Context:

A Reserve Bank of India (RBI) Working Group (WG) on digital lending, including lending through online platforms and mobile apps, has recommended a separate legislation to oversee such lending as well as a nodal agency to vet the Digital Lending Apps.

Relevance:

GS-III: Internal Security Challenges (Cyber security related issues), GS-III: Indian Economy

Dimensions of the Article:

- Introduction to Digital Lending

- Benefits of digital lending

- Issues with digital lending

- Steps Taken by RBI

- Recommendation of the RBI Working Group (WG) on digital lending

Introduction to Digital Lending

- Digital Lending is basically lending through web platforms or mobile apps, by taking advantage of technology for authentication and credit assessment.

- India’s digital lending market has seen a significant rise over the years. The digital lending value increased from USD 33 billion in FY15 to USD 150 billion in FY20 and is expected to hit the USD 350-billion mark by FY23.

- Banks have launched their own independent digital lending platforms to tap in the digital lending market by leveraging existing capabilities in traditional lending.

Benefits of digital lending

- Digital Lending helps in meeting the huge unmet credit need, particularly in the microenterprise and low-income consumer segment in India.

- It also helps in reducing informal borrowings as it simplifies the process of borrowing. Indians continue to borrow from family and friends, and moneylenders, sometimes at unreasonably high interest rates, primarily because these loans are more flexible and convenient.

- It decreases time spent on working loan applications in-branch. Digital lending platforms have also been known to cut overhead costs by 30-50%.

Issues with digital lending

- There is a growing number of unauthorized digital lending platforms and mobile applications.

- These unauthorized digital lending platforms charge excessive rates of interest and additional hidden charges.

- They adopt unacceptable and high-handed recovery methods.

- They also misuse agreements to access data on mobile phones of borrowers.

- They attract borrowers with promise of loans in a quick and hassle-free manner.

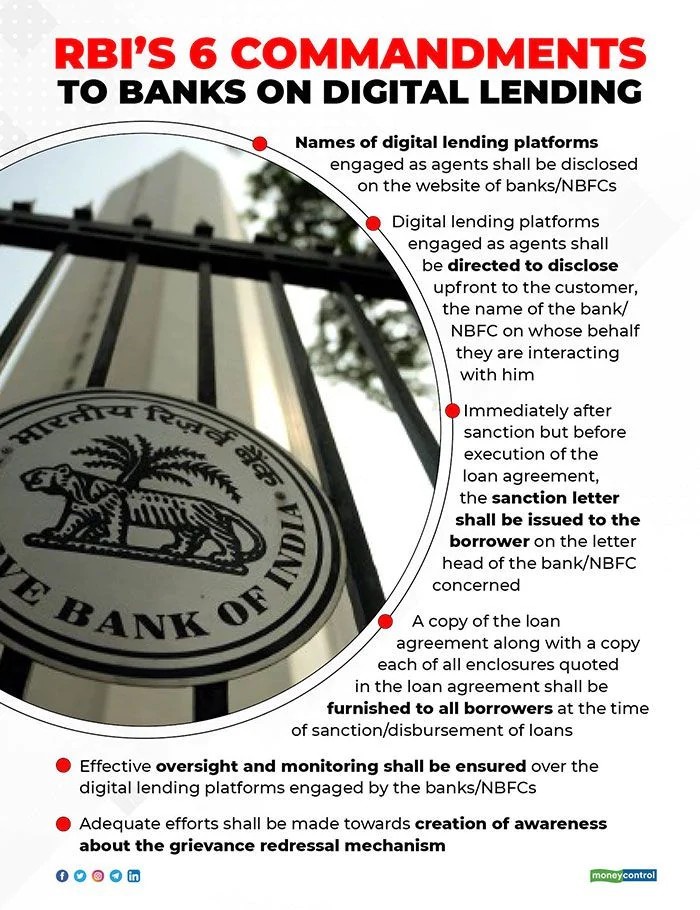

Steps Taken by RBI

- Non-Banking Financial Companies (NBFCs) and banks need to state the names of online platforms they are working with.

- RBI has also mandated that digital lending platforms which are used on behalf of Banks and NBFCs should disclose the name of the Bank(s) or NBFC(s) upfront to the customers.

- The central bank had also asked lending apps to issue a sanction letter to the borrower on the letter head of the bank/ NBFC concerned before the execution of the loan agreement.

- Legitimate public lending activities can be undertaken by banks, NBFCs registered with the RBI and other entities who are regulated by state governments under statutory provisions.

Recommendation of the RBI Working Group (WG) on digital lending

- A separate legislation should be enacted to oversee such lending.

- Setup a nodal agency to vet the Digital Lending Apps.

- A Self-Regulatory Organisation should be set up for participants in the digital lending ecosystem.

- Develop certain baseline technology standards and compliance with those standards as a pre-condition for offering digital lending solutions.

- Disbursement of loans should be made directly into the bank accounts of borrowers and servicing of loans should be done only through the bank accounts of the digital lenders.

- All data collection must require the prior consent of borrowers and come ‘with verifiable audit trails’ and the data itself ought to be stored locally.

-Source: The Hindu