Why in news?

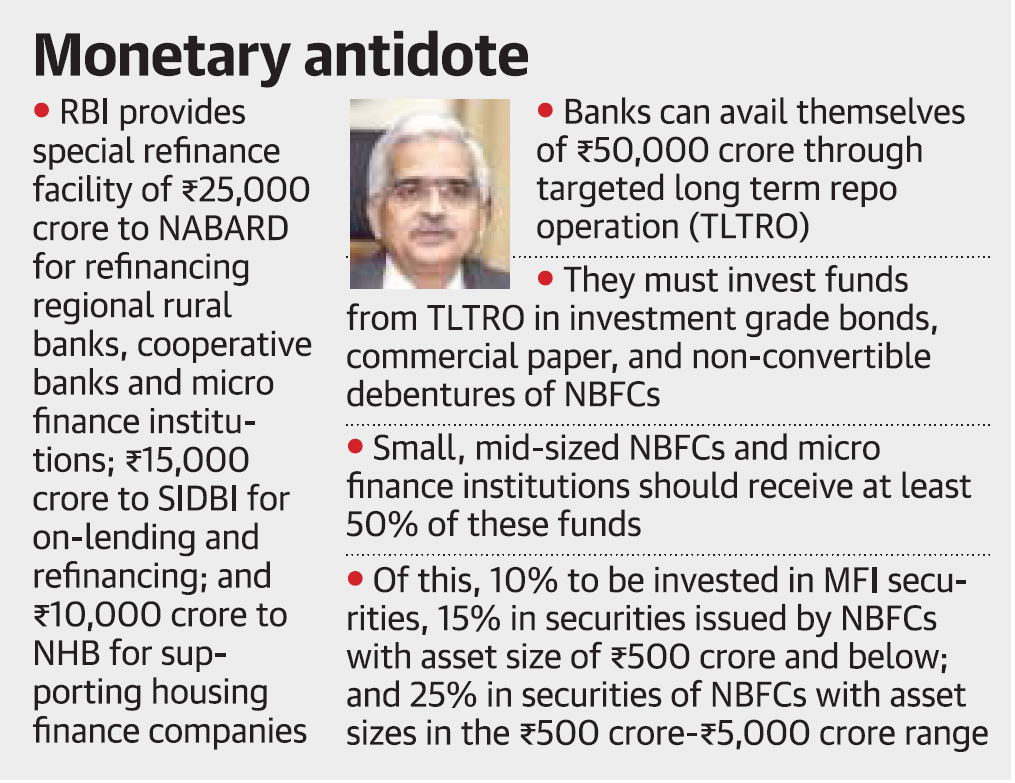

- In a move to ease financial stress and to maintain adequate liquidity in the system, the Reserve Bank of India has announced several steps on 17th April 2020 including targeted long–term repo operations and providing special refinance to financial institutions like NABARD, SIDBI and National Housing Bank.

- The Reserve Bank of India (RBI) has announced a host of measures to provide liquidity support to non-banking financial companies (NBFCs), apart from giving them certain benefits for loans extended to the commercial real estate sector.

What has RBI decided to do?

- RBI decided to conduct targeted long-term repo operations (TLTRO 2.0) for an aggregate amount of ₹50,000 crore, to begin with, in tranches of appropriate sizes.

- Banks should deploy these funds by investing in investment grade bonds, commercial paper, and non-convertible debentures of NBFC with at least 50% of the total amount availed going to small and mid-sized NBFCs and MFIs.

- NBFCs and housing finance companies are facing liquidity pressure since banks have not extended any repayment moratorium to these entities even if NBFCs have to provide the same for their borrowers.

- RBI has also decided to provide special refinance facilities for a total amount of ₹50,000 crore to NABARD, SIDBI and NHB to enable them to meet sectoral credit needs.

- Reverse repo has been reduced by 25 bps to 3.75% — to discourage banks to park surplus funds with RBI.

- RBI has also increased the ways and means advances limit further for states. It has decided to increase the WMA limit of states by 60 per cent over and above the level as on March 31. The increased limit will be available till September 30, 2020.

- For all accounts which lenders decided to grant moratorium, RBI said, there would be an asset classification standstill for all such accounts from March 1, 2020 to May 31, 2020.

- With the objective of ensuring that banks maintain sufficient buffers and remain adequately provisioned to meet future challenges, they will have to maintain higher provision of 10% on all such accounts under the standstill, spread over two quarters, i.e., March, 2020 and June, 2020.

- RBI also said scheduled commercial banks and cooperative banks shall not make any further dividend payouts from profits pertaining to the financial year ended March 31, 2020 until further instructions.

- The regulator has also brought down the liquidity coverage ratio requirement for Commercial Banks from 100 per cent to 80 per cent with immediate effect.

How will these measures help?

- These measures would facilitate increase in economic activities as the lockdown is progressively eased. State governments would start making pending payments and banks and NBFCs would activate their lending programme more aggressively.

- The set of packages by RBI is an excellent reflection of combining the policy response and regulatory responses in the most optimal manner.

- Increase in the Ways and Means Advances limit should provide a short-term relief to the state governments, by extension calming states’ yields and as a second derivative to cap markets’ borrowing costs.

- The cut of reverse repo rate by 25 basis points will also give a required push to the banks to open up the credit flow to keep economic activities moving smoothly.

- Standstill in asset classification and one-time restructuring for commercial real estate will support banking sector stability.