2019 — 50th anniversary of bank nationalization.

Since 1969, India has grown significantly to become the 5th largest economy in the world. Yet, India’s banking sector is disproportionately under-developed given the size of its economy.

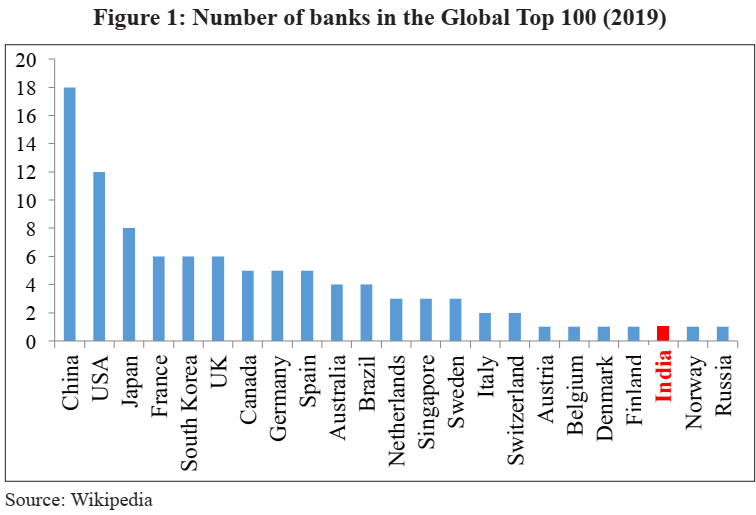

- For instance, India has only one bank in the global top 100 – same as countries that are a fraction of its size — Finland (about 1/11th), Denmark (1/8th)

- Countries like Sweden (1/6th) and Singapore (1/8th) have thrice the number of global banks.

- In terms of proportion – India should have six banks in the top 100.

- Also, the disproportionately lower penetration is not just because of our huge population but something else too.

- PSBs account for 70% of the market share — fostering its economic development falls on them.

Similarly, India becoming a $ 5 trillion economy will require at least eight Indian banks to be large enough to belong in the top 100 globally.

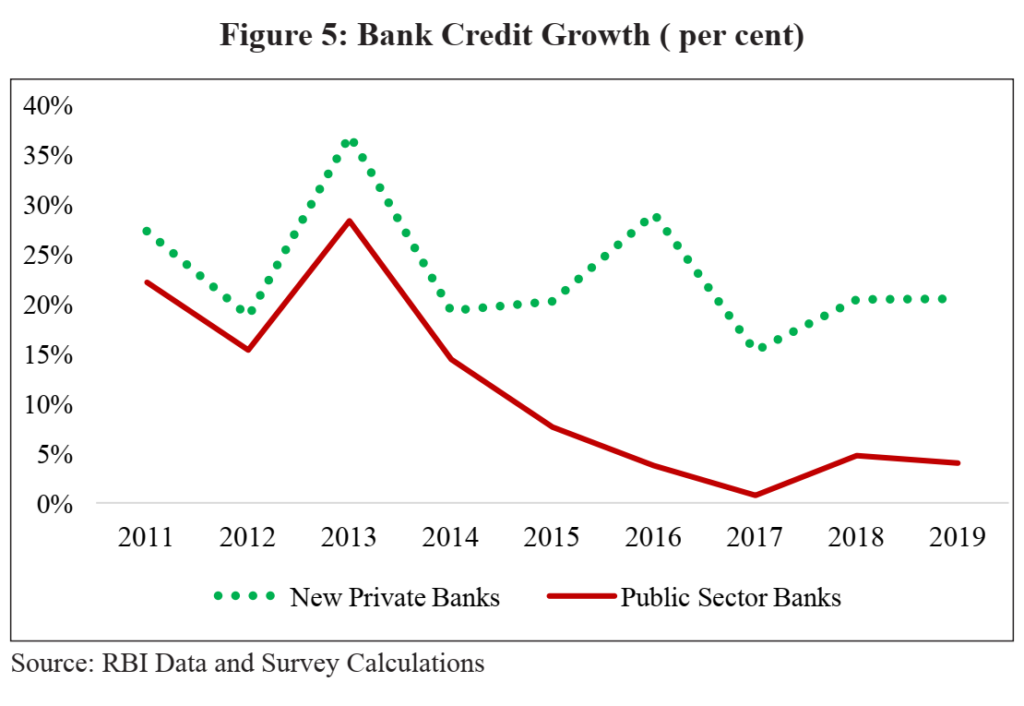

Credit growth among PSBs has declined significantly since 2013 and has also been anaemic since 2016.

