CONTENTS

- Insuring the Future

- How is India Planning to Boost EV Production?

Insuring the Future

Context:

The Insurance Regulatory and Development Authority of India (IRDAI), as the principal overseer of insurance products, has issued a directive aimed at fostering inclusivity within health insurance coverage, particularly emphasizing the need to extend benefits to a broader spectrum of citizens.

Relevance:

GS3-

- Mobilization of Resources

- Capital Market

Mains Question:

The Insurance Regulatory and Development Authority of India (IRDAI) has issued a directive aimed at extending the benefits of insurance to a broader spectrum of citizens. However, there is an even pressing need to make health insurance truly affordable. Comment. (15 Marks, 250 Words).

More on the Directive:

Notably, the directive mandates insurance providers to extend health insurance offerings to senior citizens, a demographic currently excluded as individuals aged 65 and above are unable to procure new policies for themselves. This directive underscores a recognition of the ongoing demographic shifts occurring within India.

Other Significant Developments:

- IRDAI recently unveiled its preliminary draft of the Rural, Social Sector, and Motor Third Party Obligations Regulations for the year 2024.

- In a move aimed at expanding insurance coverage nationwide, IRDAI has proposed mandatory insurance coverage in all gram panchayats across India, mandated by insurance companies to fulfil the goal of universal insurance access.

- Additionally, IRDAI has eliminated the age restriction for purchasing health insurance policies, effective from April 1, 2024.

- The year 2023 saw a concerted effort within the insurance industry towards consolidation, accompanied by a focused push for reforms and technological advancement, all with the overarching aim of achieving universal insurance coverage by the year 2047.

Insurance Sector in India:

- India’s insurance sector stands out as one of the premier industries witnessing significant upward momentum.

- Positioned as the fifth largest market globally among emerging insurance markets, India demonstrates robust growth, averaging between 32-34% annually.

- The landscape comprises 57 insurance entities, with 24 dedicated to life insurance and 34 engaged in non-life insurance activities.

- Notably, the Life Insurance Corporation (LIC) represents the solitary public sector entity among life insurers, while the non-life segment includes six public sector insurers.

- According to the Economic Survey for the period 2022-23, India’s insurance market is positioned to become one of the fastest-growing globally over the next decade.

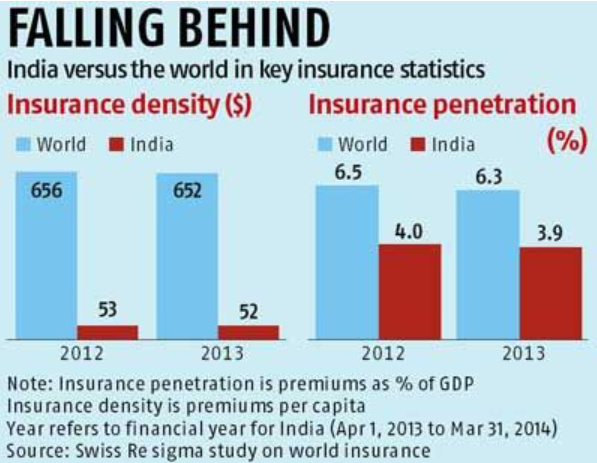

- Data from the Insurance Regulatory and Development Authority of India (IRDAI) indicates that insurance penetration in India rose from 3.76% in 2019-20 to 4.20% in 2020-21, marking an increase of 11.70%.

- Furthermore, insurance density escalated from USD 78 in 2020-21 to USD 91 in 2021-22.

- In terms of life insurance penetration, the figure stood at 3.2% in 2021, nearly twice the rate observed in emerging markets and marginally surpassing the global average.

- In terms of oversight and governance, the Insurance Regulatory and Development Authority of India (IRDAI) serves as the pivotal regulatory body responsible for the supervision and regulation of the insurance sector.

Insurance Regulatory and Development Authority of India (IRDAI):

- The Insurance Regulatory and Development Authority of India (IRDAI) was established as a statutory entity through the enactment of the Insurance Regulatory and Development Authority Act of 1999.

- Functioning as an autonomous body, its primary responsibility lies in the regulation and oversight of the insurance sector’s growth within India.

