Contents

- A recipe to tear down trade unions

- Analysis of the Aatma Nirbhar Bharat Abhiyaan

A RECIPE TO TEAR DOWN TRADE UNIONS

Context:

The new labour laws are a brutal attack on workers’ ability to safeguard their rights

Relevance:

GS Paper 3: Indian Economy (issues re: planning, mobilisation of resources, growth, development, employment); Inclusive growth and issues therein.

Mains questions

- The major challenge in labour reforms is to facilitate employment growth while protecting workers’ rights. Elaborate. 15 marks

- The new code appears to be designed to deter collective action by workers’ unions, and make them fearful of getting trapped in the cross hairs of the new, supposedly “simplified” code. Comment. 15 marks

Dimensions of the Article

- Objectives of labour reforms.

- Consolidations of labour laws.

- Issues related to new labour laws

- Way forward

Objective of the Labour reforms

Labour is a concurrent list subject, thus there is multiplicity of laws at Centre and the State levels. Amidst this, the focus of labour reforms should be twin-fold: to promote creation of formal sector jobs, and to not stifle employers by over-protection of workers.

- Consolidation and simplification of numerous States’ and Centre labour laws.

- Streamlining of Minimum Wages in the country and ensuring they reach the beneficiaries.

- Introduction of fixed term employment, to curb tendency for employing (socially insecure) contract labour.

Consolidations of the labour laws

The 2nd National Commission of labour had recommended simplification, amalgamation and rationalisation of Central Labour Laws. In 2019, the Ministry of Labour and Employment introduced four Bills on labour codes to consolidate 29 central laws. These Codes regulate: (i) Wages, (ii) Industrial Relations, (iii) Social Security, and (iv) Occupational Safety, Health and Working Conditions.

Labour Code on Wages , 2019: Key Provisions

- The Code will apply to any industry, trade, business, manufacturing or occupation including government establishments.

- Wages include salary, allowance, or any other component expressed in monetary terms. This will not include bonus payable to employees or any travelling allowance, among others.

- It differentiates the central and State Jurisdiction in determining the wage related decision for establishment such as Railways Mines and oil fields.

- A concept of statutory National Minimum Wage for different geographical areas has been introduced. It will ensure that no State Government fixes the minimum wage below the National Minimum Wages for that particular area as notified by the Central Government.

Why Labour code on Wages is needed?

- It arises in the absence of statutory National Minimum Wage for different regions, which impedes the economic prospect.

- It seeks to consolidate laws relating to wages by replacing– Payment of Wages Act, 1936; Minimum Wages Act, 1948; Payment of Bonus Act, 1965 and Equal Remuneration Act, 1976.

Labour Code on Industrial Relations: Key Provisions

- It increases the employee limit from 100 to 300 above which, the government approval is needed for layoff/retrenchment/closure. This provision has been criticized sharply by the labour groups and trade unions.

- It provides that 10% of workers shall apply (be applicant) for registering a trade union – this has also invited opposition from various worker groups and trade unions.

- For employers employing < 50 employees, the requirement to provide a minimum of 1 months’ notice and retrenchment compensation (severance) is to be removed.

- The threshold for negotiating council of trade unions have been reduced from 75% workers as members to 51% of workers.

- Workers may apply to the Industrial Tribunal in case of dispute – 45 days after the application

Why Labour code on Industrial Relations is needed?

- It aims to create greater labour market flexibility and discipline in labour – to improve upon ease of doing business and also to encourage entrepreneurs to engage in labour-intensive sectors. It would replace three laws i.e. Trade Unions Act, 1926; Industrial Employment (Standing Orders) Act, 1946 and the Industrial Disputes Act, 1947.

Labour Code on Social Security & Welfare: Key Provisions

- Definition of employee and categorization of workers covers all kinds of employment including part-time workers, casual workers, fixed term workers, piece rate/ commission rated workers, informal workers, home-based workers, domestic workers and seasonal workers.

- A proper percentage-based structure for contribution, vis-à-vis socio economic category and minimum notified wage, has been put in place under the Code.

- It introduces new approaches to ensure a transparent and fair financial set up, such as,

- Time bound preparation of Accounts within six months of the end of the financial year;

- Provision for social audit of social security schemes by State Boards after every five years;

- Accounts of Intermediate Agencies to be subject to CAG Audit on the same lines as that of Social Security Organizations.

- Wage Ceiling and Income Threshold: The term ‘wage ceiling’ is for the purpose of determining a maximum limit on contribution payable; whereas the term ‘income threshold’ is for the purpose of enabling the government to provide for two different kind of schemes (for same purpose) for two different class of workers.

- Contribution Augmentation Funds would be established through which governments could contribute to the social security in respect of workers who are unable to pay contribution.

- National Stabilization Fund will be used for harmonizing the Scheme Funds across the country and will be managed by the Central Boards.

Why Labour code on Social Security and Welfare is needed?

- Almost 90% of the current workers are not covered under any social security.