- However, in 2019, PSBs’ collective loss— largely due to bad loans—amounted to over INR 66,000 crores

- PSBs account for 85% of reported bank frauds while their gross non-performing assets (NPAs) equal INR 7.4 lakh crores which is more than 150% of the total infrastructure spend in 2019.

- Even as New Private Banks (NPBs) grew credit at between 15% and 29% per year between 2010 and 2019, PSB credit growth essentially stalled to the single digits after 2014, ending up at a 4.03% growth in 2019 compared 15% to 28% from 2010 to 2013.

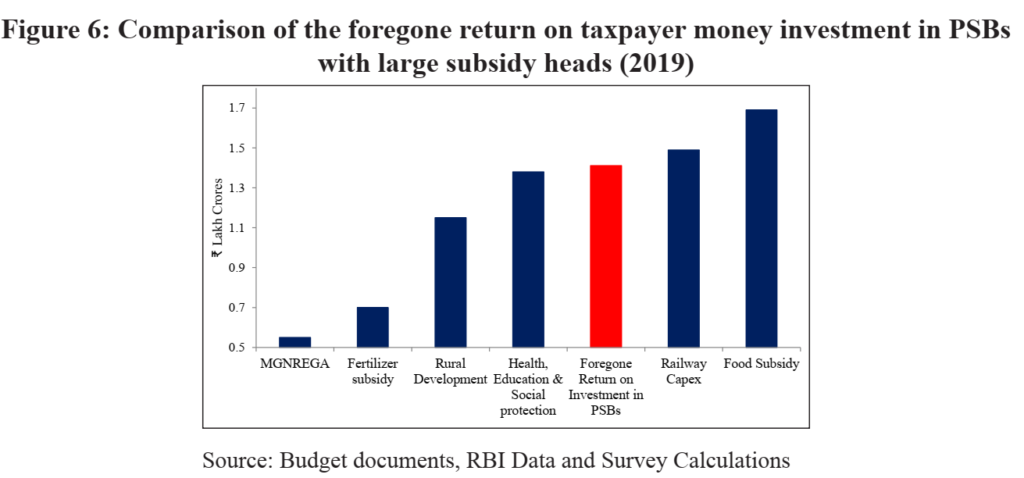

The scale of inefficiencies in PSBs can be estimated through losses that happen when a tax payer puts his money in PSBs as against investing in the NPB — return is the benchmark

BANKING STRUCTURE: FROM NATIONALIZATION TILL TODAY

SBI — 55th largest bank globally — founded as Bank of Calcutta in 1806, took the name Imperial Bank of India in 1921 and became state-owned in 1955.

- The remaining PSBs nationalised in 1969 and 1980.

- After the1980 — PSBs had a 91% share

Benefits of Nationalisation of Banks

- The allocations of banking resources to rural areas, agriculture, and priority sectors increased.

- Both rural bank deposit mobilization and rural credit increased significantly after the1969 nationalization.

- This growth represents a significant correction to the under supply of credit to farmers that drove nationalization.

Confounding effects are introduced by the policies pursued by RBI after nationalization.

- Its directed lending programmes set lending targets for priority sectors, using a complex mix of pricing formulas — mark of central planning

- RBI used both formal means and moral suasion to persuade banks to achieve the targets it set.

- These tools carried special force given that banks were essentially operating in a marketplace sheltered from entry.

