Content:

- Editorial: Oxygen for fiscal federalism

Oxygen for fiscal federalism: On GST Compensation

Context:

- At the time of introducing the new indirect tax regime, the Goods and Services Tax (GST) law assured States a 14% increase in their annual revenue for five years (up to July 1, 2020).

- But the Union government has deviated from the statutory promise and has been insisting that States avail themselves of loans.

Relevance:

- GS Paper 3: Indian Economy and issues relating to Planning, Mobilization of Resources, Growth, Development and Employment.

Mains Questions:

- A special rate could be levied to the States to enable them to raise more resources during the pandemic. Discuss 15 Marks

Dimensions of the Article:

- What is GST Compensation Cess and the tussle over it?

- What is State’s stance on the issue?

- What is Centre’s stance on the issue?

- Way forward

What is GST Compensation Cess and the tussle over it?

GST was implemented through the GST (101st Amendment Act), 2016 as a long pending indirect tax reform. It is a single tax that replaces multiple other indirect taxes. The Centre lost out on its power to levy taxes such as excise duty, while the States could no longer levy entry tax, VAT etc. To allay the fears of States regarding loss of revenue, following mechanism was made:

- GST (Compensation to States) Act, 2017 was enacted:

- Under the Act, the percentage of annual revenue growth of a State has been projected to be 14%. If the annual revenue growth of a State is less than 14%, the State is entitled to receive compensation under the statute.

- The compensation payable to a State shall be provisionally calculated and released at the end of every two months period.

- The generation of revenue under the Act would happen through a GST Compensation Cess:

- The cess comprises the cess levied on sin and luxury goods for five years.

- The entire cess collected during the year is required to be credited to a non-lapsable Fund (the GST Compensation Cess Fund).

- The collected compensation cess flows into the CFI and is then transferred to the Public Account of India, where the GST compensation cess fund has been created.

The issue arose when payments due for August-September 2019 were delayed. Since then, all subsequent payouts have seen cascading delays. The problem has aggravated and further compounded due to following reasons:

- Persistent Economic Slowdown: The slowdown has impacted the demand and consumption levels and has thus dented the overall GST collections (both Centre and States).

- Effect of the Pandemic: The pandemic has given an economic shock to the Indian Economy which has dented the tax collection expectations (including the collections from GST Compensation Cess) of both Centre and States.

- Estimation of 14% revenue growth unrealistic: The high rate of 14%, which has compounded since 2015- 16, has been seen as delinked from economic realities. In the initial meetings of the GST Council, a revenue growth rate of 10.6% (the average all-India growth rate in the three years preceding 2015-16) was proposed but 14% revenue growth was accepted “in the spirit of compromise”.

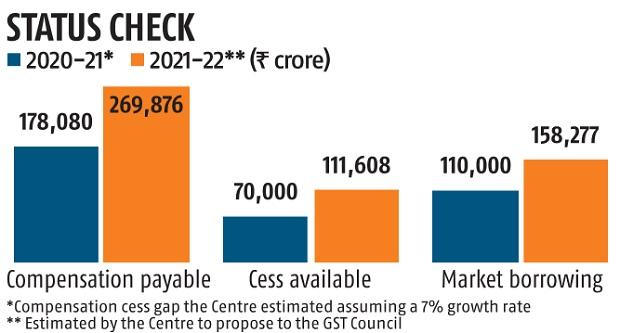

As a result of these issues, the stalemate reached at a point where States were looking at the GST shortfall of Rs. 30,000 crore and the Centre being in no position to provide for it.

What is State’s stance on the issue?

