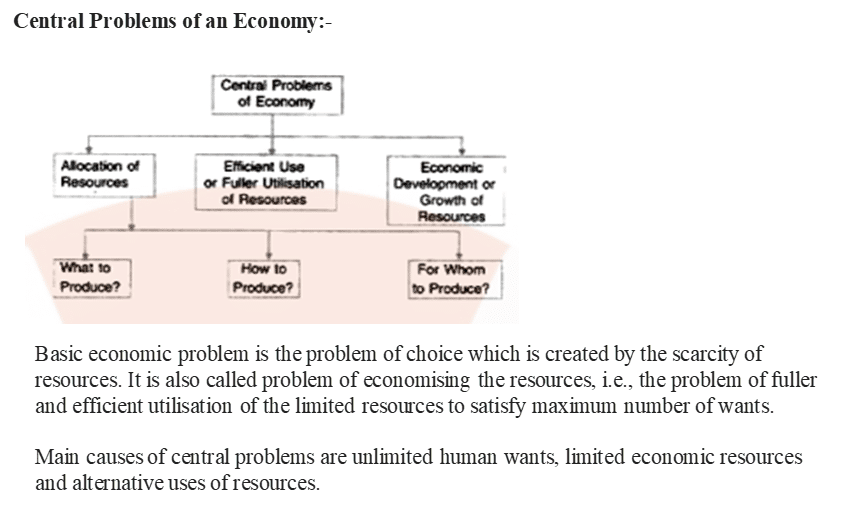

Allocation of resources:-

(i) What to produce and how much to produce?

(ii) How to produce?

(iii) For whom to produce?

What to produce: – An economy have unlimited wants and limited means having alternative use. Economy can’t produce all type of goods like consumer goods, producer goods etc. So, Economy has to make a choice what type of goods and services are to be produced and in what quantities.

How to produce: – It is the problem of choice of technique of production. There are two techniques of production.

• (a) Labour Intensive Technique: – It is the technique of production when labour is used more than capital.

• (b) Capital Intensive Technique: – In this technique capital is used more than Labour.

For whom to produce: – It is the problem related to distribution of produced goods among the different group of the society.

It has two aspects:-

1. Personal distribution

2. Functional distribution

Personal distribution: – When the National Income is distributed according to the ownership of the factors of production.

Functional distribution: – When the national Income/Production is distributed among different factors of production like Land, Labour, capital and Entrepreneurship for providing their service in term of rent, wages, interest and profit respectively

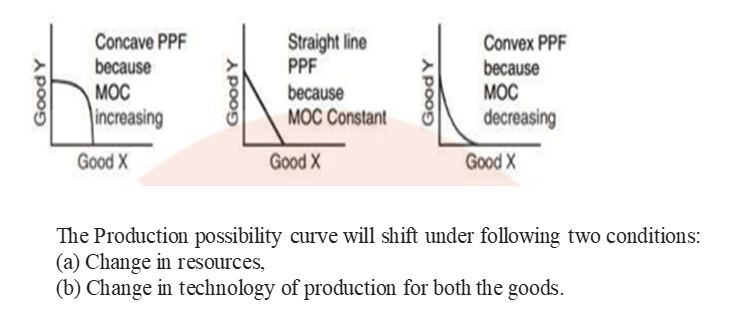

Production possibility frontier or production possibility curve

This shows all possible combinations of two set of goods that an economy can produce with available resources and given technology, assuming that all resources are fully and efficiently utilized.

Production Possibility Frontier or Curve Features

- Slopes downward from left to right because if production of one commodity is to be increased then production of other commodity has to be sacrificed as there is scarcity of resources.

- Concave to the origin because of increasing marginal opportunity cost or (MRT)

Marginal Rate of Transformation (MRT) – It is the amount of one commodity that is to be sacrificed to increase the production of other commodity by one unit. It can also called Marginal Opportunity Cost.

It is defined as the additional cost in terms of number of units of a good sacrificed to produce an additional unit of the other good.

Production Possibility Curve and Central Problems:-

The production possibility curve solves five problems –

- what and how much to produce,

- how to produce,

- full utilisation of resources,

- economic efficiency and

- economic growth.

Production possibility curve is unable to solve the economic problem ‘for whom to produce’.

Ways to solve fundamental problems in captalistic and planned economies:-

In a market oriented or capitalist economy, the fundamental problems are solved by the market mechanism.

In a planned economy, all the economic decisions regarding what, how and for whom to produce are solved by the state through planning. Economic planning replaces the price mechanism. The market is regulated by the state. The prices of the various products are fixed by the state which are called administrated prices.