CONTENTS

- Plastic Solution

- An Inheritance Tax will Help Reduce Inequality

Plastic Solution

Context:

The latest round of negotiations for the Global Plastics Treaty, a sweeping endeavor involving over 175 United Nations member nations aimed at phasing out plastic usage, has recently concluded. The objective is to finalize a legal framework by the end of 2024, outlining timelines for countries to agree on measures to reduce plastic production, eliminate wasteful uses, prohibit certain harmful chemicals in production, and establish recycling goals. However, reaching an agreement remains elusive, with another round of talks scheduled for November in Busan, South Korea.

Relevance:

GS3- Environment- Pollution

Mains Question:

Plastic pollution cannot stop by treaties, without investment in alternatives. Analyse in the context of the latest round of negotiations for the Global Plastics Treaty. (15 Marks, 250 Words).

More on the Global Plastics Treaty:

- The fourth session of the Intergovernmental Negotiating Committee (INC-4) of the United Nations Environment Assembly (UNEA) recently took place in Ottawa, Canada, with the participation of over 170 member states.

- This session forms part of the ongoing negotiations aimed at establishing a legally binding treaty on plastic pollution by the conclusion of 2024 under UNEA.

- However, INC-4 failed to reach an agreement on the global plastics treaty. Negotiators are now targeting a consensus by the end of 2024 at INC-5, which is scheduled for November 2024 in South Korea.

- The Intergovernmental Negotiating Committee (INC) was established by the United Nations Environment Programme (UNEP) in March 2022 to develop an international legally binding agreement on plastic pollution.

- Its mandate includes addressing the entire life cycle of plastic, encompassing its presence in the marine environment, and exploring both voluntary and binding approaches.

- The series of negotiations began with INC-1 in November 2022 in Punta del Este, Uruguay, followed by INC-2 in May-June 2023 in Paris, France, and INC-3 in Nairobi in December 2023.

Primary Obstacles:

- The primary obstacles lie in economic concerns, particularly from oil-producing and refining nations like Saudi Arabia, the United States, Russia, India, and Iran, which are hesitant to commit to firm deadlines for ending plastic production.

- On the other hand, a coalition of African countries, supported by several European nations, advocates for setting a deadline around 2040 to ensure a phased reduction plan is put into action.

- Disagreements also persist regarding whether contentious issues within the treaty should be resolved through voting or consensus, the latter implying that each country holds veto power.

- India, among others, expresses discomfort with binding targets and insists that any legally binding agreement to combat plastic pollution should address various factors, including the availability, accessibility, and affordability of alternatives, along with considerations for capacity building, technical assistance, technology transfer, and financial support.

- This stance echoes the principle of ‘common but differentiated responsibility’ seen in climate negotiations, where countries share a collective goal but more privileged nations are expected to support others and undertake stricter commitments themselves.

- Common But Differentiated Responsibilities (CBDR) is a principle embedded within the United Nations Framework Convention on Climate Change (UNFCCC), acknowledging the varying capabilities and obligations of individual nations in combating climate change.

- Originating from the Earth Summit of 1992 in Rio de Janeiro, Brazil, CBDR recognizes two key aspects of responsibility: first, the shared responsibility of all states to address environmental concerns and promote sustainable development, and second, the differentiated responsibility that allows states to address environmental issues based on their national capacity and priorities.

Plastic Treaty and India:

