Contents

- Dangerous suggestion

- The migrant worker as a ghost among citizens

- With land rights, but no land

DANGEROUS SUGGESTION

Context:

Former RBI governor Raghuram Rajan and ex-deputy governor Viral Acharya argued against allowing companies to own banks because it would allow non-financial businesses to gain easy access to financing and encourage connected lending and because it could lead to further concentration of economic and political power in certain business houses.

Relevance:

GS Paper 2: Indian Economy (issues re: planning, mobilisation of resources, growth, development, employment); Inclusive growth and issues therein.

Mains Questions

- The banking sector needs reform but the recommendation of corporate-owned banks is neither ‘big bang’ nor risk-free. Critically comment. 15 marks

- Banking sector needs more competition. But allowing corporates in without strong regulation could heighten systemic risk. Discuss. 15 marks

Dimensions of the article

- Status of the Banking sector in India

- Key points of the Internal Working Group of the Reserve Bank of India

- Issues related to the corporate houses be given bank licences

- Way Forward

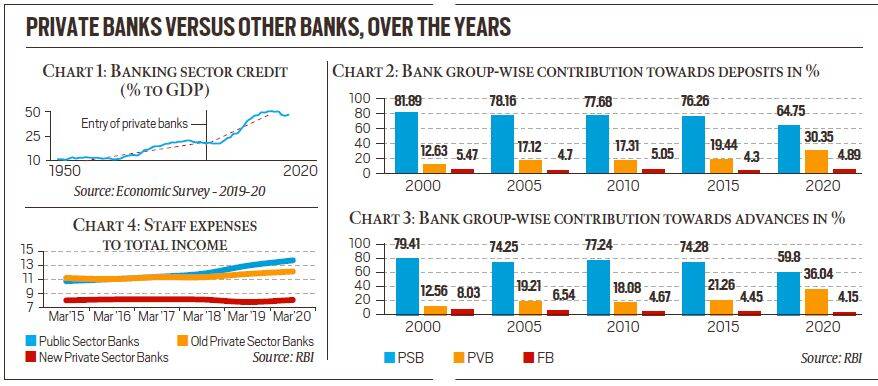

Status of the Banking Sector in India

- The banking system in any country is of critical importance for sustaining economic growth. India’s banking system has changed a lot since Independence when banks were owned by the private sector, resulting in a “large concentration of resources in the hands of a few business families”.

- To achieve “a wider spread of bank credit, prevent its misuse, direct a larger volume of credit flow to priority sectors and to make it an effective instrument of economic development”, the government resorted to the nationalisation of banks in 1969 (14 banks) and again in 1980 (6 banks).

- With economic liberalisation in the early 1990s, the economy’s credit needs grew and private banks re-entered the picture. This had a salutary impact on credit growth.

- However, even after three decades of rapid growth, “the total balance sheet of banks in India still constitutes less than 70 per cent of the GDP, which is much less compared to global peers” such as China, where this ratio is closer to 175%.

- Moreover, domestic bank credit to the private sector is just 50% of GDP when in economies such as China, Japan, the US and Korea it is upwards of 150 per cent. In other words, India’s banking system has been struggling to meet the credit demands of a growing economy. There is only one Indian bank in the top 100 banks globally by size. Further, Indian banks are also one of the least cost-efficient.

Clearly, India needs to bolster its banking system if it wants to grow at a fast clip. In this regard, it is crucial to note that public sector banks have been steadily losing ground to private banks. Private banks are not only more efficient and profitable but also have more risk appetite.

Key points of the Internal Working Group of the Reserve Bank of India

Entry of Corporates into Banking Space:

- Large corporates and industrial houses may be allowed as promoters of banks only after necessary amendments to the Banking Regulation Act, 1949.

- A promoter is an individual or organization that helps raise money for some type of investment activity.

- This is to prevent connected lending and exposures between the banks and other financial and non-financial group entities.

- Connected lending is modelled as a situation in which the bank’s controlling owner extends loans of inferior quality at lower interest rates to himself or his connected parties.

- Credit exposure is a measurement of the maximum potential loss to a lender if the borrower defaults on payment.

- The RBI has been against allowing corporate houses to set up or run commercial banks due to their poor track record on governance and credit disbursement.

- Corporate houses routinely delay payments to banks and the system has no in-built incentives or disincentives for orderly debtor behaviour.