Since the GST Compensation acts as a harbinger of State’s trust on Centre, non-compliance on this agreement has the potential to erode the trust between the Centre-State relationship. In this context, several States have expressed following issues:

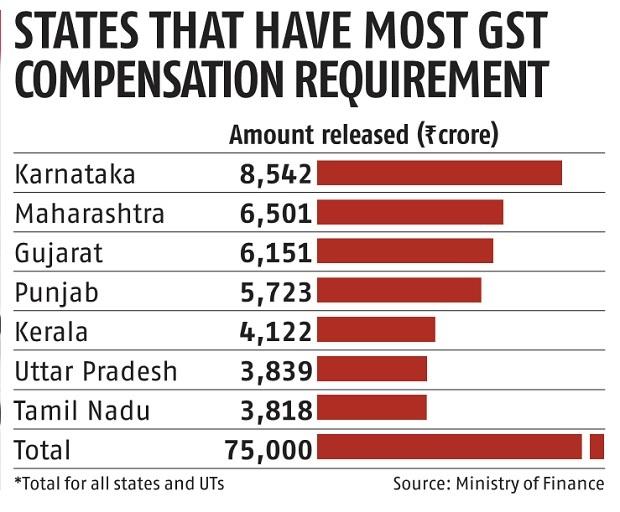

- Centre not honoring its moral and legal obligation: Finance Ministers of both Kerala and Punjab have argued that the Central Government has a legal, and a moral obligation to compensate the State Governments for the revenue shortfall. A deadlock so early in the implementation of GST has made States skeptical about the future of Fiscal Federalism.

- Ineffectiveness of the GST Council: Any dispute regarding GST is to be handled by the GST Council but in the recently concluded 39th GST Council meeting, no steps were taken to create such a dispute resolution mechanism. With a 1/3rd voting power, the Centre has a virtual veto over the decision making in the council (since 3/4th majority is needed to pass a decision). This has made the States question the functioning structure of the Council itself.

- Resort to legal proceedings: In the absence of an alternate remedy, the only option left for states like Kerala and Punjab is to approach the Supreme Court under Article 131 of the Constitution. Such a judicial remedy to establish fiscal federalism of the states would erode even the limited institutional capital present between Centre and States.

What is Centre’s stance on the issue?

The stand of the Centre on these issues is not based solely on the response to the States but in the background of low economic growth and negative tax buoyancy rates (percentage change in tax revenue to percentage change in GDP) which is in addition to almost 25% reduction in collection of Corporate taxes. In this background, the Centre has taken following stands:

- The Centre has refused to compensate the States immediately but has provided the States with two options (to make good either the shortfall in compensation arising from GST implementation or the overall shortfall).

- Option 1: It offered states to borrow the shortfall arising out of GST implementation, to be borrowed through issue of debt under a special window coordinated by the Ministry of Finance. The option is to ensure steady flow of resources similar to the flow under GST compensation on a bi-monthly basis.

- Option 2: It has offered the states to borrow the entire compensation shortfall (including the COVID impact portion) through issue of market debt. The states will not be required to repay the principal from any other source. However, the interest shall be paid by the states from their own resources.

- The Centre has alongside contended that the revenue shortfall is on account of the COVID-19 pandemic, which is an ‘Act of God’, stating that it has no legal obligation to compensate the States in this scenario.

- It has also argued that the inflows to the GST Compensation Fund are to be made from the GST Compensation Cess and if that is inadequate, the Centre is not obligated to supplement it by diverting flows from other sources.

Way forward

- Rebuilding institutional capital to soothe the Centre-State relationship: Efforts could be made rejuvenate and rekindle the Inter-State Council as the body not only has constitutional backing but its mandate and nature of participation is ideally suited for a larger federal role. o Alongside the Inter-State Council, efforts could be made to increase political capital through institutions like Chief Minister’s Conference.

- Widening the ambit of GST for revenue augmentation: The current coverage of GST excludes electricity, petrol, diesel and real estate, as also agriculture. Widening the ambit of GST could provide a larger base for taxation in the long run.

- Structural reforms: The augmentation of revenue in the long-term will require structural reforms like reviewing of GST on continuous basis and increasing tax compliance.

- Increasing transparency in Fiscal management: Increasing transparency in areas like working of GST Council, adhering to the procedure established by the GST Compensation Act, and decreasing over-reliance on cesses and surcharges could repose the lost faith of States in Centre’s Fiscal Management