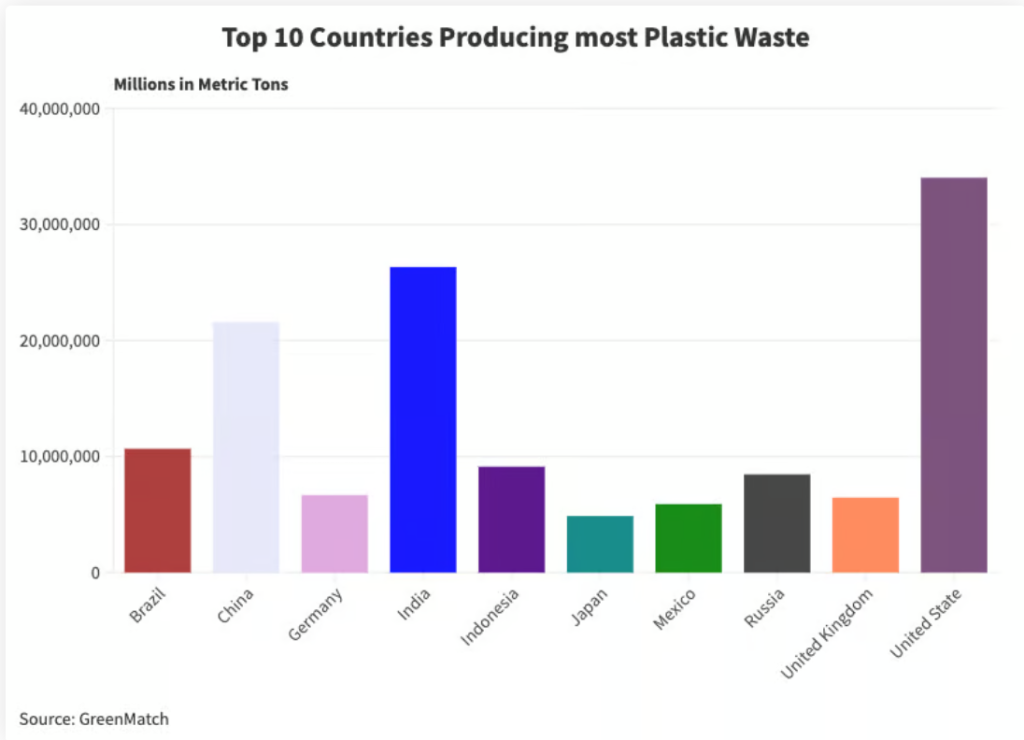

- The global distribution of plastic pollution is uneven, with Brazil, China, India, and the U.S. collectively responsible for 60% of plastic waste, according to a report by the non-profit EA Earth Action.

- In 2022, when the idea of the plastics treaty emerged, India implemented the Plastic Waste Management Amendment Rules (2021), which prohibited 19 categories of “single-use” plastics.

- The Plastic Waste Management Amendment Rules of 2021 outline several measures to address plastic pollution:

- By 2022, certain single-use plastic items deemed to have low utility and high littering potential will be prohibited.

- Starting from July 1st, 2022, the manufacture, import, stocking, distribution, sale, and use of specific single-use plastic items, including polystyrene and expanded polystyrene, will be banned.

- Plastic packaging waste not covered by the single-use plastic item phase-out will be collected and managed in an environmentally sustainable manner through Extended Producer Responsibility (EPR), as mandated by the Plastic Waste Management Amendment Rules of 2021.

- These rules legally enforce the responsibility of producers through EPR.

- There will be an increase in the thickness of plastic carry bags from 50 microns to 75 microns, effective from September 30th, 2021, and further to 120 microns by December 31st, 2022.

- However, notable exclusions from the ban include plastic bottles, even those under 200 ml, and multi-layered packaging such as milk cartons.

- Additionally, the enforcement of the ban on single-use plastic items varies across the country, with many outlets continuing to sell these products.

Conclusion:

Similar to the challenges encountered in transitioning away from fossil fuels, addressing plastic pollution cannot rely solely on treaty agreements. There must be significant investment in alternative products and efforts to make them affordable before setting realistic targets for reduction.

An Inheritance Tax will Help Reduce Inequality

Context:

A statement by the Chairman of the Indian Overseas Congress advocating for the implementation of an inheritance tax to redistribute wealth, has ignited extensive debates. This article presents arguments for addressing high inequality and supports the use of progressive taxes as a means to alleviate it.

Relevance:

GS3- Inclusive Growth

Mains Question:

With reference to rising inequality in India, discuss whether levying inheritance tax could offer feasible solutions. (10 Marks, 150 Words).

Disproportionate Power:

- In an unequal society, a small group of influential individuals may wield disproportionate power by controlling resources.

- This concentration of power can result in a few wealthy elites shaping socioeconomic and political decisions to benefit themselves at the expense of the majority. The recent electoral bonds scandal serves as evidence of this phenomenon.

- In such a scenario, the citizenship of the wealthy elites carries more weight than that of the majority of the population, posing ethical concerns.

Importance of Addressing Inequality:

The importance of addressing inequality stems from several key factors.

- Firstly, inequality undermines economic growth over the medium to long term by hindering firm productivity, reducing labor income, and diverting resources away from essential rights such as education.

- Secondly, in unequal societies, an individual’s place of birth disproportionately influences their lifetime outcomes. In India, nearly one-third of the variation in consumption can be attributed to the individual’s place of residence, whether it be the state, city, or village.

- Thirdly, high levels of inequality are linked to political polarization and increased conflict.

- Fourthly, inequality tends to have a negative multiplier effect on the economy, as diminished earnings for the poor result in reduced consumption and savings, increased indebtedness, and subsequently lower aggregate demand, production, and investment, leading to diminished growth rates in the future.

Concerning Trends in India:

Examining data from various sources, including the Labor Bureau and the Reserve Bank of India, researchers like Jean Drèze, Reetika Khera, Zico Dasgupta, and Srinivas Raghavendra have highlighted concerning trends.

- For instance, while real wages of agricultural laborers showed growth between 2004 and 2014, they declined in the last decade.

- Moreover, a significant proportion of households earn less than the recommended daily minimum wage, and there’s been a notable reduction in household savings accompanied by increased debt.

