RBI’s measures to tackle COVID-19

The measures taken by RBI have four objectives in mind. These are aimed to maintain adequate liquidity in the system and its constituents, to facilitate and incentivize bank credit flows, to de-stress and enable performance of markets.

Important graphs to correlate with RBI Measures for UPSC exam

Targeted Long-Term Repo Operations (TLTROs)

TLTRO 2.0 (April 2020)

TLTRO 2.0 of ₹50,000 crore is to ensure that different segments of financial markets such as non-banking financial companies (NBFCs) and microfinance institutions (MFIs) get enough liquidity. At least 50% of amount availed by banks must go to mid and small sized NBFCs and MFIs

The funds will have to be made in bonds, Commercial Papers, Non-Convertible Debentures of NBFCs with 50% of it going to small and mid-sized NBFC within one month of availing the credit from RBI.

The reason behind targeting the NBFCs was that the funds raised via TLTRO 1.0 have been parked in issue of public banks and big corporates. NBFCs were finding hard to raise money.

TLTRO 1.0 (March 2020)

Reserve Bank had announced to conduct auctions of targeted long-term repos of up to three years tenor of appropriate sizes for a total amount of up to Rs 1,00,000 crore at a floating rate linked to the policy repo rate. Liquidity availed by banks under TLTROs should be deployed in investment grade corporate bonds, commercial paper, and non convertible debentures over and above the outstanding level of their investments in these bonds as on March 27, 2020.

Cash Reserve Ratio (CRR) (March 2020)

- CRR requirement of banks was reduced by 100 bps from 4 per cent of NDTL to 3 per cent effective fortnight beginning March 28, 2020, which would augment primary liquidity in the banking system by about Rs 1,37,000 crore. This dispensation will be available for a period of one year ending March 26, 2021.

- RBI announced measures that the minimum daily CRR balance requirement was reduced from 90 per cent to 80 per cent effective from the first day of the fortnight beginning March 28, 2020. This dispensation will be available up to June 26, 2020.

Marginal Standing Facility (MSF) (March 2020)

In view of the exceptionally high volatility in domestic financial markets and to provide comfort to the banking system, banks’ limit for borrowing overnight under the MSF by dipping into their Statutory Liquidity Ratio (SLR) were raised to 3 per cent of NDTL from 2 per cent.

This measure announced by RBI will allow the banking system to avail an additional Rs 1,37,000 crore of liquidity under the liquidity adjustment facility (LAF) window at the reduced MSF rate of 4.65 per cent.

Reduction in Policy Rate and Widening of the Policy Corridor

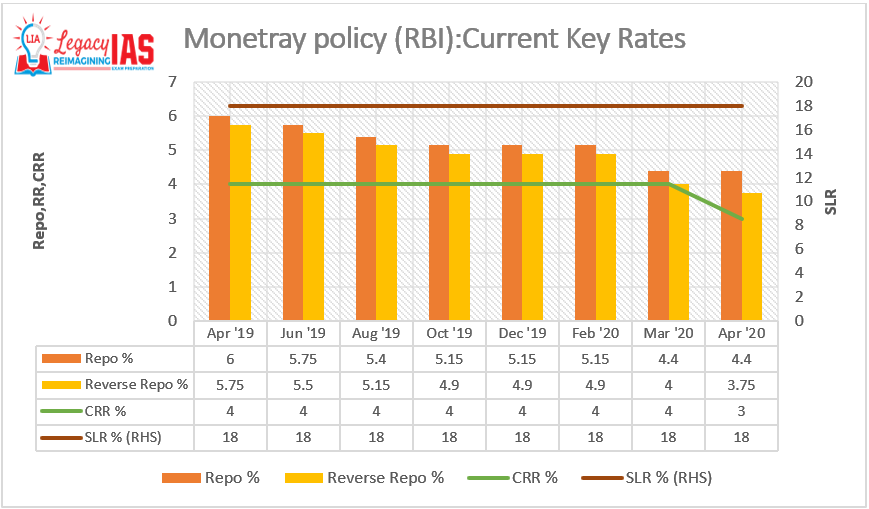

- March 2020: The policy repo rate under the LAF was reduced by 75 basis points to 4.40 per cent from 5.15 per cent in March 2020. Accordingly, RBI announced measures that the MSF rate and the Bank Rate were reduced to 4.65 per cent from 5.40 per cent.

- March 2020: In view of persistent excess liquidity, the existing LAF corridor was widened asymmetrically to 65 bps from 50 bps. Accordingly, the reverse repo rate was reduced by 90 bps from 4.90 per cent to 4.00 per cent. The purpose of this measure was to make it relatively unattractive for banks to passively deposit funds with the RBI; instead, these funds should be deployed for on-lending to productive sectors of the economy.

- April 2020: The Reserve Bank of India cut the reverse repo rate by 25 basis points to 3.75% even as it kept the repo rate unchanged at 4.4%.

Thus, the reverse repo rate is now 65 bps lower than the policy repo rate while the MSF rate continues to be 25 bps above the policy repo rate.

BACK TO BASICS

QUANTITATIVE TOOLS

Cash reserve Ratio (3% since March 2020)

- Scheduled Banks (under RBI act) and Non-scheduled Co-operative banks (Banking regulation act) have to hold a percentage of NDTL as cash

- CRR has been reduced over the years, thanks to Narasimhan committee I. However, it was increased during the Sub-prime crisis (2009-10)

- Also, the ceiling and floor have been removed in 2007(even for SLR)

This was fixed to be in the range of 3 to 15 per cent. A recent Amendment (2007) has removed the 3 per cent floor and provided a free hand to the RBI in fixing the CRR.

