CONTENTS

- Ties that Epitomise India’s Neighbourhood First Policy

- Simplifying and Rationalising the Goods and Services Tax

Ties that Epitomise India’s Neighbourhood First Policy

Context:

Throughout history, people have marveled at the close relationship between Bhutan, a nation spanning 38,394 square kilometers with a population of 770,000, and its much larger neighbor, India, covering 3.28 million square kilometers with a population of 1.4 billion. The explanation for this enduring friendship is rather straightforward. Both countries view each other as equals, treating one another with the utmost respect.

Relevance:

GS2-

- India and its Neighbourhood

- Effect of Policies and Politics of Countries on India’s Interests

- Groupings and Agreements Involving India and/or Affecting India’s Interests

Mains Question:

There is much evidence of the unique level of trust between the leadership of Bhutan and India that has led to a strengthening of relations. Discuss in the context of recent visits by the leaders of both nations. (15 Marks, 250 Words).

More on India-Bhutan Ties:

- They have come to understand that size alone does not determine the strength of relations between two independent nations.

- Consequently, India has consistently honored Bhutanese identity, respected its distinct religious practices, and supported its economic aspirations while preserving its unique way of life.

- In return, Bhutan has recognized that its sovereignty and identity are not threatened from its southern border and has looked to India for support in its growth and development.

- India has met these expectations, fostering a deep level of trust between the leadership of both nations over the decades, a trust that has been evident in recent times.

The Gelephu Initiative:

- The Gelephu initiative, mentioned during the King of Bhutan’s visit to India in November 2023, hints at plans for establishing a Mindfulness City in southern Bhutan. This city is envisioned as a Special Economic Zone aimed at attracting foreign investment to bolster the prosperity of Bhutan. Naturally, India, along with its business community, is anticipated to play a significant role in this endeavor.

- Moreover, the Gelephu Mindfulness City is designed with a focus on sustainability, well-being, and environmental considerations. It is anticipated that such a project will not only elevate Bhutanese income levels but also address concerns regarding its impact on Bhutan’s status as a carbon-negative country.

- Gelephu city is also expected to prioritize human well-being, with features such as yoga, leisure activities, spa treatments, and mental relaxation programs.

- The recent visit of the Prime Minister of Bhutan to India serves as a follow-up to the King’s earlier visit, featuring constructive discussions with Prime Minister Narendra Modi and President Droupadi Murmu.

- Furthermore, Prime Minister Modi’s forthcoming visit to Bhutan underscores the importance of nurturing relationships, whether between individuals or nations, through ongoing dialogue and cooperation.

Other Recent Developments:

- The consecutive visits of the Prime Ministers of Bhutan and India underscore the commitment of both governments to fostering a strong relationship. This bodes well for the continued growth and development of ties between the two countries and reflects India’s Neighbourhood First policy approach.

- In the Interim Budget for the fiscal year 2024-25, the Ministry of External Affairs (MEA) has been allocated a sum of Rs 22,154 crore. Demonstrating India’s commitment to its ‘Neighbourhood First’ policy, the largest portion of aid has been designated for Bhutan, amounting to Rs 2,068 crore compared to Rs 2,400 crore in the previous fiscal year.

- Both nations have inked an agreement ensuring a consistent and dependable supply of petroleum products from India to Bhutan. This move aims to bolster economic cooperation and growth in the hydrocarbon sector.

- Bhutan’s Food and Drug Authority and India’s Food Safety and Standards Authority (FSSAI) have signed an agreement to enhance cooperation in ensuring food safety. This collaboration will facilitate trade by ensuring adherence to food safety standards, thereby reducing compliance costs.

- An MoU on energy efficiency and conservation has been signed, underscoring both countries’ commitment to sustainable development.

- India will support Bhutan in improving energy efficiency in households, promoting the use of energy-efficient appliances, and developing standards and labeling schemes.

- The visit of the Bhutanese Prime Minister coincides with ongoing discussions between Bhutan and China to resolve their border dispute, particularly in the Doklam region, with implications for regional security.

- In August 2023, both countries agreed on a plan to address the disagreement, culminating in the formal signing of the agreement in October 2021. This agreement follows a conflict between India and China in Doklam in 2017, sparked by China’s attempt to construct a road in the area.

- Hydropower collaboration stands as the cornerstone of India’s relationship with Bhutan. Over the years, numerous joint hydroelectric projects have been successfully completed and inaugurated by the respective governments, supplying clean energy to India while generating substantial revenue for Thimphu. This revenue influx has propelled Bhutan out of the Least Developed Country status.

- Despite delays, the Punatsangchhu-II hydropower project is poised for completion in 2024, serving as another testament to the efficacy of government-to-government cooperation in the hydroelectric sector.

- In recent times, a novel joint venture model was introduced for hydroelectric project construction between India and Bhutan. However, none of the proposed five projects has gained significant traction.

- This suggests a need to recognize the flaws in this new model and return to the drawing board to devise a more practical and potentially successful approach for future hydroelectric ventures.