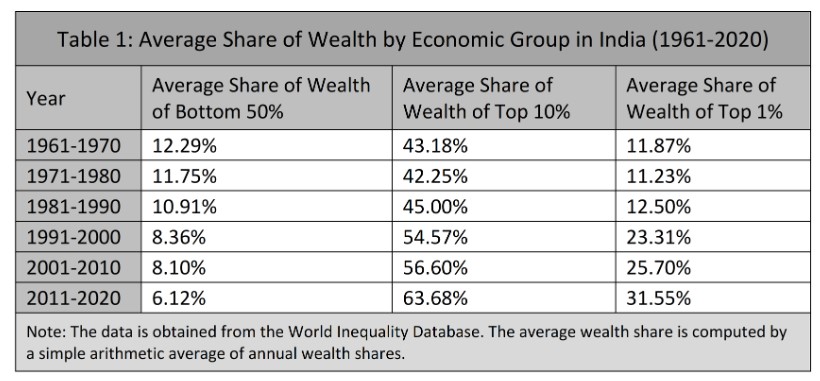

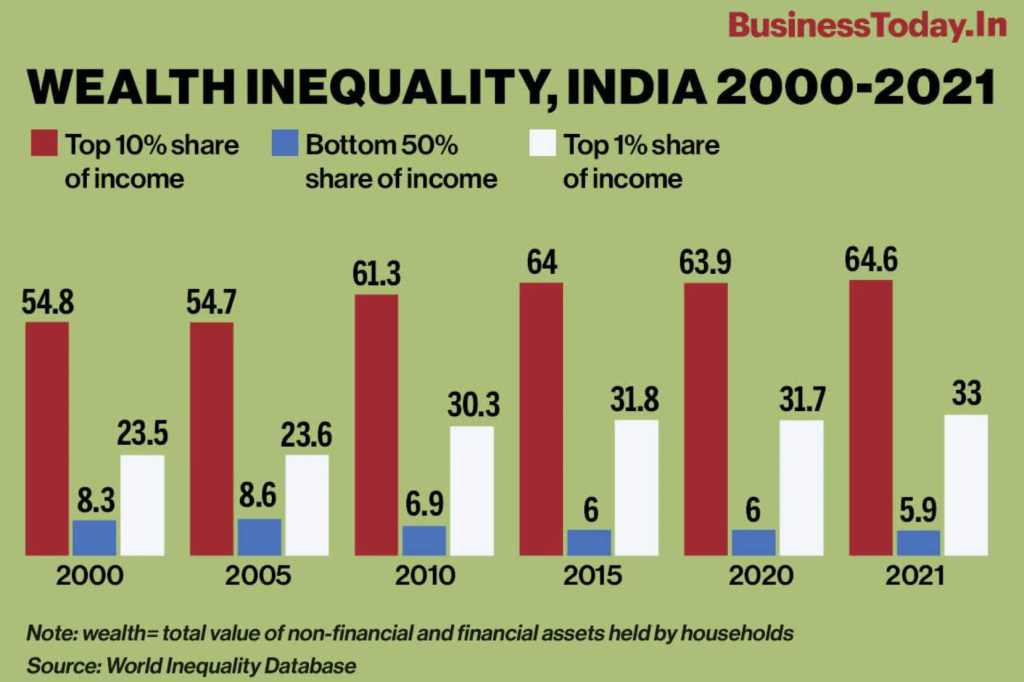

- In stark contrast, the wealthiest 1% of the population holds a staggering 40% of India’s wealth.

- Some analysts argue that a certain degree of inequality is unavoidable during periods of economic growth, suggesting that efforts should focus on poverty reduction instead.

- However, research conducted by Tianyu Fan and colleagues indicates that the benefits of India’s economic growth over the past two decades have disproportionately favored affluent urban residents.

- Underlying this argument is the notion that there’s nothing inherently superior about the children of wealthy families compared to those from less affluent backgrounds.

- The Constitution mandates equality of status and opportunity, thus placing an obligation on the government to address disparities stemming from factors beyond an individual’s control, such as their birth circumstances.

Inheritance Tax as a Proposed Solution:

- One proposed solution to tackle wealth inequality is through the implementation of an inheritance tax.

- Unlike a wealth tax, which is an ongoing tax on an individual’s assets, an inheritance tax is levied once during an individual’s lifetime and is intergenerational.

- Typically targeted at individuals with substantial wealth exceeding a certain threshold, these taxes, when effectively implemented, serve to reduce wealth concentration and incentivize the allocation of resources towards productive endeavors.

- Moreover, the transfer of property from affluent individuals to their descendants often occurs without the latter having contributed any labor to acquire it, further justifying the imposition of such taxes.

- There is no economic rationale for exempting individuals from inheritance tax. Some may argue that implementing such a tax would discourage innovation.

- However, this overlooks the fact that innovation is crucial for maintaining competitiveness in modern economies and suggests that innovation serves only to perpetuate dynastic control of resources, which contradicts democratic principles.

- On the contrary, revenue generated from inheritance tax could be utilized to finance a diverse range of innovative endeavors.

- Japan, an advanced nation, imposes an inheritance tax of up to 55%. In India, a form of inheritance tax known as the estates duty was in effect between 1953 and 1985 but was abolished due to administrative complexities.

- Economist Rishabh Kumar demonstrates that this tax was effective in reducing the top 1% personal wealth share from 16% to 6% between 1966 and 1985.

Conclusion:

Various economists illustrate that implementing a 2% wealth tax and a 33.3% inheritance tax solely on the top 1% of earners in India could generate additional public expenditure equivalent to 10% of the GDP. This additional revenue could then be allocated towards securing various socioeconomic rights for the impoverished, such as ensuring living wages, access to healthcare, employment opportunities, and food security.