Following the recommendations of the Narasimhan Committee on the Financial System (1991) the government started two major changes concerning the CRR:

- Reducing the CRR was set as the medium-term objective and it was reduced gradually from its peak of 15 per cent in 1992

- Since 2006 the RBI can prescribe CRR for scheduled banks without any floor or ceiling rate

- Payment of interest by the RBI on the CRR discontinued from mid-2007.

Statutory liquidity ratio(18%)

- Percentage of NDTL in the form of cash, gold, RBI approved securities (G-sec, T-bill, PSU-debentures) i.e Liquid assets

- Again, under Banking regulation act

- Some profit can be earned because liquidation of these assets can earn something

- All commercial banks except PACS and among NBFCs, only deposit taking ones, need to maintain SLR

- The Government of India has removed the 25 per cent floor for the SLR

CRR dnd SLR are used by RBI to control multiplier effect, manage bank run situations and unexpected demands. The ratios have to be maintained with a lag of one fortnight

When the reserve ratios are too high, the banks lend at a higher rate (including spread). Such dear lending would make business expansions and investments costlier. A possible consequence would be low employment, lower tax to GDP ratio causing FD to go up and weakening BoP in the longer run.

Open market operations

Being the debt manager of the Govt, the RBI auctions the G-secs and T-bills upto 364 days. When it is unable to sell the requisite G-secs, the RBI itself purchases them, thus accumulating G-secs with itself. When the need be, the RBI puts these securities on sale to banks, which are always keen to invest. This leads to lower money supply.

They are conducted by the RBI by way of sale or purchase of government securities (g-secs) to adjust money supply conditions.

- The central bank sells g-secs to suck out liquidity from the system and buys back g-secs to infuse liquidity into the system.

- These operations are often conducted on a day-to-day basis in a manner that balances inflation while helping banks continue to lend.

- The RBI uses OMO along with other monetary policy tools such as repo rate, cash reserve ratio and statutory liquidity ratio to adjust the quantum and price of money in the system.

- When the RBI wants to increase the money supply in the economy, it purchases the government securities from the market and it sells government securities to suck out liquidity from the system.

- RBI carries out the OMO through commercial banks and does not directly deal with the public.

Market stabilization scheme

If the RBI does not have enough G-secs to absorb liquidity, it would be difficult to tackle money supply. Hence, RBI and the government have an agreement according to which the RBI can issue G-secs with 2-year maturity, T-bills with 364 days maturity and CMBs with 90 days maturity. This means, even if the Govt is not willing to borrow, the RBI can go ahead with issuance of such securities upto 30k cr. (Govt pays the interest here as well)

OMOs are used either to increase or reduce liquidity. But MSS is only to reduce liquidity.

Rates

Bank rate (4.65% April 2020)

It is the rate at which Long term lending is done by RBI

- No collateral is required

- Not used as policy rate anymore

- Used as a base for penalty rate(bank rate plus 3%-5%), if banks don’t maintain CRR/SLR

- The clients who borrow through this route are the Government of India, state governments, banks, financial institutions, co-operative banks, NBFCs, etc.

- The rate has direct impact on long-term lending activities of the concerned lending bodies operating in the Indian financial system.

Liquidity Adjustment facility (LAF)- Repo rate (4.4% April 2020)

- Also referred to as policy rate (all rates expressed in terms of basis points)

- Lent for short term to all RBI’s clients- Central and state govts, banks, Financial intermediaries

- Collateral is Govt securities and a repurchase agreement is also signed

- Cannot use govt securities of SLR for repo transactions

- Minimum borrowing is 5cr

- In practice it is not called an interest rate but considered a discount on the dated government securities, which are deposited by institution to borrow for the short term.

- In October 2013, RBI introduced term repos (of different tenors, such as, 7/14/28 days), to inject liquidity over a period that is longer than overnight. It has several purposes to serve— stronger money market, stability, and better costing and signaling of the loan products.

Long Term Repo Operations (LTROs)

Usually, Repo loans are for short term borrowing from overnight to 14-days. But in 2020-Feb, RBI announced to conduct Long Term Repo Operations (LTROs) of 1 year and 3-year tenors.

- RBI will loan total ₹ 1,00,000 crore, in various rounds through E-Kuber platform.

- RBI’s clients can apply to borrow a minimum ₹1 crore or higher.

- Interest rate would be prevailing repo rate. Interest rate will be compounded annually.

- This will increase loanable funds with banks and economic growth can be revived.

- MSF and (short term) repo lending will also be continued separately as per their own existing norms. LTRO doesn’t aim to eliminate / replace them.

Marginal standing facility (MSF) (4.65% April 2020)

- Only SCBs except RRBs, can use this window

- Collateral is G-secs from SLR quota. Though there would be a shortfall for SLR because of MSF transaction, the banks will not be fined.

- A maximum of 3% (March 2020) of NDTL worth GAS can be used from the SLR quota

- At present the rate is 0.25% above repo

- Minimum borrowing is 1cr

LAF- Reverse repo

- Interest rate at which RBI borrows for short term from its clients.

- April 2020: The rate is 3.75%, which is 65 basis points less than Repo. This is also called LAF window

- March 2020: The Reverse repo was 40 BPs less than Repo i.e RR was 4%. Before this rate cut the Reverse Repo was 4.9% and repo was 5.15%

All these transactions happen on the e-Kuber platform of the RBI