- Its core functions encompass safeguarding the rights and interests of policyholders on various fronts, including policy assignment, nomination procedures, determination of insurable interests, resolution of insurance claims, evaluation of policy surrender values, and ensuring adherence to terms and conditions outlined in insurance contracts.

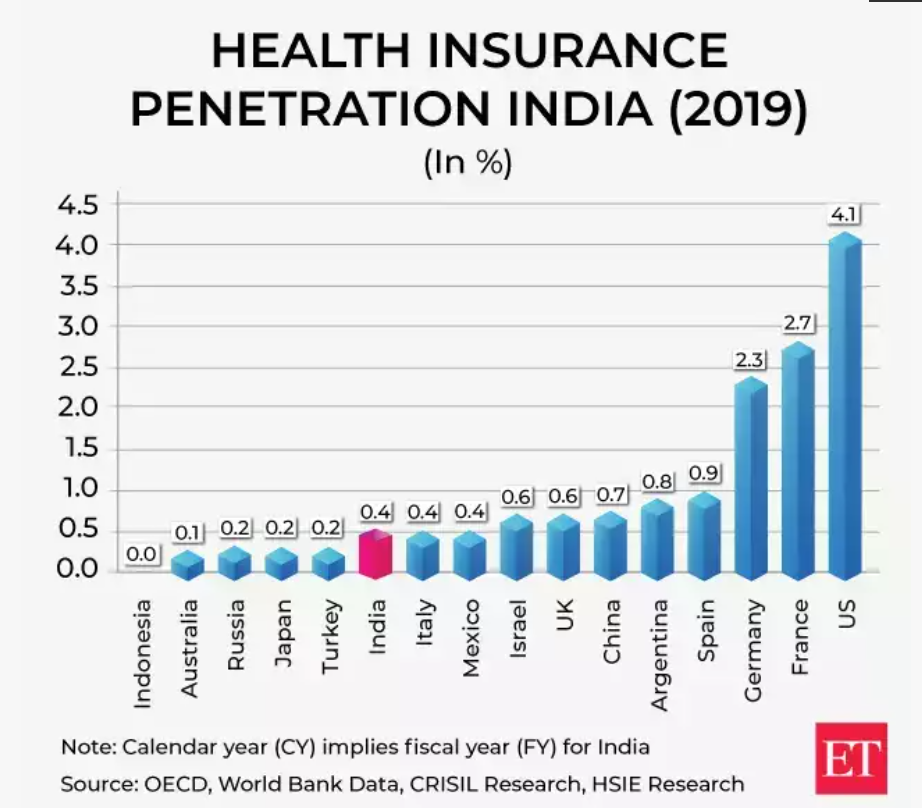

Elderly Population Needs and Insurance Coverage:

- Although official population statistics for India have not been updated since 2011, estimates provided by the UN Population Fund and experts suggest that India’s population is nearing parity with China’s and might have even surpassed it by 2023.

- According to projections outlined in the India Ageing Report, 2023, extrapolated from UN data, the cohort of seniors in India—those aged 60 and above—is projected to escalate from approximately 10% of the population (149 million in 2022) to a staggering 30% (347 million) by 2050, surpassing the current population of the United States.

- Comparatively, several highly developed nations already contend with significant proportions of elderly citizens (aged 65 and above), ranging from 16% to 28% of their populations.

- This demographic trend has sparked substantial concerns within these societies regarding access to healthcare, affordable medications, and the adequacy of caregiving infrastructure to support senior citizens.

- While some of these economically advanced countries boast publicly funded healthcare systems, others rely entirely on private healthcare, where the cost serves as a significant determinant of access to quality care.

Associated Concerns:

- In many of these nations, there are minimal barriers to entry for health insurance policies. However, adhering to long-standing principles of actuarial economics, health insurance premiums tend to escalate progressively, and at times exponentially, with advancing age.

- Even now, only a small fraction of India’s economic elite, constituting single-digit percentages, can afford comprehensive “family floater” plans that cover both individuals and their parents at a cost lower than what standalone senior-citizen health insurance would entail.

- If the sole outcome of the recent circular issued by the IRDA is to inundate the market with numerous unaffordable health insurance policies, it would be akin to admiring the icing on an inedible cake.

