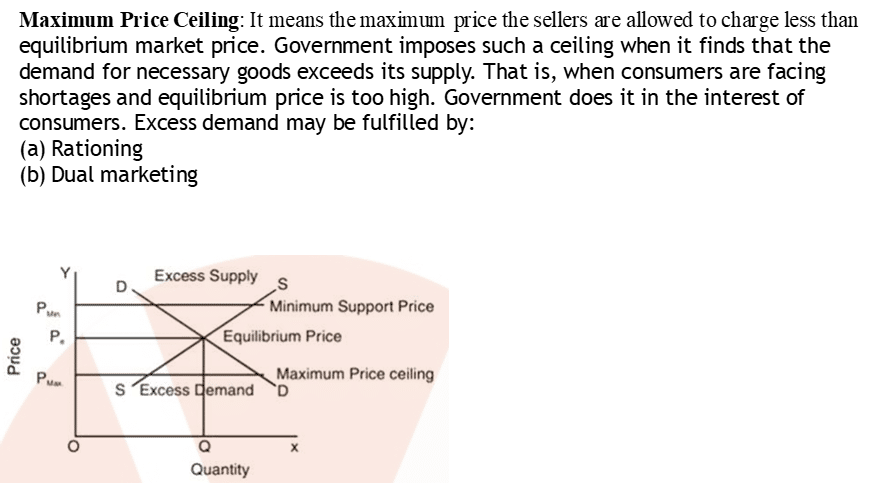

Minimum Price Ceiling: It means that producer are not allowed to sell, the goods below the price fixed by Government, When government finds that equilibrium price is too low for the produce, then Govt. fixes a price ceiling higher than equilibrium price to prevent the possible loss to the producers. The price is also called floor price or minimum support price. Generally, government buys the excess supply at this price.

Technological Progress on Supply Curve:-

Technological progress reduces the marginal cost of production. Producers can produce comparatively more goods and services with the help of available factors of production. This situation is likely to shift the supply curve rightward.

There is a positive relationship between technological progress and supply. Technological progress often leads to a decline in the cost of production which enables producers to produce and supply more goods and services at the existing price.

Thus, technological progress is likely to increase supply causing a rightward shift in the supply curve.