- The current thresholds for wage and number of workers employed for a labour law to be applicable creates tenacious incentives for the employers to avoid joining the system which results in exclusions and distortions in the labour market.

Labour Code on Occupational Safety, Health & Working Conditions: Key Provisions

- Centre has been empowered to prescribe standards on occupational safety and health

- Annual health check to be made mandatory in factories and its charge will be borne by the employers

- Appointment letters for all workers (including those employed before this code), underlying their rights to statutory benefits.

- At least 50% of penalty levied on employers could go towards providing some relief to families of workers who die or are seriously injured while working.

- National Occupational Safety and Health Advisory Board at national level and similar bodies at state level, have been proposed to recommend standards on related matters. · Appointment of facilitators with prescribed jurisdiction for inspection, survey, measurement, examination or inquiry has been proposed.

- Mandatory license for every contractor who provides or intends to provide contract labour. Also, license is needed for industrial premises as well.

Why Labour Code on Occupational Safety, Health & Working Conditions, is needed?

- The proposed code is the first single legislation prescribing standards for working conditions, health and safety of workers and it will apply on factories with at least 10 workers.

- It will amalgamate 13 labour laws including the Factories Act, 1948; the Mines Act, 1952; the Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996; the Contract Labour (Regulation and Abolition) Act, 1970 etc.

Issues related to New Labour Code:

- According to Indiaspend’s analysis, the new codes may impact the number of permanent jobs in seasonal factories – which will result in a decline in wages, benefits and work conditions and reduced accountability for companies.

- The report points out that as per the Bills’ fixed-term contracts clause, there will be a reduction in the number of permanent jobs and that the ambiguity on the definition of ‘trade unions’, may lead to diluting working rights.

- With unclear terms for short-term workers, Indiaspend’s report argues that states will have more authority on lay-offs. As per the International Labour Organisation, at least 41 lakh people in the country have lost their jobs while the Centre for Monitoring the Indian Economy (CMIE) estimated 2.1 crore salaried jobs were lost following the lockdown.

- Under the new Industrial Relations Code, a trade union can be deregistered for contravention of unspecified provisions of the code. It simply says that deregistration would follow in case of “contravention by the Trade Union of the provisions of this Code”. The possibility of deregistering a trade union in this unspecified manner shifts the balance completely in favour of employers, who continue to enjoy protection under the Companies Act. This violates the principles of equality before the law and of natural justice.

Way forward

The New Labour Codes try to bring balance between facilitating employment growth and protecting workers rights. The government should address the apprehensions of trade unions give more voice to workers so they can live their life with dignity.

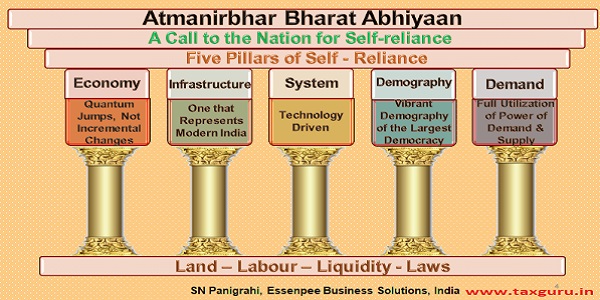

ANALYSIS OF THE AATMA NIRBHAR BHARAT ABHIYAAN

Context:

Emphasising that the special economic package would focus on land, labour, liquidity and laws, PM Modi said it would benefit labourers, farmers, honest tax payers, MSMEs and cottage industry.

Relevance:

GS Paper 3: Indian Economy (issues re: planning, mobilisation of resources, growth, development, employment); Inclusive growth and issues therein.

Mains Questions:

- What is Aatma Nirbhar Bharat Abhiyan? Discuss the focus area under Aatma Nirbhar Bharat Abhiyan. 15 marks

- The Aatma Nirbhar Bharat Abhiyan seeks to increase the borrowing limits of state governments from 3% to 5% of Gross State Domestic Product (GSDP) for the year 2020-21. Discuss the reforms to be implemented by states for increase in borrowing limit. 15 marks

Dimensions of the Topic:

- What is public finance?

- Public finance under Aatma Nirbhar Bharat Abhiyan.

- Issues related to Public finance.

- Way forward

What is Public Finance?

Public finance can be defined as the study of government activities, which may include spending, deficits and taxation. The goals of public finance are to recognize when, how and why the government should intervene in the current economy, and also understand the possible outcomes of making changes in the market.

Public finance under Aatma Nirbhar Bharat Abhiyan:

Borrowing limits: The Scheme seeks to increase the borrowing limits of state governments from 3% to 5% of Gross State Domestic Product (GSDP) for the year 2020-21. This is estimated to give states extra resources of Rs 4.28 lakh crore. Followings Reforms to be implemented by states for increase in borrowing limit:

One nation one ration card:

- Ensuring pan-India availability of food grain entitlements to beneficiaries through portable ration cards and Aadhaar based authentication.

- 24 states and union territories have adopted this reform in 2019-20. This covers 65 crore beneficiaries (80% of the population eligible for entitlements under the National Food Security Act).