Conversion of NBFCs into Banks:

- Well-run large NBFCs, with an asset size of Rs. 50,000 crore and above, including those which are owned by a corporate house, may be considered for conversion into banks subject to completion of 10 years of operations and meeting due diligence criteria and compliance with additional conditions specified in this regard.

Hike in Promoters’ Stake:

- The cap on promoters’ stake in the long run (15 years) may be raised from the current level of 15% to 26% of the paid-up voting equity share capital of the bank.

- On non-promoter shareholding, the panel has suggested a uniform cap of 15% of the paid-up voting equity share capital of the bank for all types of shareholders.

Hike in Minimum Capital for New Banks:

- The minimum initial capital requirement for licensing new banks should be enhanced from Rs. 500 crore to Rs. 1,000 crore for universal banks and from Rs. 200 crore to Rs. 300 crore for small finance banks.

- Universal Banks combine the three main services of banking viz. wholesale banking, retail banking, and investment banking under one roof. For example, Deutsche Bank, Bank of America, HSBC, etc.

Payments Banks’ Conversion into Small Finance Bank:

- For payments banks intending to convert to a Small Finance Bank (SFB), a track record of 3 years of experience as payments bank may be considered as sufficient.

- Payments banks (Airtel Payments Bank, India Post Payments Bank, etc.) are like any other banks, but operating on a smaller or restricted scale.

- Small Finance Banks are the financial institutions which provide financial services to the unserved and unbanked region of the country.

Harmonisation and Uniformity in Different Licensing Guidelines:

- The RBI should take steps to ensure harmonisation and uniformity in different licensing guidelines, to the extent possible.

- Whenever new licensing guidelines are issued, if new rules are more relaxed, the benefit should be given to existing banks, and if new rules are tougher, legacy banks should also conform to new tighter regulations, but a non-disruptive transition path may be provided to affected banks.

Non Operative Financial Holding Company:

- NOFHC should continue to be the preferred structure for all new licenses to be issued for universal banks. However, it should be mandatory only in cases where the individual promoters, promoting entities and converting entities have other group entities.

- NOFHC is a financial institution through which promoter/promoter groups will be permitted to set up a new bank.

- Entities or groups in the private sector, public sector and NBFCs can set up these wholly-owned NOFHCs.

Issues related to the corporate houses be given bank licences

As the report notes, the main concerns are interconnected lending, concentration of economic power and exposure of the safety net provided to banks (through guarantee of deposits) to commercial sectors of the economy.

Increasing concentration of economic power:

- Corporate houses can easily turn banks into a source of funds for their own businesses.

- In addition, they can ensure that funds are directed to their cronies.

- They can use banks to provide finance to customers and suppliers of their businesses.

- Adding a bank to a corporate house thus means an increase in concentration of economic power.

- Just as politicians have used banks to further their political interests, so also will corporate houses be tempted to use banks set up by them to enhance their clout.

Exposure of the safety net provided to banks:

- The banks owned by corporate houses will be exposed to the risks of the non-bank entities of the group. If the non-bank entities get into trouble, sentiment about the bank owned by the corporate house is bound to be impacted. Depositors may have to be rescued through the use of the public safety net.

Interconnected Lending:

- The Internal Working Group believes that before corporate houses are allowed to enter banking, the RBI must be equipped with a legal framework to deal with interconnected lending and a mechanism to effectively supervise conglomerates that venture into banking.

- It is naive to suppose that any legal framework and supervisory mechanism will be adequate to deal with the risks of interconnected lending in the Indian context.

- Corporate houses are adept at routing funds through a maze of entities in India and abroad. Tracing interconnected lending will be a challenge.

- Monitoring of transactions of corporate houses will require the cooperation of various law enforcement agencies. Corporate houses can use their political clout to thwart such cooperation.

- The RBI can only react to interconnected lending ex-post, that is, after substantial exposure to the entities of the corporate house has happened. It is unlikely to be able to prevent such exposure.

- Suppose the RBI does latch on to interconnected lending. How is the RBI to react? Any action that the RBI may take in response could cause a flight of deposits from the bank concerned and precipitate its failure. The challenges posed by interconnected lending are truly formidable.

Regulator credibility at stake

- Pitting the regulator against powerful corporate houses could end up damaging the regulator. The regulator would be under enormous pressure to compromise on regulation. Its credibility would be dented in the process. This would indeed be a tragedy given the stature the RBI enjoys today.

Moreover, The Committee on Financial Sector Reforms (2008) had set its face against the entry of corporate houses into banking. It had observed, “The Committee also believes it is premature to allow industrial houses to own banks. This prohibition on the ‘banking and commerce’ combine still exists in the United States today, and is certainly necessary in India till private governance and regulatory capacity improve.