- India has also played a crucial role as a major development partner to Bhutan, contributing ₹5,000 crore to its recently concluded 12th Five Year Plan.

- A key aspect of this development assistance is India’s emphasis on aligning projects with the priorities of the Bhutanese people, ensuring that initiatives directly benefit them.

- This collaborative and consultative approach is fundamental to the successful partnership for prosperity between New Delhi and Thimphu, and it is imperative that this model persists in the future.

Way Forward:

- In the forthcoming years, India can play a pivotal role in ensuring the success of the Gelephu Mindfulness City by considering the following measures:

- Initiate direct flights between Mumbai/Delhi and Gelephu to facilitate easier access.

- Offer technological expertise and knowledge in constructing essential infrastructure to Bhutan, with the private sector taking a leading role in implementation.

- Promote Gelephu as a destination for high-end Indian tourists and business professionals, while maintaining controlled visitor numbers.

- Encourage Indian enterprises to establish operations within the city, fostering economic growth and collaboration.

Conclusion:

Given Gelephu’s proximity to remote regions of West Bengal and Assam, the prosperity of the Mindfulness City is anticipated to have positive socio-economic effects in these areas as well. This collaborative endeavor between India and Bhutan will serve as yet another example of mutually beneficial cooperation.

Simplifying and Rationalising the Goods and Services Tax

Context:

A Committee of Ministers (CoM) appointed by the GST (Goods and Services Tax) Council is presently reassessing the new tax framework, with a primary focus on achieving ‘simplification’ and ‘rationalization’ as core objectives. GST, a unified nationwide tax system, amalgamates more than a dozen taxes from the pre-GST era. Implemented across India, it incorporates a provision for offsetting tax paid on inputs, commonly referred to as input tax credit (ITC).

Relevance:

GS3- Indian Economy

Mains Question:

A Group of Ministers (GoM) set up by the GST (Goods and Services Tax) Council is currently reviewing the GST tax regime with a focus on ‘simplification’ and ‘rationalisation’ as key objectives. In this context, discuss the factors that govern GST collections and the rationale behind the constitution of this GoM. (15 Marks, 250 Words).

More about GST:

- GST aims at eliminating the cascading effect of tax on tax and incentivizes businesses to accurately report all their purchase and sales transactions.

- The Gross GST (GGST) collection comprises various components: Central GST (CGST), imposed by the central government on intrastate transactions within a single state; State GST (SGST), a tax levied by individual state governments on intrastate supplies of goods and services consumed within their respective territories; Integrated GST (IGST) collection, a tax applied to all interstate transactions involving goods and/or services across two or more states/Union Territories (UTs), including collections from the import of goods.

- Additionally, GGST encompasses Compensation Cess (CC), imposed on specific goods and/or services to compensate states for revenue losses incurred due to the GST regime’s implementation. Initially intended for a five-year period until July 1, 2022, it has been extended until March 2026.

- The extension aims to utilize proceeds to repay loans acquired during 2020-21 and 2021-22 to cover shortfalls in cess collections compared to states’ compensation requirements during those years.

Relevant Statistics:

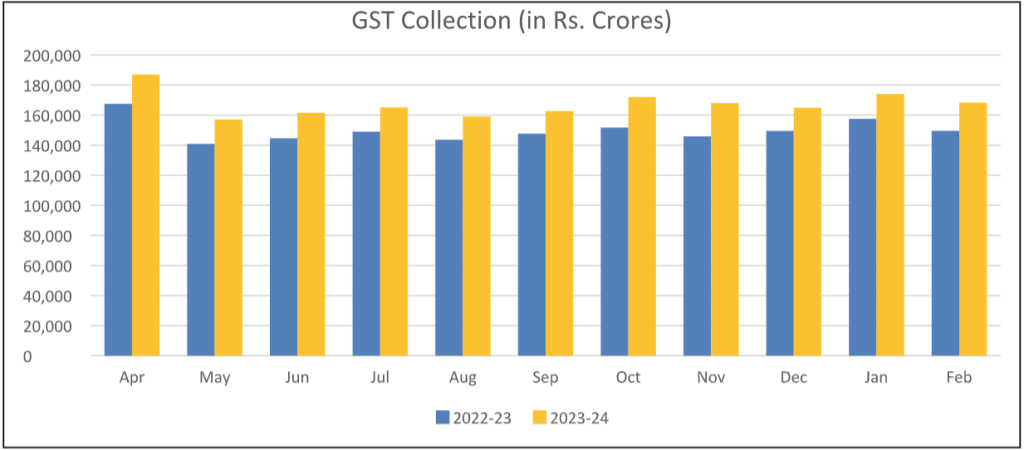

- GGST collections during 2018-19 and 2019-20 typically remained below Rs 100,000 crore per month. Amid the COVID-19 pandemic, collections in the first half of 2020-21 experienced a decline, but rebounded to Rs 100,000 crore during the second half.

