Context:

Moody’s Investors Service said that India’s public debt level is among the highest in emerging economies with a quantitative easing programme underway, while its debt affordability is among the weakest.

Relevance:

GS-III: Indian Economy (Economic Growth and Development in India)

Dimensions of the Article:

- What are Emerging markets/economies?

- What is Public Debt?

- Is Public Debt good or bad?

- Trends in India’s Public Debt

- Highlights of Moody’s report

What are Emerging markets/economies?

- An emerging market/country/economy is a market that has some characteristics of a developed market, but does not fully meet its standards.

- This includes markets that may become developed markets in the future or were in the past.

- The nine largest emerging and developing economies by either nominal or PPP-adjusted GDP are 4 of the 5 BRICS countries (Brazil, Russia, India and China) along with Indonesia, South Korea, Mexico, Saudi Arabia and Turkey.

What is Public Debt?

- The public debt is how much a country owes to lenders outside of itself.

- The term “public debt” is often used interchangeably with the term sovereign debt and these lenders to the country can include individuals, businesses, and even other governments.

- Public debt usually only refers to national debt and it is the accumulation of annual budget deficits (A nation’s deficit affects its debt and vice-versa).

- Also, if interest rates go up on the public debt, they will also rise for all private debt.

- Public debt is different from External debt – External Debt is the amount owed to foreign investors by both the government and the private sector and Public debt does impact external debt.

Is Public Debt good or bad?

- In the short run, public debt is a good way for countries to get extra funds to invest in their economic growth.

- Public debt is a safe way for foreigners to invest in a country’s growth by buying government bonds – much safer than Foreign Direct Investment.

- However, when Governments tend to take on too much debt because the benefits are making them popular with voters, investors usually start demanding a higher interest rate (wanting more return for the greater risk as the country is more likely to default on its debt).

- If the country keeps spending by borrowing, then its bonds will lose their value and ratings and as interest rates rise, it becomes more expensive for a country to refinance its existing debt. In time, income has to go toward debt repayment, and less toward government services.

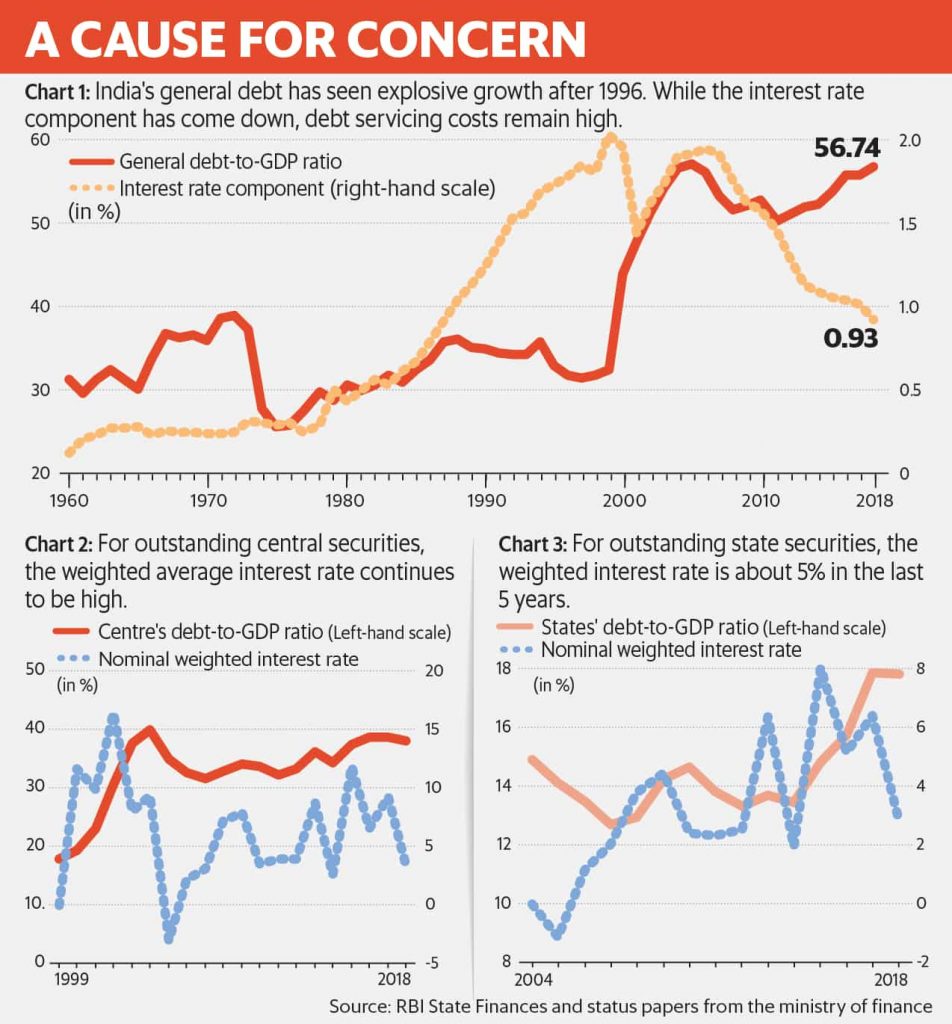

Trends in India’s Public Debt

- Till 1972, India’s general debt—for the Centre and states—rose steadily to about 39% of gross domestic product (GDP) and then fell sharply in 1974.

- After 1996, it saw explosive growth, reaching 57% in 2005.

- In 2018, general debt was approximately 57% of GDP.

Should India be worried?

- A 2020 research paper argues that the pandemic has depressed real interest rates despite ballooning government debts in the industrial world.

- Lower interest rates mean countries are less constrained by fiscal space.

- Large fiscal expansions can thus improve fiscal sustainability by raising GDP more than they raise debt and interest payments.

- For example: Despite a ballooning US federal debt/GDP ratio from below 50% in 2000 to about 100% in 2020, federal interest payments in the US as a percentage of GDP in the last 10 years have hovered between 1% and 2%.

- In simple words: in a world of low interest rates, advanced economies can run limited primary deficits and still keep their public debt stable.

- However, because interest rates are falling, this does not mean that debt servicing costs are going down due to rising debt.

- Also, high levels of public debt in India have historically been associated with fiscal dominance, and more uncertainty and volatility in the economy. Therefore, there are good reasons for India to worry about its public debt.

Highlights of Moody’s report

- Most of the 11 emerging markets, except Chile, have weak government effectiveness, suggesting potential risks executing fiscal reforms or consolidation plans.

- Debt affordability varies widely, with Ghana and India rated the weakest.

- With the exception of the Philippines, Indonesia and Ghana, most emerging market central banks have not yet announced maximum purchases nor a clear time frame for their programs, hence, there is a risk that central banks will not taper these programs once they fulfil their primary objectives unless they are supported by strong fiscal policy frameworks.

- The report warned that depending on recovery prospects and future debt servicing costs, high debt levels may become unsustainable for the more vulnerable economies.

-Source: The Hindu, Livemint