What is Social Audit?

Social audit is a process in which details of resources used by public agency for development initiatives are shared with people often through public platforms, which allows end users to scrutinize the impact of developmental programs.

Social audit serves as an instrument for the measurement of social accountability of an organization. It gained significance after the 73rd amendment of the constitution relating to Panchayat Raj institutions.

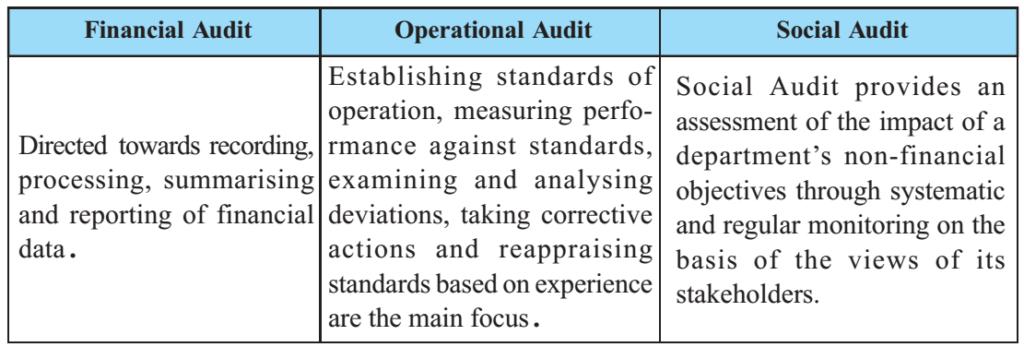

Difference with other audits

Need of Social Audit

The investment of large amount of funds and resources by the Government of India and various national and international agencies, since independence in social development programmes, has not been justified by the impact it has made.

The major focus by the Government hitherto has been in the supply side of the Programme Delivery System. While improvement of the SUPPLY SIDE is a long term process strengthening the DEMAND SIDE, may be a short run process, which will improve the effectiveness of the total delivery system much faster.

Principles of Social Audit

Eight specific key principles have been identified from Social Auditing practices around the world:

1. Multi-Perspective: Reflect the views of all the stakeholders.

2. Comprehensive: Report on all aspects of the organisation’s work and performance.

3. Participatory: Encourage participation of stakeholders and sharing of their values.

4. Multidirectional: Stakeholders share and give feedback on multiple aspects.

5. Regular: Produce social accounts on a regular basis

6. Comparative: Provide a means whereby the organisation can compare its performance against benchmarks and other organisations’ performance.

7. Verified: Social accounts are audited by a suitably experienced person or agency with no vested interest in the organisation.

8. Disclosed: Audited accounts are disclosed to stakeholders and the wider community in the interests of accountability and transparency.

Significance of Social Audit

• Enhances reputation: Social Auditing helps the legislature and executive in identifying the problem areas and provides an opportunity to take a proactive stance and create solutions.

• Alerts policymakers to stakeholder trends

• Increases accountability: There is a strong emphasis on openness and accountability for government departments. This leads to reduction in wastages and corruption.

• Assists in re-orienting and re-focusing priorities: Social Auditing could be a useful tool to help departments reshape their priorities in tune with people’s expectations.

• Provides increased confidence in social areas: Social Audit can enable departments/ institutions to act with greater confidence in social areas that have been neglected in the past or have been given a lower priority.

In recent years due to the steady shift in devolution of funds and functions to the local government, the demand for social audit has grown. In flagship schemes such as MGNREGA, the Union Government is promoting social audit to check corruption.

Limitations of Social Audit

• The scope of social audits is highly localised and covers only certain selected aspects.

• Social audits are often sporadic and ad hoc.

• Monitoring is informal and unprocessed.

• The findings of social audit cannot be generalised over the entire population.

• Several problems require a package of programme to be implemented simultaneously. For example, rural health requires convergence between water supply, education, sanitation, nutrition etc. Social audit may therefore need a more holistic approach.

• Absence of trained auditors.

• Lack of action on audit reports and findings.