Today, however, with no real restrictions on what can be investigated and under what circumstances, officers of state-run banks are wary of taking risks in lending or in renegotiating bad debt, due to fears of harassment under the veil of vigilance investigations.

THE WEAKENING OF PUBLIC SECTOR BANKS

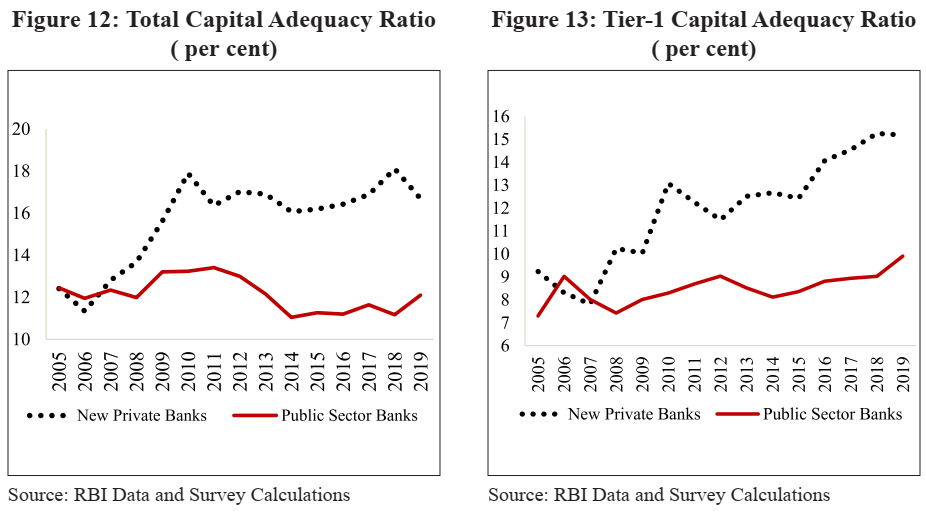

Trends over time that contrast PSBs and NPBs in a “difference-in-difference” sense reveal that the PSB weaknesses did not develop suddenly. Asset quality problems that have developed over a few years are at the root of the PSB performance slide.

The 2014 P. J. Nayak Committee report shows that the structural weaknesses in the PSBs explain their poor performance – set of systemic factors

- Combination of unsustainable macro economic policies

- Market failures

- Regulatory distortions

- Government interference in the allocation of capital.

Moreover, crises that are not resolved effectively and swiftly impose enormous costs on society.

Credit growth in PSBs has been much lower than NPBs for the last several years.

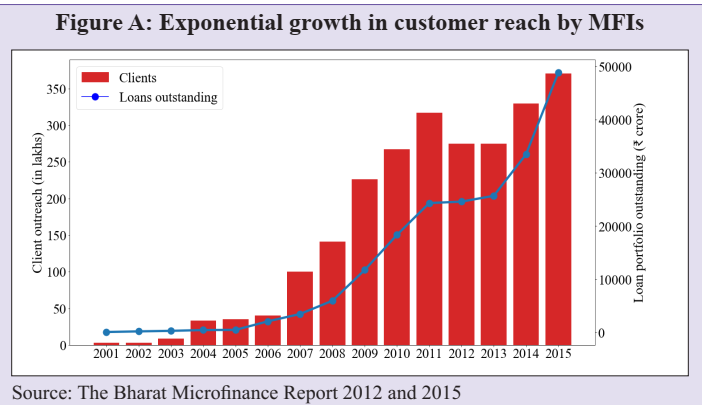

Microfinance Institutions:

Most micro-finance institutions (MFIs) started as not-for-profit institutions. Post-2000, while their objective remained poverty alleviation via inclusive growth and financial inclusion, MFIs moved from purely pursuing social goals to the double bottom-line approach of achieving social and financial returns.

- Some banks partnered with MFIs by lending to MFIs for on-lending the money to this segment and thereby fulfil their priority lending obligations.

- The United Nation’s declaration of Micro-finance year in 2005 highlighted the role of MFIs in poverty alleviation. Some MFIs have transformed themselves into banks as well.