- There has been significant emphasis placed on the critical importance of the next two decades for India’s future, predicated on the notion that this period represents the window during which India must leverage its ‘demographic dividend’.

Conclusion:

This concept rests on the assumption that a substantial portion of the workforce will transition away from agriculture, inevitably leading to a breakdown in the traditional caregiving structure for the elderly. The experiences observed in various southern Indian states serve as poignant examples of this trend. Therefore, while expanding the eligibility criteria for health insurance is essential, it must be accompanied by a massive overhaul and enhancement of affordable healthcare services.

How is India Planning to Boost EV Production?

Context:

On March 15, the Union government sanctioned a pivotal policy aimed at positioning India as a manufacturing powerhouse for Electric Vehicles (EVs), with a minimum investment threshold set at ₹4,150 crore. This policy heralds a new era, paving the way for renowned global EV manufacturers such as Tesla and Chinese giant BYD to venture into the Indian market.

Relevance:

GS2-

Government Policies and Interventions

GS3-

- Achievements of Indians in Science and Technology

- Mobilization of Resources

Mains Question:

The Union government recently sanctioned a policy aimed at positioning India as a manufacturing powerhouse for Electric Vehicles (EVs). In this context, discuss the details of this policy while suggesting a way forward strategy to further upscale electric vehicle adoption. (15 Marks, 250 Words).