Way Forward

India’s banking sector needs reform but corporate houses owning banks hardly qualifies as one. If the record of over-leveraging in the corporate world in recent years is anything to go by, the entry of corporate houses into banking is the road to perdition.

There is a strong case for liberalising entry into the banking sector, and to encourage the creation of big private banks capable of meeting the financing needs of the economy, a system of stringent checks and balances will need to be put in place before the central bank contemplates any such step.

THE MIGRANT WORKER AS A GHOST AMONG CITIZENS

Context:

When Prime Minister Narendra Modi announced the world’s most stringent lockdown on March 24, 2020 with barely four hours-notice, lakhs of migrant workers across the country found themselves trapped in a novel situation: their livelihood in the city was gone, but they could not return to their native villages.

Relevance:

GS Paper 2: Welfare Schemes (centre, states; performance, mechanisms, laws, institutions and bodies constituted for protection of vulnerable sections);

Mains Questions

- The active production of migrant labour and their invisibilised exploitation are two parallel processes that feed into each other. Elaborate. 15 marks

Dimensions of the Article

- What is Migration?

- Migrants in India

- Causes of internal migration in India

- Issues related to internal migration in India

- Measures to address these issues

- Way Forward

What is Migration?

Human migration involves the movement of people from one place to another with intentions of settling, permanently or temporarily, at a new location (geographic region).

Migrants in India

- The Census defines a migrant as a person residing in a place other than his/her place of birth (Place of Birth definition) or one who has changed his/ her usual place of residence to another place (change in usual place of residence or UPR definition).

- The number of internal migrants in India was 450 million as per the most recent 2011 census.

- Seasonal Migrants: Economic Survey of India 2017 estimates that there are 139 million seasonal or circular migrants in the country.

Causes of internal migration in India

- Unemployment in hinterland: An increasing number of people do not find sufficient economic opportunities in rural areas and move instead to towns and cities.

- Marriage: It is a common driver of internal migration in India, especially among women.

- Pull-factor from cities: Due to better employment opportunities, livelihood facilities etc cities of Mumbai, Delhi, and Kolkata are the largest destinations for internal migrants in India.

Issues related to internal migration in India

- Non-portability of entitlements for migrant labourers (such as the Public Distribution System) which further gets aggravated due to absence of identity documentation.

- Absence of reliable data: The current data structure lacks realistic statistical account of their number and an understanding of the nature of their mobility.

- Data on internal migration in India is principally drawn from two main sources –Census and the surveys carried out by the National Sample Survey Office. One of the main lacunae of both the Census and NSS surveys is their failure to adequately capture seasonal and/or short-term circular migration.

- A large majority of migrants hail from historically marginalized groups such as the SCs and STs, which adds an additional layer of vulnerability to their urban experiences.

- Exploitation by Employers and Contractors (Middlemen): in the form of Non-payment of wages, physical abuse, accidents. The existing legal machinery is not sensitive to the nature of legal disputes in the unorganized sector.

- Lack of Education: The issue of lack of access to education for children of migrants further aggravates the intergenerational transmission of poverty.

- Housing: Migration and slums are inextricably linked, as labor demand in cities and the resulting rural-to-urban migration creates greater pressures to accommodate more people.

- Social Exclusion: Since the local language and culture is different from that of their region of origin they also face harassment and political exclusion.

- Due to migrant’s mobile nature, they don’t find any place in the manifestos of trade unions.

- Stuck in the cycle of poverty: Most migrants are generationally stuck in a vicious cycle of poverty. (See infographic.)

Way Forward

- Universal food grain distribution: There are 585 lakh tonnes of grains stored in Food Corporation of India god owns, which could be proactively distributed.

- Direct cash transfers: Mechanisms could be evolved to deliver cash directly into the hands of people, instead of routing it through bank accounts.

- Inter-state coordination committee could be formed to ensure safe passage of migrants to their villages.

- Legal cell at the central and state levels could be created to protect wages. As there have been claims of non-payment of wages, forced leaves and retrenchments.

- Mapping of migrant workers: There is a need to create a database to map migrant workers scattered across the country. Government is planning to map migrant workers which would be first comprehensive exercise to map migrant workers scattered across sectors.

The challenges of the migrant problem are complex, also lack of recognition for migrants is still to be fully addressed. But if policy makers are able to recognize migrant workers as a dynamic part of a changing India, migration instead of being part of the problem will start becoming part of the solution.