- Figure A shows the exponential growth in the impact that MFIs have had since 2000.

- As of 2016, 97% of the borrowers were women with SC/ST and minorities accounting for around 30% and 29% of the borrowers.

- This shows that the loans that have been given by these MFIs primarily cater to the marginal sections of the society.

- The micro-finance sector, especially given its transformation since 2000, provides a good illustration of how social goals can be achieved at scale using business models that are different from that of PSBs.

ENHANCING EFFICIENCY OF PSBs: THE WAY FORWARD

The key drivers of India’s growth prospects are now:

- Highly favourable demographics – with 35% of its population between 15 and 29 years of age;

- A modern and modernizing digital infrastructure that encompasses the “JAM” trinity of financial inclusion, the Aadhaar Unique Identification System, and a well-developed mobile phone network

- A uniform indirect taxation system (GST) tore place a fragmented, complex state-level system

These investments have set the stage for a modern economy in which tens of crores of individuals and businesses are entering the formal financial system.

India’s growth path depends on how quickly and productively these growth levers are deployed using a well-developed financial system.

- Employee Stock Ownership Plan (ESOP) for PSBs’ employees: To incentivize employees and align their interests with that of all shareholders of banks, bank employees should be given stakes through an employee stock ownership plan (ESOP) together with proportionate representation on boards, proportionate to the blocks held by employees.

- With the cleaning up of the banking system and the necessary legal framework such as the Insolvency and Bankruptcy Code (IBC), the banking system must focus on scaling up efficiently to support the economy

