Context:

By the end of December 2021, the Reserve Bank of India (RBI) released its latest Financial Stability Report (FSR).

Relevance:

GS-III: Indian Economy (Growth and Development of Indian Economy)

Dimensions of the Article:

- What is the Financial Stability Report (FSR)?

- Highlights of the latest FSR (December 2021)

What is the Financial Stability Report (FSR)?

- The FSR is one of the most crucial documents on the Indian economy published twice each year by the Reserve Bank of India (RBI) – and it presents an assessment of the health of the financial system.

- The FSR includes contributions from all the financial sector regulators (details of the current status of different financial institutions such as all the different types of banks and non-banking lending institutions).

- The FSR allows the RBI to assess the macro-financial risks in the economy. (Macro-financial risks refer to the risks that originate from the financial system but affect the wider economy as well as risks to the financial system that originate in the wider economy.)

- As such, the FSR looks into:

- sufficiency of capital for operation of Indian banks (both public and private),

- levels of bad loans (or non-performing assets) and their manageable limits,

- ability of different sectors of the economy to get credit (or new loans) for economic activity etc.

- Accordingly, it reflects the collective assessment of the Sub-Committee of the Financial Stability and Development Council (FSDC-SC) on risks to financial stability.

- The FSR puts together a wealth of data and information that also allows the RBI to assess the state of the domestic economy, especially in a fast-changing global economy.

- As part of the FSR, the RBI also conducts “stress tests” to figure out what might happen to the health of the banking system if the broader economy worsens.

- With the FSR, the RBI also tries to assess how factors outside India — say the crude oil prices or the interest rates prevailing in other countries — might affect the domestic economy.

- Each FSR also contains the results of something called the Systemic Risk Surveys.

Highlights of the latest FSR (December 2021)

Global growth has started to falter

- Since the July 2021 issue of the FSR, the rejuvenation of the global recovery in the first half of 2021 has started losing momentum, impacted by:

- resurgence of infections in several parts of the world,

- supply disruptions and bottlenecks and

- the persistent inflationary pressures that have manifested themselves in their wake.

- The slowdown in activity is occurring even in countries with relatively high vaccination rates that seemed to be emerging as global growth drivers.

- What has complicated matters more is the rise of the Omicron variant. All this has a considerable impact on even the emerging economies (such as India) where vaccination rates are even lower than advanced economies and which are also likely to suffer from central banks in developed countries making money costlier (by raising interest rates).

- The Goods Trade Barometer of the World Trade Organization (WTO) shows that the World merchandise trade volumes, which had risen to over 22% year-on-year in Q2 (April to June) of the 2021 calendar year, have been slowing in the second half of the year.

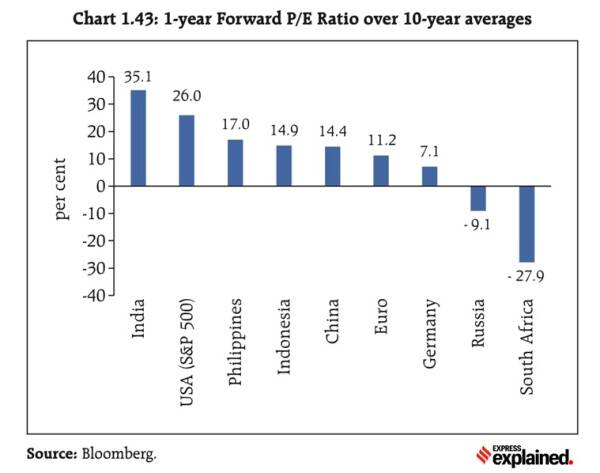

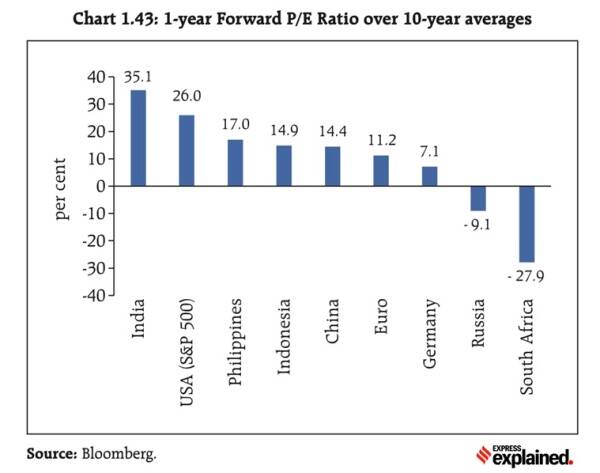

Disconnect between real economy and India’s equity markets

- Lifted by the bull run in equity markets across the globe, the Indian equity market surged on strong rallies with intermittent corrections and strong investor interest has driven up price-earnings (P/E) ratios substantially.

- As of December 13, the one-year forward P/E ratio for India was 35.1 per cent above its 10-year average, and one of the highest in the world.

- This reflects some disconnect between the real economy and equity markets.

- But this is not the first time that RBI frowned at the growing disconnect between the overall state of the economy and the pace at which India’s stock markets have grown. High levels of divergence are a concern from the point of view of financial stability.

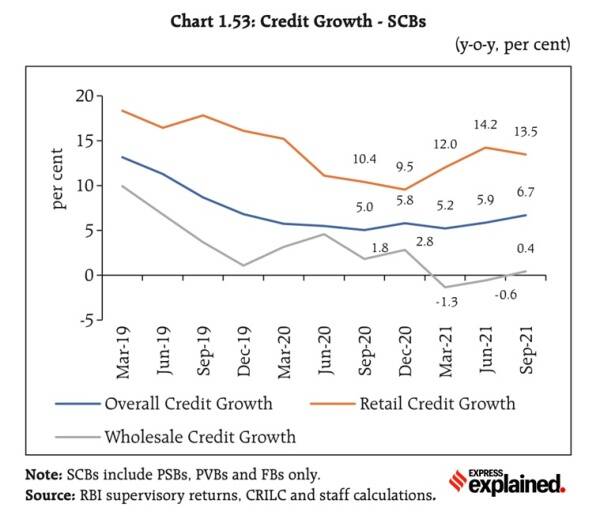

Bank credit growth is improving, but not fast enough

- According to the FSR, the banking stability indicator (BSI), which indicates the changes in underlying conditions and risk factors of India’s commercial banks, showed improvement in “soundness, asset quality, liquidity and profitability” parameters when compared to the situation in March 2021.

- Only in the “efficiency” parameter did this indicator worsen. This is good news since this period includes the disruption due to the vicious second wave of Covid-19.

- Of particular importance is the improvement in the credit growth rate which is beginning to look up and form a “U-shaped” recovery.

- However, within this overall improvement, there are some matters of concern still.

- For once, the growth rate is still far off the ideal level.

- Secondly, retail credit (that is, less than Rs 5 crore) is growing at a decent clip, wholesale credit (Rs 5 crore and above) growth continues to struggle.

- Moreover, data shows that most of the wholesale credit is being picked up by public sector undertakings while the private sector is holding back from raising fresh funding.

- There is also the disturbing fact that bank credit to the MSME segment slowed down (y-o-y) by the end of September 2021 vis-a-vis March 2021.

NPAs may rise by September 2022

- Stress tests indicate that the Gross NPA ratio of all SCBs may increase to 8.1 per cent by September 2022 under the baseline scenario and further to 9.5 per cent under severe stress.

- Among all the banks typically it is public sector banks that are more guilty of such slippages.

- For India, the main sources of risks are commodity prices, domestic inflation, equity price volatility, asset quality deterioration, credit growth and cyber disruptions.

-Source: Indian Express