Background

1: Internally Displaced People: Internal Migration due to disasters

- India had the highest number of new disaster displacements (five million) in the world in 2019 as per the Global Report on Internal Displacement, 2020.

- These were the result of a combination of increasing hazard intensity, high population exposure, conflicts and high levels of social and economic vulnerability.

- 590,000 people live in internal displacement as a result of disasters in India. New disaster displacements were a result of various cyclones like Fani, Vayu, Bulbul etc along with south west monsoon and droughts in various parts.

- IDPs are different from refugees in that, having not crossed a border, they are not typically covered by international refugee protections. They remain subjected to national laws, and as such are afforded less protection.

WITH LAND RIGHTS, BUT NO LAND

Context:

Tribal politics in the erstwhile State of Jammu and Kashmir was focused on the twin issues of political reservation and enactment/extension of the Forest Rights Act (FRA) of 2006.

Relevance:

GS Paper 2: Welfare Schemes (centre, states; performance, mechanisms, laws, institutions and bodies constituted for protection of vulnerable sections);

Mains Questions:

- What are the salient features of the Forest Right Act 2006. Assess the role of Forest Right Act to protect to rights of tribal people. 15 marks

Dimensions of the Article:

- What is the Forest Right Act?

- Rights under forest right Act

- Challenges in implementation of the Forest Right Act

- Way forward

What is the Forest Rights Act?

- Schedule Tribes and Other Forest Dwellers Act or Recognition of Forest Rights Act came into force in 2006. The Nodal Ministry for the Act is Ministry of Tribal Affairs.

- It has been enacted to recognize and vest the forest rights and occupation of forest land in forest dwelling Scheduled Tribes and other traditional forest dwellers, who have been residing in such forests for generations, but whose rights could not be recorded.

- This Act not only recognizes the rights to hold and live in the forest land under the individual or common occupation for habitation or for self-cultivation for livelihood, but also grants several other rights to ensure their control over forest resources.

- The Act also provides for diversion of forest land for public utility facilities managed by the Government, such as schools, dispensaries, fair price shops, electricity and telecommunication lines, water tanks, etc. with the recommendation of Gram Sabhas.

Rights under the Forest Right Act 2006

- Title Rights- ownership of land being framed by Gram Sabha.

- Forest management rights– to protect forests and wildlife.

- Use rights- for minor forest produce, grazing, etc.

- Rehabilitation– in case of illegal eviction or forced displacement.

- Development Rights– to have basic amenities such as health, education, etc.

Challenges in implementation of the Forest Right Act

- Adivasi lands in Jammu and Kashmir have not been protected, nor have these communities been given ownership rights. Instead, evictions of Adivasis have intensified in the last few years.

- A series of legislation– amendments to the Mines and Minerals (Development and Regulation) Act, the Compensatory Afforestation Fund Act and a host of amendments to the Rules to the FRA- undermine the rights and protections given to tribal in the FRA, including the condition of “free informed consent” from gram Sabhas for any government plans to remove tribal from the forests and for the resettlement or rehabilitation package.

- The process of documenting communities’ claims under the FRA is intensive — rough maps of community and individual claims are prepared democratically by Gram Sabhas. These are then verified on the ground with annotated evidence, before being submitted to relevant authorities.

- There is a reluctance of the forest bureaucracy to give up control with FRA being seen as an instrument to regularise encroachment. This is seen in its emphasis on recognising individual claims while ignoring collective claims — Community Forest Resource (CFR) rights as promised under the FRA — by tribal communities. To date, the total amount of land where rights have been recognised under the FRA is just 3.13 million hectares, mostly under claims for individual occupancy rights.

- In almost all States, instead of Gram Sabhas, the Forest Department has either appropriated or been given effective control over the FRA’s rights recognition process. This has created a situation where the officials controlling the implementation of the law often have the strongest interest in its non-implementation, especially the community forest rights provisions, which dilute or challenge the powers of the forest department.

- Saxena Committee pointed out several problems in the implementation of FRA. Wrongful rejections of claims happen due to lack of proper enquiries made by the officials.

Way Forward

- In spite of its inadequacies, there can be little doubt that the Forest Rights Act (FRA) stands as a powerful instrument to protect the rights of tribal communities. The little progress that has been made in implementation so far has been due to close coordination between tribal departments, district administrations and civil society.

- There is a clear need to strengthen the nodal tribal departments, provide clear instructions to the State and district administrations, and encourage civil society actors.