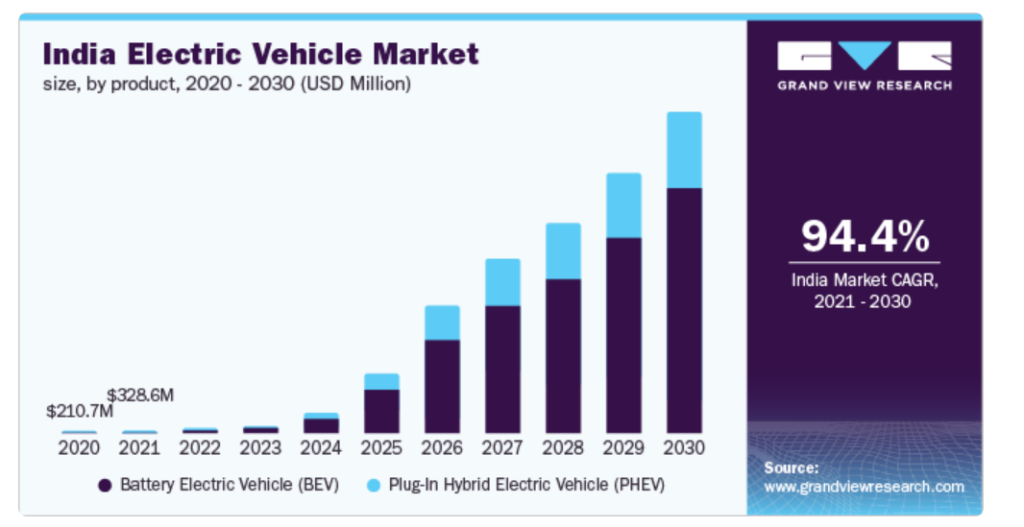

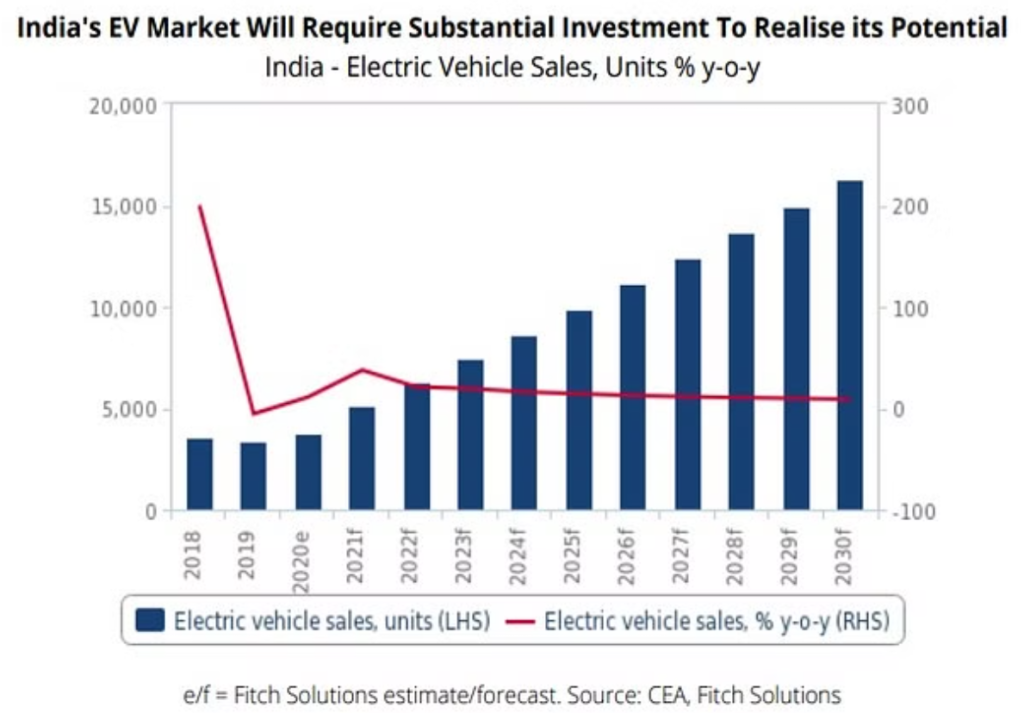

EV Market in India:

More on the Policy:

At the heart of this policy lies a strategic objective: to facilitate a seamless transition towards localized EV production in a financially sustainable manner, aligning with local market dynamics and consumer demand.

Reduction in Import Duties:

- Notably, a significant provision of this policy entails a substantial reduction in import duties on electric vehicles brought in as Completely Built Units (CBUs) with a minimum Cost, Insurance, and Freight (CIF) value of $35,000.

- Over a five-year period, the import duty is slashed from the current 70%-100% to a mere 15%, contingent upon the establishment of a manufacturing unit within three years.

Incentivization:

- Furthermore, the policy offers a lucrative incentive by waiving a total duty amounting to ₹6,484 crore or a sum commensurate with the investment made, whichever is lower, on the total quantity of EVs imported.

- However, this scheme imposes a cap of 40,000 EV imports, not exceeding 8,000 units annually, provided that the minimum investment threshold of $800 million is met.

Localization Targets:

- Another crucial facet of this initiative pertains to localization targets. Manufacturers are granted a three-year window to establish their production facilities within India.

- They are expected to achieve a localization level of 25% by the third year of incentivized operation, escalating to 50% by the fifth year.

- Failure to meet these localization targets, coupled with the inability to fulfil the stipulated minimum investment criteria, will result in the revocation of manufacturers’ bank guarantees.

What about the Local Industry Participants?

- In December 2023, Tata Motors, as reported by Reuters, voiced opposition to the proposal put forth by Tesla. Tata Motors contended that reducing duties would adversely impact the domestic industry and potentially disrupt the investment climate.

- Currently, most Indian players excel in segments priced below ₹29 lakh. Consequently, the benefits of this policy, particularly the reduction in import duties to 15%, are likely to accrue primarily to Original Equipment Manufacturers (OEMs) catering to consumers in the higher-end market segments.

- Additionally, the policy incentivizes global EV manufacturers and Indian joint ventures with such entities to expand their sales and manufacturing operations within India.

How does the Policy Address the Needs of the Indian Market?

- A Distinguished Fellow at The Energy and Resources Institute (TERI), emphasizes that global players venturing into the Indian market must take into account local factors such as environmental conditions, road infrastructure, and usage patterns.

