Context:

Analysis said that IT markets are picking up to such a degree that both the U.S. and Europe are running out of critical skills, and with this, offshore and Indian alternatives are increasingly becoming attractive for tech buyers.

Relevance:

GS-III: Industry and Infrastructure (IT Sector), Indian Economy

Dimensions of the Article:

- About the attractiveness of the Indian Offshore model

- Service Sector boom in India

- Has the growth in service sector ensured adequate employment opportunities?

About the attractiveness of the Indian Offshore model

- Typically, offshore accounts for 70-80% of a project while onshore is in the 20-30% range. In the COVID-19 era, markets are seeing a clear 50% reduction in onshore and 5-15% rise in offshore share.

- For all IT work conducted remotely, it makes perfect sense to run it from India and the Indian model will dominate the IT service scene for at least another decade.

- Offshore providers have ended up being ‘pandemic winners’, seeing quantum growth in revenues and substantial decline in operational cost after the WFH trend kicked in.

- In addition to the skills shortage, the pandemic-induced work-from-home has further raised the openness of global tech buyers to working in a distributed environment, away from onshore (or the client’s location).

- There is now some of the most aggressive pricing ever as an impact of the pandemic, with some deals priced as low as $4-6 per hour for IT and business process work.

Service Sector boom in India

- India’s economic growth since the 1990s has largely been on account of an expansion of the services sector, in which exports are seen as having played an important role.

- The rise in the share of services in GDP was particularly sharp after 1996-97.

- In the event, services as a group came to dominate the Indian economy, accounting for more than half its GDP.

- The Economic Survey 2013-14 noted that India has the second fastest growing services sector with CAGR (compound annual growth rate) at 9%, just below China’s 10.9%, during the last 11-year period from 2001 to 2012.

- This trend has continued which is shown by gross value added (GVA) from services growing at 8.7% per annum and accounted for 58% of the increase in total GVA between 2011-12 and 2016-17.

- This growth in services has also been accompanied by a significant increase in the exports of services.

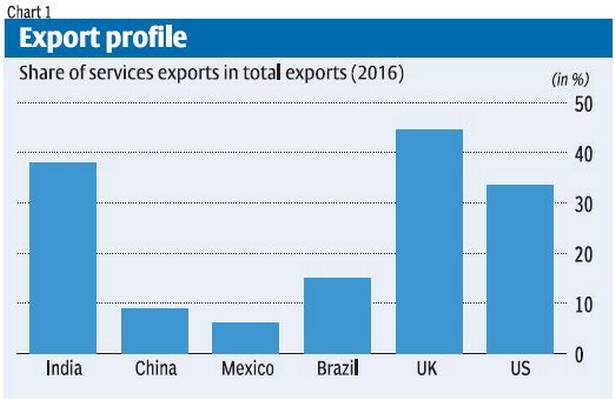

- India’s success in the services exports area has meant that its share of services in total exports (38%) is much higher than in countries such as China, Mexico and Brazil and close to ratios in the UK and the US.

Has the growth in service sector ensured adequate employment opportunities?

- Despite the presence of unorganised services, the share of the services sector in total employment was relatively low.

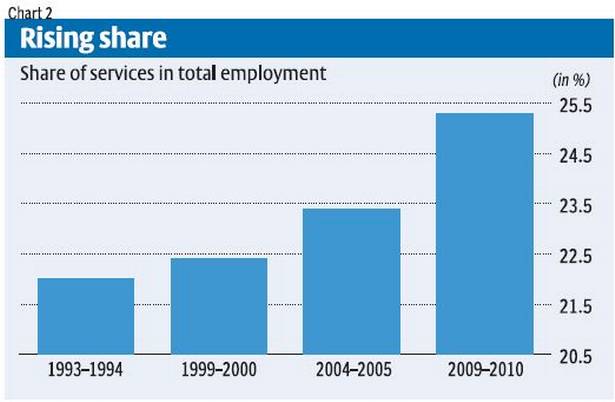

- Between 1999-00 and 2004-05, employment in the tertiary sector increased by only 22%, whereas GDP at constant prices contributed by the services sector expanded by 44%.

- Tertiary sector employment in 2009-10 amounted to only 25% of the work force, despite the fact that around 55% of GDP came from this sector.

- Also, NSSO reveals that the share of services in employment increased by far less than the huge increase in its share in GDP.

- India is also unusual in terms of the wide divergence of the shares of the services sector in total gross value added and employment.

- The GVA and employment shares in India were 53 and 29%, as compared with 50 and 42% in China, 60 and 61% in Mexico, and 72 and 69% in Brazil.

- The Economic Survey 2016-17 says that among the top 15 services producer countries, India has the lowest share (28.6%) of total employment in 2016.

-Source: The Hindu