Ease of Doing Business:

- Transparency in regulations, permit and inspections. Streamlining of approval, labour regulation and contract enforcement to facilitate ease of doing businesses.

- The central government notified a list of 340 reforms under the Business Reform Action Plan (BRAP) in 2015 which were to be implemented by 2019.

- Ministry of Commerce and Industry releases state-wise rankings based on implementation of these reforms by the states.

Power distribution:

- To replace subsidies given by states with Direct Benefit Transfers (DBT) to safeguard consumer interests while ensuring financial health of the power sector.

Urban local body revenue:

- To promote urban development, health, and sanitation through an improvement in revenue. Proposed means to increase revenue collection include notification of appropriate floor rates (minimum value of a property based on which tax is levied) and water and sewerage charges, to recover operation and maintenance costs.

States such as Telangana and Uttar Pradesh have amended their respective Fiscal Responsibility and Budget Management Acts to raise limits for borrowing to help generate more resources, citing the adverse impact of COVID-19 pandemic and related lockdown on state finances. Both states have increased the limit for fiscal deficit limit from 3 to 5%.The Acts require the state governments to ensure responsible fiscal management and long-term stability.

Disinvestment

Disinvestment means sale or liquidation of assets by the government, usually Central and state public sector enterprises, projects, or other fixed assets. The government undertakes disinvestment to reduce the fiscal burden on the exchequer, or to raise money for meeting specific needs, such as to bridge the revenue shortfall from other regular sources. Main objectives of Disinvestment in India:

- Reducing the fiscal burden on the exchequer

- Improving public finances

- Encouraging private ownership

- Funding growth and development programmes

- Maintaining and promoting competition in the market

A Public Sector Enterprise is defined to include companies and subsidiaries where 51% or more share capital is owned by the central or state governments. As on March 2019, there were 348 central PSEs in India, with a total public investment of Rs 16.4 lakh crore.

The central government has announced that it will notify a new Public Sector Enterprise Policy to privatise all PSEs in non-strategic sectors. In case of strategic sectors, the government will notify a list of sectors which must have at least one PSE (maximum four), alongside the private sector. Other PSEs in these sectors will be privatised, merged, or brought under holding companies (a company with controlling stock of other companies) to minimise administrative costs.

Issues related to public finance in India:

- Increasing Fiscal Deficit: India’s fiscal deficit may touch 9 per cent of GDP in the current fiscal year 2020-21, on the back of the twin issues of revenue loss and higher spending due to the pandemic. It will further increase and create more fiscal burden on the government.

- Increasing interest rate and reducing private investment: When the government borrows a lot from public savings, it pushes out the private sector, which also needs to borrow in order to run businesses. Then begins a competition between the government and the private sector, pushing up the interest rates on loans.

- Punishing next generation: Higher borrowing today means a greater pay out of taxes in the future, which punishes the next generation.

- Increasing Current Account deficit: A high fiscal deficit also triggers the possibility of current account deficit (the shortfall between a country’s exports and imports) and raises public debt and inflation.

- Negative impact on Credit Rating: Global investors and rating agencies keep an eye on the fiscal deficit. Investors also monitor this sacrosanct figure as they use it to judge the health of the economy before making any investment decision.

Way forward

The Aatma Nirbhar Bharat Abhiyan will create fiscal constraints upon the central and state governments which further will increase the fiscal deficit. However, if this extra borrowing will utilised and focus more on physical and social capital formation then it will create demand in economy and bring virtuous cycle.

Background:

The Fiscal Responsibility and Budget Management (FRBM) Act

Objectives of FRBM Act:

The primary objective was the elimination of revenue deficit and bringing down the fiscal deficit. The other objectives included:

- Introduction of a transparent system of fiscal management within the country

- Ensuring equitable distribution of debt over the years

- Ensuring fiscal stability in the long run

The act also intended to give the required flexibility to the Central Bank for managing inflation in India.

Features of the FRBM Act:

It was mandated by the act that the following must be placed along with the Budget documents annually in the Parliament:

- Macroeconomic Framework Statement

- Medium Term Fiscal Policy Statement and

- Fiscal Policy Strategy Statement

It was proposed that the four fiscal indicators i.e., revenue deficit as a percentage of GDP, fiscal deficit as a percentage of GDP, tax revenue as a percentage of GDP, and total outstanding liabilities as a percentage of GDP be projected in the medium-term fiscal policy statement.

Targets and fiscal indicators as per the FRBM Ac:

The central government agreed to the following fiscal indicators and targets, after the enactment of the FRBMA

- Revenue deficit to be eliminated by the 31st of March 2009. A minimum annual reduction of 0.5% of GDP.

- Fiscal Deficit to be brought down to at least 3% of GDP by 31st of March 2008. A minimum annual reduction – 0.3% of GDP.

- Total Debt to be reduced to 9% of the GDP (a target increased from the original 6% requirement in 2004–05). An annual reduction of – 1% of GDP.

The purchase of government bonds by RBI must cease from 1 April 2006.