NBFC:

- Financial institutions that offer various banking services but do not have a banking license.

- They are primarily responsible for making investments but do not have the authority to accept deposits.

- NBFCs cannot form part of the payment and settlement system.

- This means that cannot issue cheques drawn on itself.

- The deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation is not available to depositors of NBFCs, unlike in the case of banks.

Housing Finance Company (HFC)

- company registered under the Companies Act which primarily transacts or has as one of its principal objects, the transacting of the business of providing finance for housing, whether directly or indirectly.

IL&FS

- Infrastructure Leasing & Financial Services Limited is an Indian infrastructure development and finance company (NBFC).

- It operates through more than 250 subsidiaries.

DHFL

- DHFL is an HFC (a category of NBFC) that provides easy access to affordable Housing Finance to millions of lower– and middle–income families in semi-urban and rural India.

Mutual Fund

A mutual fund is a type of investment vehicle consisting of a portfolio of stocks, bonds, or other securities. Mutual funds give small or individual investors access to professionally managed portfolios of equities, bonds, and other securities. Each shareholder, therefore, participates proportionally in the gains or losses of the fund.

Liquid Debt Mutual Funds (LDMF)

- The LDMF sector is a primary source of short-term wholesale funds in the NBFC sector. This means that the NBFC sector is intricately interconnected with the LDMF sector.

Liquidity crunch (limited/restricted flow of money): It often leads to credit rationing.

- Credit rationing results when firms with robust financial and operating performance get access to credit while the less robust ones are denied credit.

- Firms with robust financial and operating performance can withstand a prolonged period of liquidity crunch if they choose not to raise funds from debt mutual funds.

Money Market

The money market is the trade of short-term debt investments. At the wholesale level, it involves large volume trades between institutions and traders. At the retail level, an individual may invest in the money market by purchasing a money market mutual fund, buying a Treasury bill, or opening a money market account at a bank.

Provisioning Norms

Provisioning is a part of the RBI’s prudential regulation norm. Under provisioning, banks have to set aside or provide funds to a prescribed percentage of their bad assets. The assets are classified by the RBI in terms of their duration of non-repayment.

Basel Norms

These norms provide banks with a common goal of financial stability and standards of banking regulation.

- The purpose of the Basel norms is to ensure that financial institutions have enough capital on account to meet obligations and absorb unexpected losses.

- India has accepted Basel accords for the banking system.

- In fact, on a few parameters, the RBI has prescribed stringent norms as compared to the norms prescribed by BCBS (Basel Committee on Banking Supervision).

Bank Run

A bank run occurs when a large number of customers of a bank or other financial institution withdraw their deposits simultaneously over concerns of the bank’s solvency. As more people withdraw their funds, the probability of default increases, prompting more people to withdraw their deposits.

Commercial Paper

Commercial Paper (CP) is an unsecured money market instrument issued in the form of a promissory note.

Rollover risk

Financial institutions rely on short-term financing to fund long-term investments. This reliance on short term funding causes an asset-liability management/Mismatch (ALM) problem because asset side shocks expose financial institutions to the risk of being unable to finance their business.

Asset liability management risk (ALM)

This risk arises in most financial institutions due to a mismatch in the duration of assets and liabilities. Liabilities are of much shorter duration than assets which tend to be of longer duration, especially loans given to the housing sector. This mismatch implies that an NBFC must maintain a minimum amount of cash or cash-equivalent assets to meet its short-term obligations.

Refinance

A refinance occurs when an individual or business revises the interest rate, payment schedule, and terms of a previous credit agreement.

Redemption

In finance, redemption describes the repayment of any money market fixed-income security at or before the asset’s maturity date.

Risks involved in Investment

It refers to the chance an outcome or investment’s actual gains will differ from an expected outcome or return. Risk includes the possibility of losing some or all of the original investment.

Retail Funding

A retail fund is an investment fund with capital primarily invested by individual investors. Mutual funds and exchange-traded funds (ETFs) are common types of retail funds that are intended for ordinary investors.

Wholesale Funding

Wholesale funding means that a financial institution receives deposits from sources outside of traditional consumer and retail deposits. These funds come from larger entities, such as governments or fellow financial institutions. Wholesale funding differs from retail funding in that the latter focuses heavily on small businesses like stores and restaurants.

Shadow banking

Shadow banking comprises a set of activities, markets, contracts and institutions that operate partially (or fully) outside the traditional commercial banking sector and are either lightly regulated or not regulated at all.