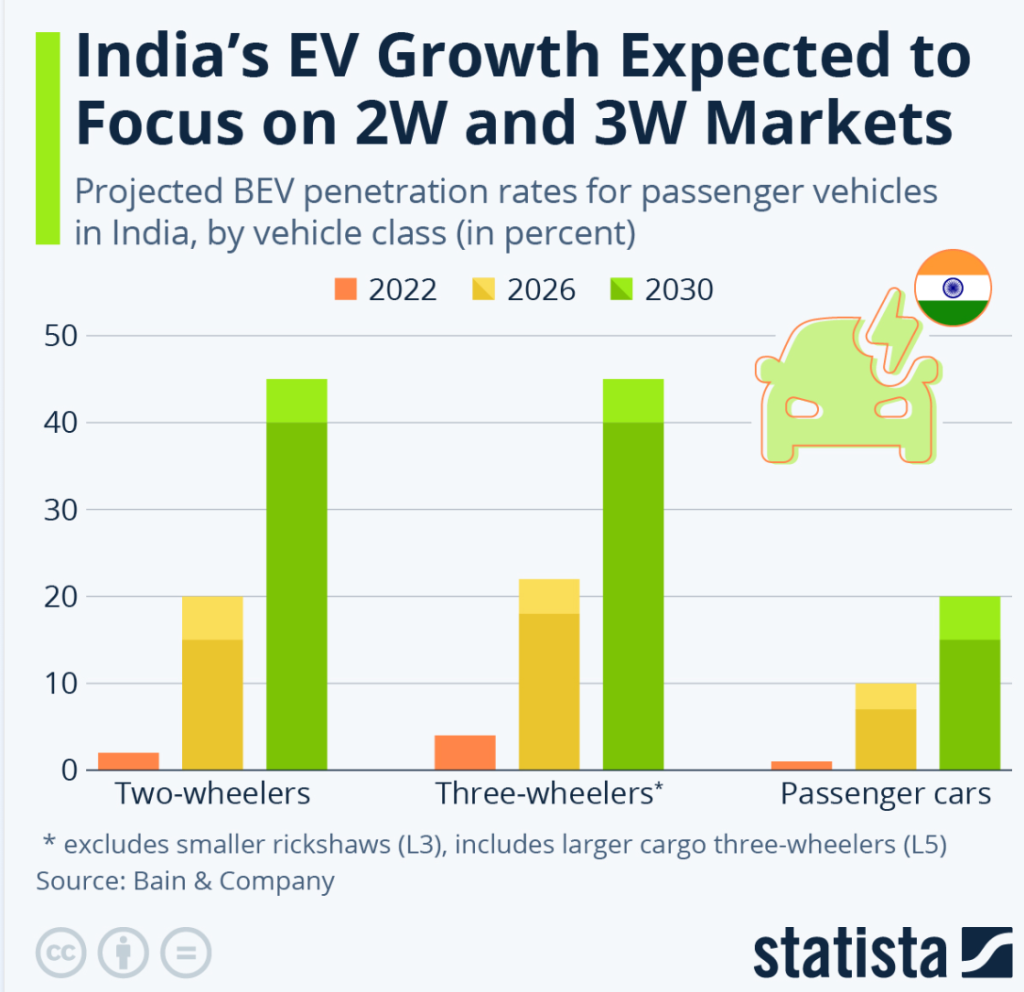

- While there has been substantial penetration in the two and three-wheeler segments, the contribution from passenger vehicles remains modest at 2.2% thus far.

- This is majorly due to challenges such as inadequate charging infrastructure, concerns about range limitations, and a limited selection of affordable EV models due to insufficient localization efforts.

- The Confederation of Indian Industry (CII), in a report from July 2023, projected that India may require a minimum of 13 lakh charging stations by 2030 to facilitate the anticipated surge in EV adoption.

- A retired professor from the Institute for Studies in Industrial Development, elaborates on the necessity of building a robust EV ecosystem capable of ensuring the reliability and durability of components, as well as providing comprehensive service support.

- A policy shift towards a 21st-century paradigm that prioritizes not only competitive products but also sustainability is the need of the hour. The focus should be on tailoring product and system designs, as well as business portfolios, to align with domestic demand, with exports following suit.

- The importance of leveraging appropriate product and system designs, especially in the context of two-wheelers, three-wheelers, and four-wheelers, to guide policies like the Production-Linked Incentive (PLI) needs to be stressed on.

Conclusion:

Foreign capital alone is not the way out and there is a need for Indian manufacturers to be steered in the right direction. The comprehensive policy framework, as seen above, underscores the government’s concerted efforts to foster a robust EV ecosystem and drive sustainable growth in the sector.