Context:

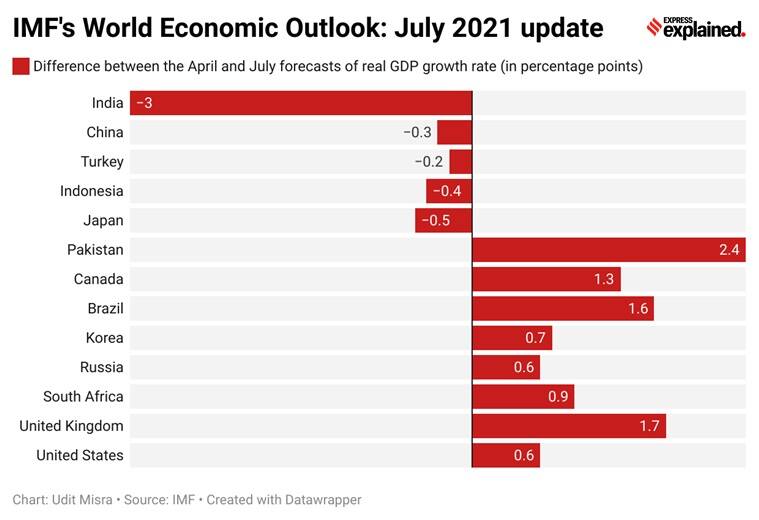

The latest update on the global economy by the International Monetary Fund (IMF) cut India’s GDP growth forecast for 2021-22 (or FY22) by as much as three percentage points.

This is set to affect the upcoming monetary policy review by the Monetary Policy Committee of the Reserve Bank of India.

Relevance:

GS-III: Indian Economy (Growth and Development of Indian Economy, Monetary)

Dimensions of the Article:

- Significant Points that will affect the August MPC review

- Impact of the second Covid-19 wave on Monetary Policy

Significant Points that will affect the August MPC review

- The RBI is legally mandated to keep the inflation rate between 2% and 6% but there is no such requirement when it comes to GDP growth.

- So, it can be said that the thumb rule for RBI is that – if inflation is within the desired range, it tries to do whatever it can to boost economic growth.

- Typically, boosting economic growth translates to reducing the interest rate that RBI charges to lend money to India’s commercial banks; this rate is called the repo rate. By doing so, it tries to make it easier for all economic agents (especially businesses) to seek new loans and boost economic activity.

- When inflation is too high, the RBI typically increases the interest rate, thus incentivising consumers to keep their money in their bank accounts (instead of spending it) while also making it costlier for businesses to take out new loans.

- If the retail inflation is too low, it suggests weak economic activity and one would expect the RBI to lower interest rates to boost GDP.

- Of course, the RBI cannot boost growth as well as curb inflation at the same time. If it chooses to boost growth when inflation is also high, it runs the risk of further fuelling inflation.

Impact of the second Covid-19 wave on Monetary Policy

IMF cut India’s GDP growth forecast for 2021-22 due to:

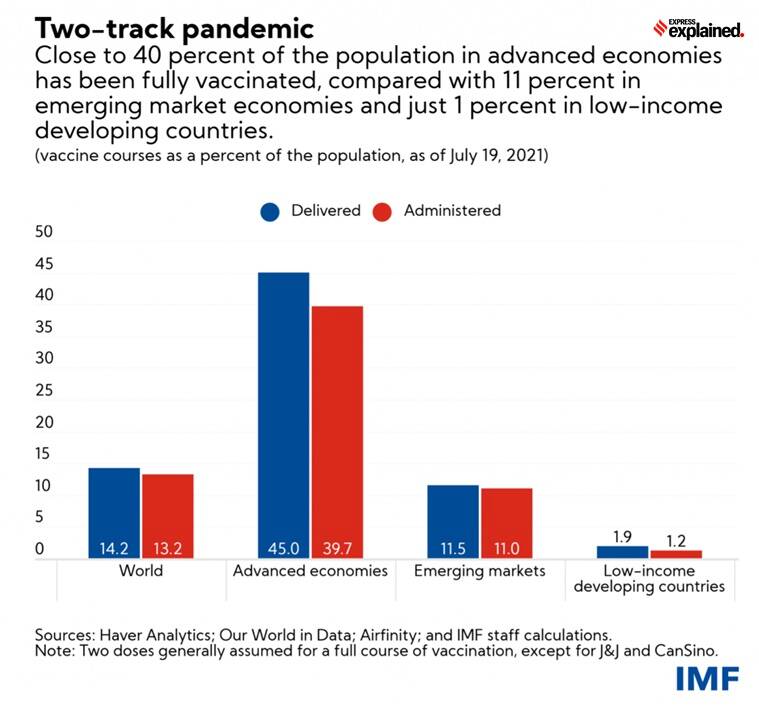

- Inadequate levels of vaccination: Emerging economies such as India have only 11% of their population fully vaccinated — far behind the 40% mark for advanced economies such as the US and UK.