- A shadow banking system can be composed of a single entity that intermediates between end-suppliers and end-users of funds, or it could involve multiple entities forming a chain.

- NBFCs are considered as an important segment of the shadow banking system in India.

Capital Adequacy Ratio (CAR)

The capital adequacy ratio (CAR) is a measurement of a bank’s available capital expressed as a percentage of a bank’s risk-weighted credit exposures. The capital adequacy ratio, also known as capital-to-risk weighted assets ratio (CRAR), is used to protect depositors and promote the stability and efficiency of financial systems around the world

NBFC crises

- From June to September 2018, two subsidiaries of Infrastructure Leasing & Financial Services (IL&FS) defaulted on their payment obligation.

- Dewan Housing Finance Limited (DHFL) defaulted on its payment obligation from June to August 2019.

- Both IL&FS and DHFL are NBFCs and they defaulted on non convertible debentures and commercial paper obligations.

- In response to the defaults, mutual funds started selling off their investments in the NBFC sector to reduce exposure to stressed NBFCs.

The impact of payment defaults was not limited to debt markets. There was a sharp decline in the equity prices of stressed NBFCs as equity market participants anticipated repayment troubles at these firms.

Hence, both debt and equity investors suffered a massive erosion in wealth due to these defaults.

Increasing redemption pressure prevented Debt mutual funds from refinancing the NBFC sector. Redemption pressure faced by debt mutual funds is akin to a “bank run”, which is a characteristic of any crisis in the financial sector. The redemption pressure gives rise to refinancing risk (rollover risk) for NBFCs, thereby affecting the real sector.

- The extent of refinancing risk faced by NBFCs is fundamentally driven by their reliance on short-term wholesale funding.

- The wholesale funding sources of the NBFCs comprise mainly of banks (primarily via term loans) and debt mutual funds (via non-convertible debentures and commercial paper).

- Since the banks were already facing NPAs, now with the NBFC sector facing refinance trouble, the overall credit growth in the Indian economy took a dip. This led to a decline in the GDP growth.

What’s the relation between Credit growth, NBFC, and liquidity?

When banks and NBFC lend money, it is considered as Credit growth. This credit provides liquidity (flow of money) in the market. If it is easily available, the rate of interest to obtain this credit is low. This helps MSME and others to scale up their investment.

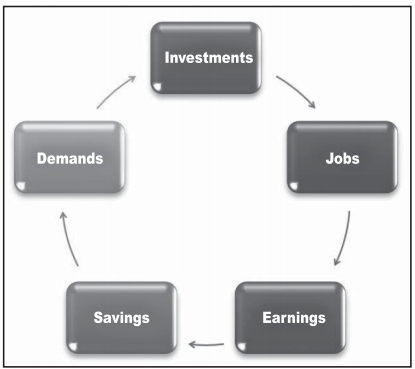

If there is an investment in the economy, people get jobs. They earn, and hence there is an increase in demand for services and products like a new home loan, a car or holiday packages. A significant part of earning from job/work is also put to savings, which along with investment component is again put to productive use in the economy. Thus creating a virtuous cycle of investment – Jobs – earning – savings – demands – investments.

Since most of the banks are reeling under Basel norms and rising NPA, the lower spectrum of the economy was financed by NBFC. In the event of their failure, the opportunity of credit creation will take a hit. With no one left to give credit (money) to the investor at a cheaper rate of interest, the liquidity will not be easily available, thus impacting growth. And, that’s the relationship which exists between credit growth, NBFCs, and liquidity.

What drives redemption (LDMF sector) and Rollover Risk problems (NBFC sector)?

- The magnitude of the ALM problem in the NBFC

- The interconnectedness of the NBFC with the LDMF sector

- The resilience of the NBFC as reflected in the strength of the balance sheet

These three risks work in tandem to cause Rollover Risk. At the time of refinancing their CP obligations, the NBFCs having stronger balance sheets are successful in rolling over CPs, albeit at a higher cost. Other NBFCs with weaker balance sheets face higher default probabilities and find it difficult to access the CP market at affordable rates or are unable to raise money at all, i.e., they are unable to avoid default.

Since NBFCs are that important, it gets crucial to predict their failure. This prediction exercise can be done by creating an Early Warning system that can help devise a Health Index for NBFCs.This Health index will estimate the financial fragility of the NBFC sector and can predict the constraints on external financing (or refinancing risk)faced by NBFC firms.

Health Index

Health Score of a stressed NBFC and the HFC sector will serve a critical role in predicting refinancing related stress (rollover risk) faced by the financial firms in advance. It can serve as an important monitoring mechanism to prevent such problems in the future.

