big corporate houses creating a succession plan through private trusts – by transferring assets to the trusts. (This is done by wealthy families in the Western countries like the Waltons who run Walmart via private trusts).

Impact of such reductions in direct taxation

- One of the implications of the reductions in direct tax rates has been that governments have increasingly depended on the regressive indirect taxes for revenue generation.

- Value-Added Tax and Goods and Services Tax have been increasingly used to get more revenues. This impacts the less well-off proportionately more and is inflationary.

- Direct taxes tend to lower the post-tax income inequality. The rising inequalities result in shortage of demand in the economy and to its slowing down which then requires more investment and that calls for more concessions to capital. However, that does not guarantee revival because investment in response to a tax cut is uncertain. Instead, increased government expenditures are sure to raise demand.

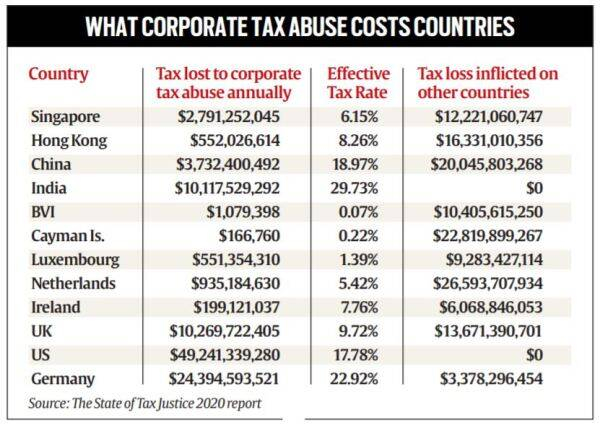

Base Erosion Profit Shifting (BEPS)

- The world experiences Base Erosion Profit Shifting (BEPS) when companies shift their profits to low tax jurisdictions, especially, the tax havens.

- For instance, many of the most profitable companies like Google and Facebook are accused of shifting their profits to Ireland and other tax havens and paying little tax.

- EU has levied fines on Google and Apple for such practices. Former U.S. President Barack Obama in 2009 had said that the U.S. was losing $100 billion in taxes due to such practices.

- Since all the OECD countries have suffered due to cuts in tax rates and BEPS, initiatives have been taken to check these practices. But they will not succeed unless there is agreement among all the countries.

- Any country facing economic adversity can cut its tax rates to attract capital and force others to follow suit.

- India has also cut its tax rates since the 1990s. Most recently in 2019 the corporation tax rate was cut drastically to match those prevailing in Southeast Asia. Such cuts have implications for both inequality as well as for funding the schemes for the poor and the quality of public services.

About the Global Minimum Corporate Tax Rate proposal

- The US proposal envisages a 21% minimum corporate tax rate, coupled with cancelling exemptions on income from countries that do not legislate a minimum tax to discourage the shifting of multinational operations and profits overseas.

- The US views a Global Minimum Corporate Tax Rate as an attempt to reverse a “30-year race to the bottom” in which countries have resorted to slashing corporate tax rates to attract multinational corporations (MNCs).

- The proposal for a minimum corporate tax is tailored to address the low effective rates of tax shelled out by some of the world’s biggest corporations, including digital giants such as Apple, Alphabet and Facebook, as well as major corporations such as Nike and Starbucks.

- These companies typically rely on complex webs of subsidiaries to hoover profits out of major markets into low-tax countries such as Ireland or Caribbean nations such as the British Virgin Islands or the Bahamas, or to central American nations such as Panama.

The necessity of the Global Minimum Corporate Tax according to U.S.

- The proposal aims to somewhat offset any disadvantages that might arise from the proposed increase in the US corporate tax rate.

- The proposed increase to 28% from 21% would partially reverse the previous cut in tax rates on companies from 35% to 21% by way of a 2017 tax legislation.

- The increase in corporation tax comes at a time when the pandemic is costing governments across the world, and is also timed with the US’s push for a USD 2.3 trillion infrastructure upgrade proposal.

- A global compact on this issue, at the time of pandemic, will work well for the US government and for most other countries in western Europe, even as some low-tax European jurisdictions such as the Netherlands, Ireland and Luxembourg and some in the Caribbean rely largely on tax rate arbitrage to attract MNCs.

- The plan to peg a minimum tax on overseas corporate income seeks to potentially make it difficult for corporations to shift earnings offshore.

- However, a global minimum rate would essentially take away a tool that countries use to push policies that suit them. A lower tax rate is a tool they can use to alternatively push economic activity.

India and the Global Minimum Tax rate

- The Government of India has to prepare for the introduction of the global minimum tax of 15% on MNCs, as agreed to by 130 countries in July 2021.

- This 15% is lower than what working class and middle-class people in high-income countries pay.

- The rate of global minimum tax at 15% on MNCs will mean a gain of $0.5 billion for India without deductions. The gain will be zero if deductions are allowed.

- The World Inequality Report suggested a minimum global tax on MNCs at 25% – and if this 25% is agreed upon, it would mean a gain of $1.4 billion for India without deductions and $1.2 billion with deductions of 5%.

Conclusion

- MNCs and their shareholders have been the main winners from globalisation. Their profits have boomed due to the ever-closer integration of world markets. Thus, it is only rational if they are taxed appropriately to promote equity. Inflation indexing has long been suggested as a way out to sort out the difficulties of the fixed income group and this option can be explored as well.

-Source: The Hindu