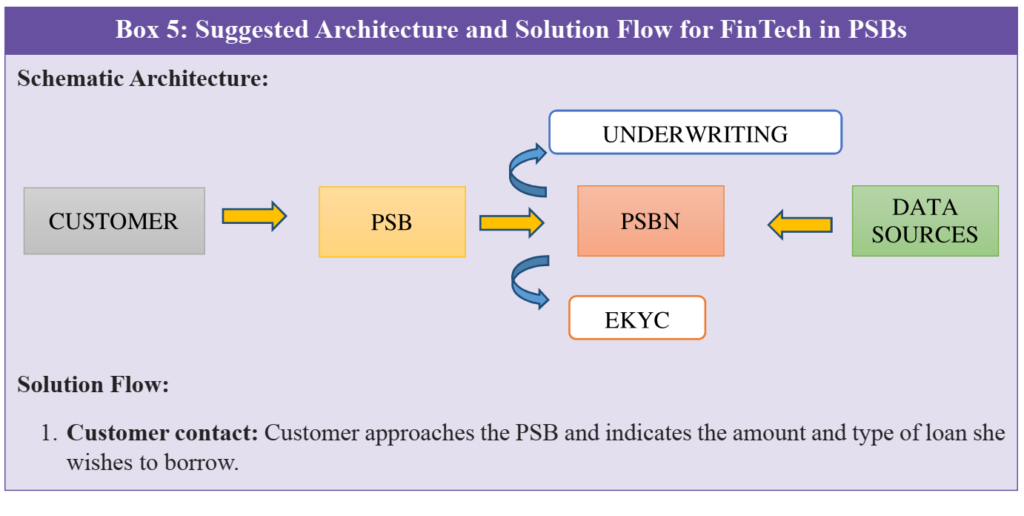

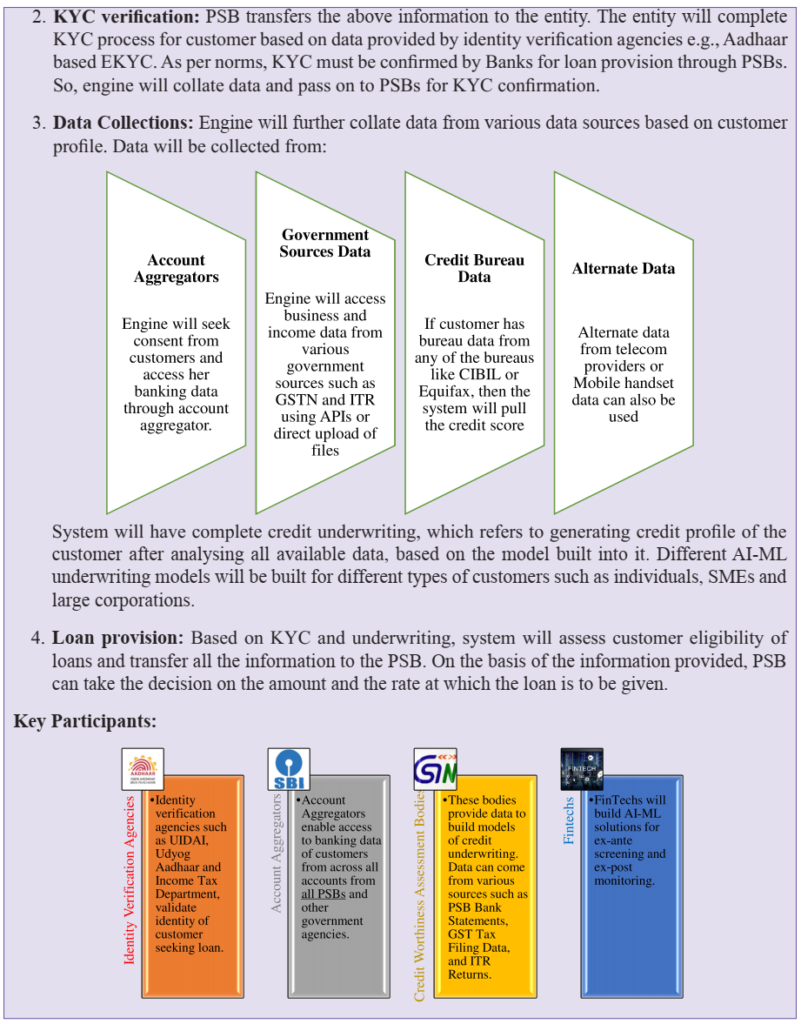

Fintech Hub

The survey proposes an establishment of an entity like GSTN called as PSBN (PSB Network) to use technology to screen and monitor borrowers widely. Apart from information exchange, PSBN could utilizes govt. sources and services to put in place AI-ML rating models for corporate.

The network would help in better decision making on credit underwriting and reduce burden on NPAs. Further it would bring down the operating costs of PSU Banks as the process of lending gets automated end-to-end, enabling PSU banks to take quicker decision, process loan application speedily and reduce TAT (Turn around Time)

MCQs

- Which of the following is/are the benefits of the nationalisation of the banks in India?

1- The number of rural bank branches increased.

2- Credit to rural areas increased.

3- Credit to agriculture expanded.

Select the correct answer using the codes given below.

A. 1 and 2 only

B. 2 and 3 only

C. 1 only

D. 1, 2, and 3

Ans. (D) The allocations of banking resources to rural areas, agriculture, and priority sectors increased after the nationalisation of the banks. The number of rural bank branches increased ten-fold from about 1,443 in 1969 to 15,105 in 1980 compared to a two-fold increase in urban and semi-urban areas from 5,248 to 13,300 branches.

Credit to rural areas increased from ` 115 crores to ` 3,000 crores, a twenty-fold increase and deposits in rural areas increased from ` 306 crores to ` 5,939 crores, again a twentyfold increase. Between 1969 and 1980, credit to agriculture expanded forty-fold from ` 67 crores to ` 2,767 crores, reaching 13 per cent of GDP from a starting point of 2 per cent. This growth represents a significant correction to the undersupply of credit to farmers that drove nationalization. Both rural bank deposit mobilization and rural credit increased significantly after the 1969 nationalization. - Which of the following committees were related to the banking sector?

1- Narasimhan Committe

2- Rajan Committee

3- P J Nayak Committee

Select the correct answer using the codes given below.