This index will range from-100to +100. A higher score will indicate higher financial stability of the firm/sector (lower Rollover Risk). It will give information on the key drivers of refinancing risks such as Asset Liability Management (ALM) problems, excess reliance on short-term whole-sale funding (Commercial Paper), and balance sheet strength of the NBFCs.

In fact, if we disaggregate these components and examine their trends, then it can shed light on how to regulate NBFCs. Other than its utility as a leading indicator of stress in the NBFC sector, the Health Score can also be used by policymakers to allocate scarce capital to stressed NBFCs in an optimal way to alleviate a liquidity crisis.

Key Metrics affecting Health Scores

- Short-Term Volatile Capital: This is measured by CP as a percentage of borrowings of the NBFC.

- Asset Quality: This is measured by the ratio of retail loans to the overall loan portfolio.

- Short-term Liquidity: This is measured by the percentage of cash to the total borrowings.

- Provisioning Policy: This is measured by the difference between provision for bad loans made in any financial year and the gross non-performing assets (NPA) in the subsequent financial year.

- Capital Adequacy Ratio (CAR): This is the sum of Tier-I and Tier-II capital held by the NBFC as a percentage of Risk-Weighted Assets (RWA).

- Liquidity Buffer levels in the LDMF Sector: This is measured by the average proportion of highly liquid investments such as cash, G-Securities, etc., that are held by the LDMFs.

- Operating Expense Ratio (Opex Ratio): This is measured by the operating expenses in a financial year divided by the average of the loans outstanding in the current financial year-end and previous financial year-end. Opex Ratio is an indicator of the efficiency of a Retail-NBFC.

Concluding remarks

This chapter has analysed firms in the NBFC sector which are susceptible to rollover risk when they rely too much on the short-term wholesale funding market for financing their investments. The following policy initiatives can be employed to arrest financial fragility in the shadow banking system:

- Regulators can employ the Health Score methodology presented in this analysis to detect early warning signals of impending rollover risk problems in individual NBFCs.

- Downtrends in the Health Score can be used to trigger greater monitoring of an NBFC.

- An analysis of the trends in the components of the Health Score can shed light on the appropriate corrective measures that should be applied to reverse the adverse trends.

- When faced with a dire liquidity crunch situation, regulators can use the Health Score as a basis for optimally directing capital infusions to deserving NBFCs to ensure efficient allocation of scarce capital.

- This analysis can also be used to set prudential thresholds on the extent of wholesale funding that can be permitted for firms in the shadow banking system.

MCQs

- Consider the following statements:

1- Housing Finance Corporations(HFCs) hold much longer duration assets as compared to Retail-NBFCs, which hold medium-term assets.

2- Asset side shocks cause a significant deterioration in the asset-liability mismatch of the HFCs, but they induce less of an adverse impact on the asset-liability mismatch of Retail NBFCs.

Which of the above statements is/are correct?

A. 1 only

B. 2 only

C. Both 1 and 2

D. Neither 1 nor 2

Ans. (C) The drivers of Rollover Risk differ between HFCs and Retail-NBFCs are demonstrated first due to the following reasons. First, HFCs hold much longer duration assets (housing loans, developer loans etc.,) as compared to Retail-NBFCs, which hold medium-term assets (auto, consumer durables, gold loans, etc.,). HFCs face a greater gap between the average maturity of their assets and liabilities, as compared to Retail-NBFCs, which typically provide loans of shorter duration in the form of working capital loans to MSME, automobile financing loans or gold loans. Thus, asset side shocks cause a significant deterioration in the asset-liability mismatch of the HFCs, but they induce less of an adverse impact on the asset-liability mismatch of Retail-NBFCs. - Consider the following statements about the “Shadow Banking”:

1- Shadow banks do not have explicit access to central bank liquidity.

2- They operate outside the traditional commercial banking sector.

Which of the above statements is/are correct?

A. 1 only

B. 2 only

C. Both 1 and 2

D. Neither 1 nor 2

Ans. (C) Shadow banking comprises a set of activities, markets, contracts and institutions that operate partially (or fully) outside the traditional commercial banking sector and are either lightly regulated or not regulated at all.

A shadow banking system can be composed of a single entity that intermediates between end-suppliers and end-users of funds, or it could involve multiple entities forming a chain”. Shadow banks do not have explicit access to central bank liquidity.

The shadow banking system is highly levered with risky and illiquid assets while its liabilities disposed to “bank runs”.