- Policy support that the Indian economy has received: Governments in most advanced economies have unveiled measures to support their economies longer. On the other hand, in the emerging market and developing economies most measures expired in 2020 and they are looking to rebuild fiscal buffers.

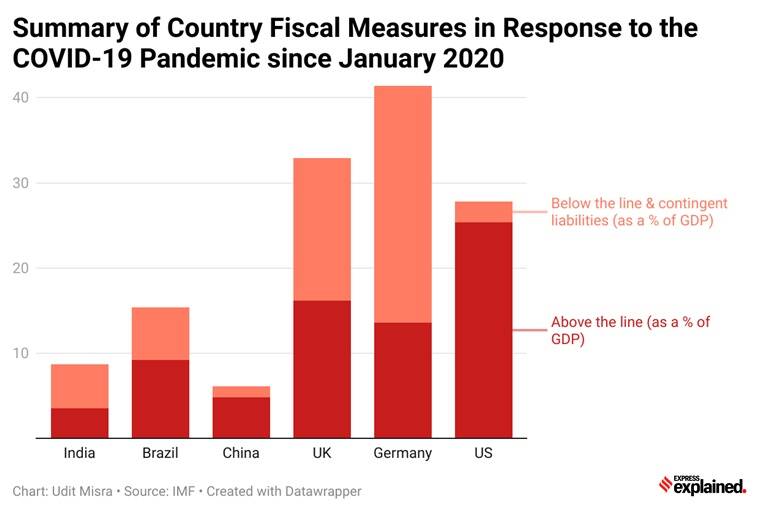

- Nature of policy support: Indian government has favoured the “below the line” measures (policy decisions where instead of a direct immediate outgo from its coffers, the government (including the RBI) provides more loans and credit guarantees) instead of the “above the line” measures (fiscal decisions that boost economic activity by either increasing government expenditures or reducing government revenues). This is contrary to the suggestion of many economists who argue that the Indian economy is in dire need of increased direct spending by the government.

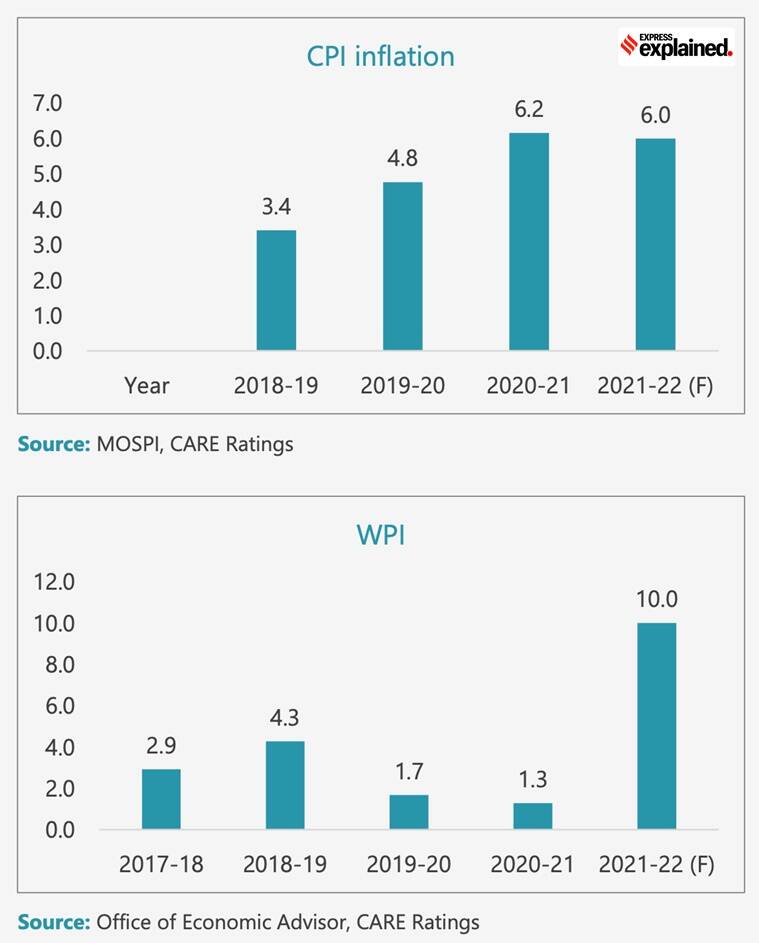

- Inflation: The upshot – Retail inflation, which is the primary target of RBI, is expected to stay outside or almost outside RBI’s comfort zone in 2021-22.

- RBI is unlikely to raise interest rates on August 2021 because India’s economic recovery continues to be quite iffy.

-Source: Indian Express