Context:

United States Secretary of the Treasury’s proposal for global coordination of corporate taxation has huge implications – If the major world economies agree and the U.S. Congress approves the increased tax rates, it would constitute a reversal of the trend in tax policies since the collapse of the Soviet Bloc 30 years back.

Relevance:

GS-III: Indian Economy (Economic Growth and Development, Foreign Trade and related issues, Inclusive growth and issues therein), GS-II: International Relations

Mains Questions:

What is the necessity of a Global Minimum Corporate Tax Rate? Discuss in the light of trends in Corporate tax rates across the globe. (10 marks)

Dimensions of the Article:

- Trend in Corporate Tax rates globally

- Base Erosion Profit Shifting (BEPS)

- The regressive tax structure

- About the Global Minimum Corporate Tax Rate proposal

- The necessity of the Global Minimum Corporate Tax according to U.S.

Trend in Corporate Tax rates globally

- When the Soviet Bloc collapsed in 1990, nations in east Europe were badly hit and needed capital infusion to overcome their economic woes. To attract global capital, they cut their tax rates sharply. This resulted in a ‘race to the bottom’. Nations in Europe were forced to cut their tax rates one after the other to not only attract capital but also to prevent capital from leaving their shores. This had global implications.

- Nations became short of resources and cut back expenditures on public services and encouraged privatisation. Governments lacked resources for education, health and civic amenities. The developing countries followed suit even though private markets do not cater to the poor. Thus, disparities increased within nations.

- Presently, governments need resources to help people through transfer of incomes, provision of more public services and also prevent business failures. But their resources have been adversely impacted by the economic downturn. Consequently, fiscal deficits have reached record high levels. In the pre-pandemic era, such levels of deficit would have led to the tanking of the stock markets but now they are booming in anticipation of demand being pumped in by these high deficits. The result is a massive increase in inequality between those who have gained in the stock markets and those who have lost employment and incomes.

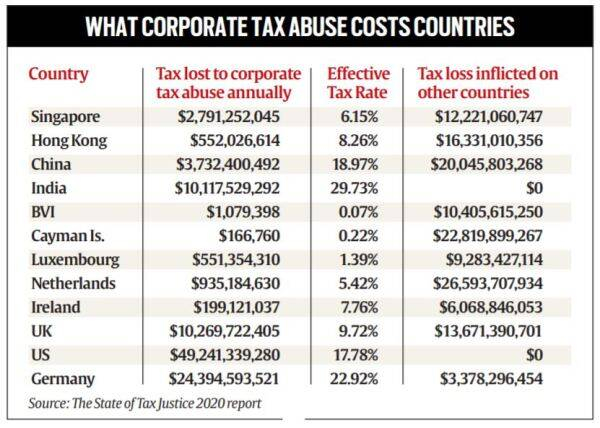

Base Erosion Profit Shifting (BEPS)

- The world experienced Base Erosion Profit Shifting (BEPS). Namely, companies shifted their profits to low tax jurisdictions, especially, the tax havens. For instance, many of the most profitable companies like Google and Facebook are accused of shifting their profits to Ireland and other tax havens and paying little tax.

- EU has levied fines on Google and Apple for such practices. Former U.S. President Barack Obama in 2009 had said that the U.S. was losing $100 billion in taxes due to such practices.

- Since all the OECD countries have suffered due to cuts in tax rates and BEPS, initiatives have been taken to check these practices. But they will not succeed unless there is agreement among all the countries.

- Any country facing economic adversity can cut its tax rates to attract capital and force others to follow suit.

- India has also cut its tax rates since the 1990s. Most recently in 2019 the corporation tax rate was cut drastically to match those prevailing in Southeast Asia. Such cuts have implications for both inequality as well as for funding the schemes for the poor and the quality of public services.

The regressive tax structure

- Another implication of the reductions in direct tax rates has been that governments have increasingly depended on the regressive indirect taxes for revenue generation.

- Value-Added Tax and Goods and Services Tax have been increasingly used to get more revenues. This impacts the less well-off proportionately more and is inflationary.

- Direct taxes tend to lower the post-tax income inequality. The rising inequalities result in shortage of demand in the economy and to its slowing down which then requires more investment and that calls for more concessions to capital.

- However, that does not guarantee revival because investment in response to a tax cut is uncertain. Instead, increased government expenditures are sure to raise demand.

About the Global Minimum Corporate Tax Rate proposal

- The US proposal envisages a 21% minimum corporate tax rate, coupled with cancelling exemptions on income from countries that do not legislate a minimum tax to discourage the shifting of multinational operations and profits overseas.

- The US views a Global Minimum Corporate Tax Rate as an attempt to reverse a “30-year race to the bottom” in which countries have resorted to slashing corporate tax rates to attract multinational corporations (MNCs).

- The proposal for a minimum corporate tax is tailored to address the low effective rates of tax shelled out by some of the world’s biggest corporations, including digital giants such as Apple, Alphabet and Facebook, as well as major corporations such as Nike and Starbucks.

- These companies typically rely on complex webs of subsidiaries to hoover profits out of major markets into low-tax countries such as Ireland or Caribbean nations such as the British Virgin Islands or the Bahamas, or to central American nations such as Panama.

The necessity of the Global Minimum Corporate Tax according to U.S.

- The proposal aims to somewhat offset any disadvantages that might arise from the proposed increase in the US corporate tax rate.

- The proposed increase to 28% from 21% would partially reverse the previous cut in tax rates on companies from 35% to 21% by way of a 2017 tax legislation.

- The increase in corporation tax comes at a time when the pandemic is costing governments across the world, and is also timed with the US’s push for a USD 2.3 trillion infrastructure upgrade proposal.

- A global compact on this issue, at the time of pandemic, will work well for the US government and for most other countries in western Europe, even as some low-tax European jurisdictions such as the Netherlands, Ireland and Luxembourg and some in the Caribbean rely largely on tax rate arbitrage to attract MNCs.

- The plan to peg a minimum tax on overseas corporate income seeks to potentially make it difficult for corporations to shift earnings offshore.

- However, a global minimum rate would essentially take away a tool that countries use to push policies that suit them. A lower tax rate is a tool they can use to alternatively push economic activity.

-Source: The Hindu