- Subsequently, in 2021-22, collections increased, averaging Rs 124,000 crore per month. Further growth was observed in 2022-23, with the monthly average rising to Rs 150,000 crore.

- During the current fiscal year, the monthly average Gross GST (GGST) collections have surged to Rs 166,000 crore between April and November 2023, marking a year-on-year growth of 12 percent. Breaking down the figures, Central GST (CGST) and State GST (SGST) collections have risen by 16.7 percent and 15.4 percent respectively.

- Compensation Cess (CC) collections have also increased by 12.9 percent. However, Integrated GST (IGST) collections have shown a more modest growth of only 8.6 percent.

- This is attributed to a meager growth of 2.6 percent in IGST collections from the import of goods, primarily caused by an 8.7 percent decline in merchandise imports during this period.

Factors Influencing GST Collections:

- Tax collections are primarily influenced by three factors: tax rates, nominal GDP (NGDP), which represents GDP at current prices, and compliance.

- According to a study conducted by the Reserve Bank of India (RBI) in 2022, the weighted average GST rate decreased from 14.4 percent at the time of GST implementation to 11.6 percent in 2019, owing to a series of tax reductions during this period.

- The initial rate of 14.4 percent itself was lower than the revenue neutral rate (RNR) estimated by the Arvind Subramanian Committee, which ranged from 15 to 15.5 percent. RNR is the tax rate intended to generate similar revenue under the new regime as collected from taxes under the previous regime.

- Despite the reduction in GST rates, the increase in GST collections indicates that the other two factors played a significant role. The substantial rise in Nominal Gross Domestic Product (NGDP) by 18.4 percent in 2021-22 and 16.1 percent in 2022-23 contributed to remarkable growth in GGST collections during those periods.

- Although the growth in NGDP slowed to around 9 percent from April to November 2023, the 12 percent increase in GGST collections during this period is attributed to enhanced compliance and evasion prevention efforts.

- Prior to the GST regime, it was feasible to move goods from factories to sales points and sell them to consumers without issuing an invoice, thus avoiding tax payment. This issue was exacerbated by the prevalence of cash transactions, leaving no audit trail.

Initiatives Under GST:

- Under GST, every transaction of a firm is monitored at every stage. Upon the departure of goods from its premises, the firm must generate an electronic invoice (e-invoice), authenticated electronically by the GST Network (GSTN).

- Additionally, the firm is required to produce an electronic Waybill (e-Way bill) through the eWay Bill Portal for any consignment of goods valued above Rs 50,000. This document must be carried by the person responsible for the conveyance transporting the goods.

- The government is also enhancing the GST infrastructure through various measures, including the implementation of AI and ML-based analytics to aid in data evaluation, Aadhaar authentication for registration, and targeted actions against non-filers.

- These initiatives aim to encourage all businesses to participate in the GST network, accurately report all transactions, and prevent fraudulent claims for Input Tax Credit (ITC).

- As a consequence, between April 2018 and April 2023, there was a notable 56 percent increase in the total number of GST return filings, reaching 11.28 million, while the count of active GST taxpayers surged by 33 percent to 13.96 million.

- Regarding evasion detection, apart from approximately Rs 100,000 crore uncovered during 2022-23, the government anticipates detecting evasion amounting to Rs 300,000 crore for the current fiscal year. It aims to recover approximately Rs 50,000 crore within the current year itself.

Way Forward:

- Firstly, the council should contemplate bringing petroleum products under the ambit of GST. Presently, these products are taxed under the pre-GST regime, incurring a considerably higher levy. For example, in Delhi, taxes (comprising central excise duty or CED plus VAT) make up about 80 percent of the ex-refinery price of petrol.

- Shifting to GST taxation would reduce this to 28 percent (even if placed in the highest slab), implying that the Centre and states would still collect over one-third of their current revenue. A robust GST regime should be capable of compensating for this loss.

- Secondly, the council should transition from the current five-tier tax structure (nil, 5 percent, 12 percent, 18 percent, and 28 percent) to a simpler tax framework, as originally envisaged for GST.

- While the Dr. Kelkar committee proposed a single GST rate of 12 percent, Arvind Subramanian recommended a three-rate regime. For the interim, the GST Council may consider adopting Dr. Subramanian’s approach.

- Thirdly, numerous sectors encounter an ‘inverted duty’ structure, wherein the tax on finished products is lower than that on the raw materials (RMs) used in their production. For instance, the GST on complex fertilizers is 5 percent, compared to 18 percent on ammonia and 12 percent on phosphoric acid.

- This leads to an output tax liability insufficient to offset Input Tax Credit (ITC), resulting in ‘unabsorbed’ tax credit. Rectifying this anomaly entails reducing the tax on raw materials to at least the level of tax on finished products.

Conclusion:

The upward trajectory in GST collections since FY 2021-22 instils confidence that the new regime is resilient and sustainable, capable of generating substantial revenue consistently. Leveraging this strength, the GST Council should address the pending issues discussed above.