The Current Predicament

- The priority for India is to ensure that it overcomes the COVID-19 pandemic and kick-starts GDP growth rather than fix the weaknesses in the macroeconomy: a high fiscal deficit of 7.49% and government indebtedness that was 69% of GDP in 2019.

- The Government’s financing strategy should be to raise long-term funds at cost effective rates, with flexible repayment terms that allow it to take tactical advantage of market movements.

What can be done with GDP-linked bonds?

- The GoI may issue listed, Indian rupee denominated, 25-year GDP-linked bonds that are callable from, say, the fifth year.

- The coupon (interest) on a GDP-linked bond is correlated to the GDP growth rate and is subject to a cap.

- The issuer, the GoI, is liable to pay a lower coupon during years of slower growth and vice-versa.

- The callable feature from the fifth year till maturity allows the GoI to effect partial repayments during high growth years and when it earns non-recurring revenues such as proceeds from disinvestment of public sector enterprises (PSEs).

- The listing of bonds provides investors an exit option.

Is this really possible?

- Costa Rica, Bulgaria and Bosnia-Herzegovina issued the first pure GDP-linked bonds in the 1990s.

- Argentina and Greece issued warrant-like instruments similar to GDP-linked bonds in 2005 and 2012 respectively.

- India could learn from their experience.

- Publishing reliable and timely GDP data is a prerequisite for the successful issue of GDP-linked bonds, which the GoI may use to part-finance the COVID-19 rescue package and to diversify its borrowing sources.

Streamlining PSEs

- The 15 largest non-financial central PSEs (CPSEs) in the S&P BSE CPSE index contributed approximately 75% of the GoI’s ₹48,256.41 crore dividend income from PSEs in FY2020.

- The Union Budget projected PSE dividends to increase by 36.25% to ₹65,746.96 crore in FY2021.

- This milestone is unlikely to be achieved in the current environment.

Significance of PSEs

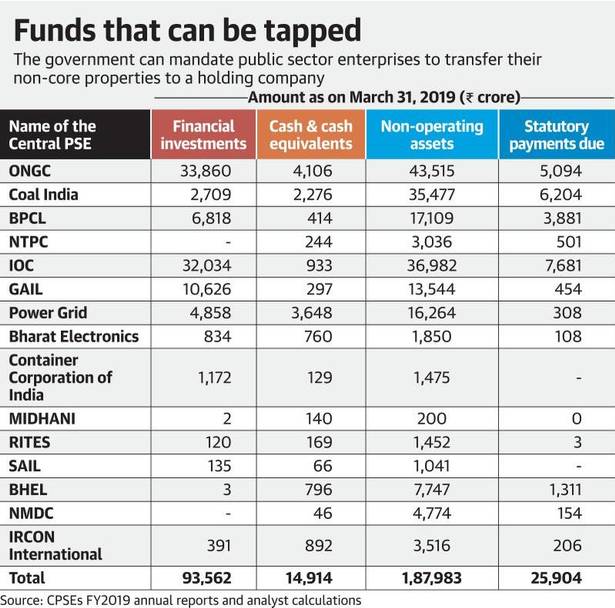

- The 15 CPSEs have accumulated sizeable non-core assets including financial investments, loans, cash and bank deposits in excess of their operating requirements, and real estate.

- The return on these assets (excluding real estate) is around 200 basis points lower than the returns on their core businesses.

- These CPSEs owe the government ₹25,904 crore as of end-March 2019. These non-core assets must be monetised to repay statutory dues and upstream dividends to GoI.

- It is imperative for the GoI to form a PSE and public sector bank holding company (‘Holdco’) to enable PSEs to monetise their non-core assets at remunerative prices, maximise their enterprise value and focus on their core businesses.

- It is essential that businesses maintain liquidity, especially during a downturn. However, the outstanding cash and bank deposits of the 15 CPSEs (₹64,253 crore) is in excess of their operating requirements.

- CPSEs must determine the cash they require to meet, say, six months of operating expenses and use the excess cash to repay statutory dues and upstream dividends to the GoI.

- Banks must extend to CPSEs committed lines of credit that the latter may draw down during exigencies.

- The 15 CPSEs have accumulated ₹93,562 crore financial investments comprising listed and unlisted debt, equity and mutual fund units. These exclude investments in associates and joint ventures.

- The CPSEs ought to transfer these investments to Holdco, which can manage the portfolio and transfer the returns to the original investors.

- The GoI must mandate all PSEs and government departments to transfer their non-core properties to Holdco, which can opportunistically sell these properties and transfer the proceeds to the owners.

RBI dividends

- The Reserve Bank of India (RBI) has allocated ₹1 lakh crore to carry out long-term repo operations in tranches and has reduced the repo rates by 75 basis points to 4.4% to help banks augment their liquidity in the wake of the pandemic.

- Recognising the RBI’s liquidity requirements, the GoI must refrain from asking the RBI to pay more dividends that it can viably pay.

- During the five years ending on June 30, 2019, the RBI paid the GoI 100% of its net disposable income, with its FY2019 dividends more than trebling to ₹1.76 lakh crore from ₹50,000 crore in FY2018.

- The Bimal Jalan panel constituted in 2019 to review the RBI’s economic capital framework opined that the RBI may pay interim dividends only under exceptional circumstances and that unrealised gains in the valuation of RBI’s assets ought to be used as risk buffers against market risks and may not be paid as dividends.