Context:

The Reserve Bank of India (RBI) proposed to lift the interest rate cap on Microfinance Institutions (MFIs), and said all micro loans should be regulated by a common set of guidelines irrespective of who gives them.

Relevance:

GS-III: Indian Economy (Growth and Development of Indian Economy, Banking, Inclusive Growth)

Dimensions of the Article:

- Concerns with the proposals

- How can the challenges be addressed?

- Back to the Basics: What are Micro Finance Institutions (MFIs)?

- Microfinance in India

- Shift in Microfinance Lending

- Micro Finance Associated Challenges

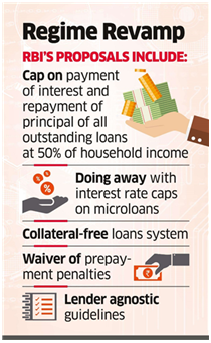

About the RBI’s Microfinance Proposals

- RBI has suggested a common definition of microfinance loans for all regulated entities: Microfinance loans according to RBI should mean collateral-free loans to households with annual household income of Rs 1,25,000 and Rs 2,00,000 for rural and urban/semi urban areas, respectively.

- The RBI also proposed that Non-banking Financial Company (NBFC)-MFIs, like any other NBFC, shall be guided by a board-approved policy and the fair practices code, whereby disclosure and transparency would be ensured.

- RBI has mooted capping the payment of interest and repayment of principal for all outstanding loan obligations of the household as a percentage of the household income, subject to a limit of maximum 50%.

- The RBI also said that there would be NO ceiling prescribed for the interest rate and NO collateral allowed for micro loans.

- Also, there can be NO prepayment penalty, while all entities have to permit the borrowers to repay weekly, fortnightly or monthly instalments as per their choice.

- RBI has reposed faith in the maturity of the microfinance sector with this step. This is a forward-looking step where the responsibility is of the institution to fix a reasonable interest rate on transparent terms.

Concerns with the proposals

- The rate of interest charged by private agencies on microfinance is the maximum permissible, a rate of interest that is far from any notion of cheap credit.

- The actual cost of microfinance loans is even higher for several reasons. An official flat rate of interest used to calculate equal monthly instalments actually implies a rising effective rate of interest over time. A processing fee of 1% is added and the insurance premium is deducted from the principal. As the principal is insured in case of death or default of the borrower or spouse, there can be no argument that a high interest rate is in response to a high risk of default.

- A shift to digital transactions refers only to the sanction of a loan, as repayment is entirely in cash. Contrary to the RBI guideline of “no recovery at the borrower’s residence”, collection was at the doorstep.

- If the borrower is unable to pay the instalment, other members of the group have to contribute, with the group leader taking responsibility.

How can the challenges be addressed?

- A structured survey-based approach could be used to assess a household’s expenses, debt position and income from various sources of occupation

- A template-based approach where various templates for different categories of households (as per location, occupation type, family characteristics, etc.) could be used

- Centralised database can be used to collect and maintain household income data for uniformity in data collection

- Technology can be used to assess the cash flows and repayment capacity of micro-enterprises

- An overarching set of principles to prevent mis-selling by retail lenders is needed

Back to the Basics: What are Micro Finance Institutions (MFIs)?

- Micro finance Institutions, also known as MFIs, a microfinance institution is an organisation that offers financial services to low-income populations.

- Usually, their area of operations of extending small loans are rural areas and among low-income people in urban areas.

- MFIs provide the much-needed aid to the economically underprivileged who would have otherwise been at the mercy of the local moneylender and high interest rates.

- The model had its genesis as a poverty alleviation tool, focused on economic and social upliftment of the marginalised sections through lending of small amounts of money without any collateral to women for income-generating activities.

- Some of the MFIs, that qualify certain criteria and are non-deposit taking entities, come under RBI wings for Non-Banking Financial Company (NBFC) Regulation and supervision. These “Last Mile Financiers” are known as NBFC MFI.

- The objective of covering them under RBI was to make these NBFC MFIs healthy and accountable.

History of Microfinance

- The term “microfinancing” was first used in the 1970s during the development of Grameen Bank of Bangladesh, which was founded by the microfinance pioneer, Muhammad Yunus.

- Since, in the developing countries, a large number of people still depends largely on subsistence farming or basic food trade for their livelihood, therefore, smallholder agriculture in these developing countries has been supported by the significant resources.

Microfinance in India

- SEWA Cooperative Bank was initiated in 1974 in Ahmedabad, Gujarat, by Ela Bhatt which is now one of the first modern-day microfinance institutions of the country.

- The National Bank for Agriculture and Rural Development (NABARD) offered financial services to the unbanked people, especially women and later decided to experiment with a very different model, which is now popularly known as Self-help Groups (SHGs).

- The SHG-Bank linkage programme in India has savings accounts with 7.9 million SHGs and involves the participation of regional rural banks (RRBs), commercial banks and cooperative banks in its operations. The origin of SHGs in India can be traced back to the establishment of the Self-Employed Women’s Association (SEWA) in 1972.

- In 2013, a loan of $144 million was provided by Grameen Capital India to the microfinance groups. Apart from the Grameen Bank, another microfinance organization named Equitas was developed in Tamil Nadu. The Southern and Western states of India are the ones attracting the greatest number of microfinance loans.

Shift in Microfinance Lending

- In the 1990s, microcredit was given by scheduled commercial banks either directly or via non-governmental organisations to women’s self-help groups, but given the lack of regulation and scope for high returns, several for-profit financial agencies such as NBFCs and MFIs emerged.

- By the mid-2000s, there were widespread accounts of the malpractices of MFIs and a crisis in some States such as Andhra Pradesh, arising out of a rapid and unregulated expansion of private for-profit micro-lending.

- The microfinance crisis of Andhra Pradesh led the RBI to review the matter, and based on the recommendations of the Malegam Committee, a new regulatory framework for NBFC-MFIs was introduced in December 2011.

- At present, privately-owned for-profit financial agencies are the “regulated entities”. They have been promoted by the RBI.

- Lending by small finance banks (SFBs) to NBFC-MFIs has been recently included in priority sector advances.

- Post-COVID-19, the cost of funds supplied to NBFC-MFIs was lowered, but with no additional restrictions on the interest rate or other parameters affecting the final borrower.

- 31% of microfinance is provided by NBFC-MFIs, and another 19% by SFBs and 9% by NBFCs. These private financial institutions have grown exponentially over the last few years, garnering high profits. At this pace, the current share of public sector banks in microfinance (the SHG-bank linked microcredit), of 41%, is likely to fall sharply.

Micro Finance Associated Challenges

- Inadequate Data: While overall loan accounts have been increasing the actual impact of these loans on the poverty-level of clients is sketchy as data on the relative poverty-level improvement of MFI clients is fragmented.

- Impact of COVID-19: It has impacted the MFI sector, with collections having taken an initial hit and disbursals yet to observe any meaningful thrust.

- Social Objective Overlooked: In their quest for growth and profitability, the social objective of MFIs—to bring in improvement in the lives of the marginalized sections of the society—seems to have been gradually eroding.

- Loans for Conspicuous Consumption: The proportion of loans utilized for non-income generating purposes could be much higher than what is stipulated by RBI. These loans are short-tenured and given the economic profile of the customers, it is likely that they soon find themselves in the vicious debt trap of having to take another loan to pay off the first.

-Source: The Hindu