A. 1 only

B. 1 and 2 only

C. 2 and 3 only

D. 1, 2, and 3

Ans. (D) The Government of India appointed a nine-member committee headed by M. Narasimham, the former Governor of RBI on August 14, 1991. The committee was appointed to review the working of the commercial banks and other financial institutions of the country and to suggest measures to remodel these institutions for raising their efficiency.

In 1998 the government-appointed yet another committee under the chairmanship of Mr Narsimham. It is better known as the Banking Sector Committee. It was told to review the banking reform progress and design a programme for further strengthening the financial system of India. The committee focused on various areas such as capital adequacy, bank mergers, bank legislation, etc.

The Raghuram Rajan Committee on Financial Sector Reforms was a committee constituted by the Government of India in 2007 for proposing the next generation of financial sector reforms in India.

The P J Nayak Committee or officially the Committee to Review Governance of Boards of Banks in India was set up by the Reserve Bank of India (RBI) to review the governance of the board of banks in India. The Committee was set up in January 2014. The Committee was chaired by P J Nayak, the former CEO and Chairman of Axis Bank. - Consider the following statements regarding Microfinance institutions (MFIs):

1- The primary objective of MFIs is poverty alleviation via inclusive growth and financial inclusion.

2- Women borrowers account for 97 percent of total borrowers from MFIs.

3- At present GST of 18 percent is levied on the loans disbursed through MFIs.

Which of the statements given above is/are correct?

A. 1 and 2 only

B. 2 only

C. 1 and 3 only

D. 1, 2 and 3

Ans. (D) Microfinance is increasingly being considered as one of the most effective tools of reducing poverty by enabling microcredit to the financially poor. The Micro Finance Institutions (MFIs) accesses financial resources from the Banks and other mainstream Financial Institutions and provide financial and support services to the poor. •Most microfinance institutions (MFIs) started as not-for-profit institutions. Post-2000, MFIs moved from purely pursuing social goals to the double bottom-line approach of achieving social and financial returns. Their objective remained poverty alleviation via inclusive growth and financial inclusion. Hence, statement 1 is correct.

•The United Nation‘s declaration of Microfinance year in 2005 highlighted the role of MFIs in poverty alleviation.

•According to Economic Survey 2019-20, 97 percent of the borrowers in MFIs were women with SC/ST and minorities accounting for around 30 percent and 29 percent of the borrowers respectively.

Hence, statement 2 is correct. Many of the MFIs operating in the country work as banking correspondents for the banks for credit disbursements for which an 18 percent GST is levied on overall borrowing by beneficiaries. Hence, statement 3 is correct. - With reference to India’s banking sector, consider the following statements:

1- India has only one bank in the global top 100.

2- The Public Sector Banks (PSBs) account for 70 per cent of the market share in banking.

Which of the above statements is/are correct?

A. 1 only

B. 2 only

C. Both 1 and 2

D. Neither 1 nor 2

Ans. (C) Learning Zone: In 2019, India completed the 50th anniversary of bank nationalization.

Since 1969, India has grown significantly to become the 5th largest economy in the world.

Yet, India’s banking sector is disproportionately under-developed given the size of its economy.

For instance, India has only one bank in the global top 100.

As PSBs account for 70 per cent of the market share in Indian banking, the onus of supporting the Indian economy and fostering its economic development falls on them. - Consider the following statements regarding Public Sector Banks (PSBs) in India:

1- PSBs account for more than half of the loans by the Indian banking sector.

2- Credit growth among PSBs has consistently declined in the last five years.

Which of the statements given above is/are correct?

A. 1 only

B. 2 only

C. Both 1 and 2

D. Neither 1 nor 2

Ans. (A) Public Sector Banks (PSBs) are a major type of bank in India, where a majority stake (i.e. more than 50%) is held by a government. Rest of the shares may be held by retail investors, private institutions, mutual funds etc.

There are a total of 12 Public Sector Banks •PSBs account for 70 percent of the market share in Indian banking. Hence, statement 1 is correct. Being a public sector bank, the onus of supporting the Indian economy and fostering its economic development falls on them. It is reflected in a higher percentage of bad loans. PSB contributes about 87% of total bad loans.